RSS

RSS|

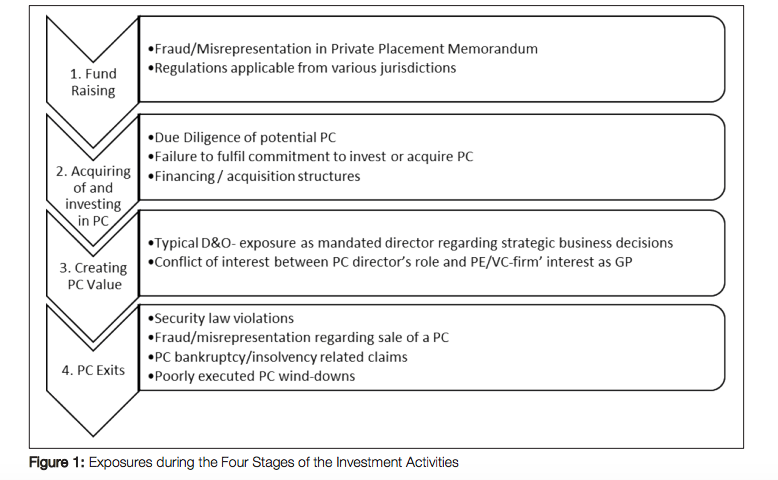

By: Gregory Walker FCII, ANZIIF (Fellow), ARM-E, Walker Risk Solution Private Equity-firms are known to be calculated risk takers; and this approach has rewarded many of them and their investors. But how much risk are they willing to take when it comes to their firm�s liability? Or their own personal liability? Many partners engaged in Private Equity-firms (PE-firms) take comfort knowing they will be protected by indemnification from the fund, the fund management company or a portfolio company if they are sued while serving on its board. But even if the fund can indemnify the individuals, PE-firms may be reluctant to do so, as settlements divert money from the fund and negatively impact internal rate of return. This could lead to disputes with fund investors. Such disputes are fairly seldom in the PE/VC community, but when they happen, they rarely arise early during a fund�s life; rather they materialise when the fund is later stage and there is little capital left in the fund to satisfy indemnification obligations. Following the AIFMD1 (and its Swiss equivalent) the liability exposure for PE-firms from their operational risks needs to be backed either by additional equity or by insurance. Having a choice, taking out insurance may be better aligned with the investors� interests: Invest Europe2 noted during the consultation process of the AIFMD, that �professional indemnity insurance should be a far better policy instrument to meet the risks to investors from professional negligence than additional own funds. Requiring additional own funds reduces the ability of the owners of the AIFM (typically the senior management) to invest in the AIF. This has traditionally been a key mechanism, insisted on by private equity and venture capital AIF investors, for aligning the interests of investors and AIFM.� The insurance market has responded to the needs of the PE/VC business by creating an industry-specific coverage (in the following called �Venture Capital Liability Insurance� � VCAP insurance) in order to transfer these liability exposures. A properly structured VCAP policy not only can provide for defence of certain claims up to final adjudication but can also keep things from getting to that point by providing a funding source for a settlement that doesn�t impact the fund. Most importantly for those persons holding director positions within the investment structure, VCAP insurance can protect individuals in situations where they would not have the benefit of indemnification from the fund (e.g. when the lawsuit is a derivate suit initiated by the investors or a regulatory agency or when the partnership agreement does not permit indemnification). Liability claims against a PE-firm and its directors fall typically into one of the two categories: (1) �Fund Management�, creating an exposure to professional indemnity (PI) along the four stages of PE-investing as outlined below in section 1, and (2) �Board Representation�, a directors� & officers� liability exposure, which is examined in section 2. Next, section 3 illustrates how VCAP-insurance addresses these exposures and tells which pitfalls need to be avoided when implementing such insurance. Section 4 concludes. Liability Exposures During the Investment Phases Investors (the �limited partners�) expect the PE-firm (the �general partner�) to manage the fund according to guidelines outlined in private placement memorandums. When describing a typical investment process for direct investments, four stages with different core activities and their associated risks can be detected: Stage 1 - Fund Raising The solicitation process of institutional investors is started by presenting the investment strategy of the fund. It is key that all information needed to get a full and clear picture of the investments and the associated risks is presented to the potential investors. This presentation is done via road shows and outlined in writing in the prospectus or private placement memorandum (PPM). The main exposure of this first stage is the actual or alleged fraud or misrepresentation and incorrect or incomplete risk disclosure in the PPM or other information provided during the solicitation process.

Stage 2 - Investing and Acquiring of Portfolio Companies (PC) Once the investors are on board and the necessary commitments have been received in the first closing, the fund manager enters into the stage of performing due diligence reviews of potential target companies. The selection of a PC as such, the chosen structure, the type of financing of the acquisition and other decisions taken in the context of the acquisition can be grounds for complaints by the investors. Whereby these allegations will be made by investors there is also a risk coming from another side: potential or future portfolio companies can claim compensation from the PE-firm or the fund manager for the failure to fulfil commitments to invest or acquire the portfolio company. Stage 3 - Creating PC Value The focus of the investment is to increase the value of the PC. The PE-firm will intend to do so by gaining influence on the business model of the PC sending employees to sit on the different board of directors. One person may hold between four to eight board seats. The PE-mandated directors are often directly engaged in strategic management decisions with the aim to make the PC more profitable and enhance their value. And, as directors, they are personally liable for wrongful management decisions. When the PC does not show the expected development and increase in value the range of potential allegations claiming wrongful management decisions or omissions is wide. The PEmandated director can consequently be facing allegations like any �regular� board member An additional risk, specific to the role as PE-mandated director, arises out of their �double role� which can lead to a potential conflict of interest: Being sent by the PE-firm to act as director to the PC, the employee is requested to act in the interest of the PE-firm (or the GP) whereas in the position as board member of the PC, the director has to act exclusively in the interest of the PC. In fact, allegations of conflicts of interests are widely seen in claims. Claims filed against board members of a PC can originate from various sources: the original founders of a PC, other members of the management, creditors, shareholders, competitors, suppliers, vendors, governmental/regulatory agencies or company employees. Even the PC itself can be the claimant and in such cases will not indemnify the director for the damages they claim. Stage 4 - Portfolio Company Exits There are a number of options available how the PE-firm can exit a PC: sale, IPO or - in case the investment did not develop well � �close the doors� (write down, liquidation, bankruptcy) � only to name a few. In the course of the divestment various aspects need to be monitored by the management of the PC. A potential breach of obligations can occur in different areas: a violation of applicable securities laws, misrepresentation or fraud in respect of the sale of a PC (potentially in a prospectus), non-fulfilment of contractual obligations of an M&A contract, duties of notification related to a bankruptcy proceeding of the PC, poor execution of the PC wind-down, negligence in respect of general reporting and information duties towards regulatory bodies or investors etc. with branch-offices and subsidiaries abroad, advising or managing offshore funds that hold SPVs and PCs in a variety of jurisdictions, and their directors have to comply with several legal and regulatory frameworks. Regulatory investigations and criminal prosecutions are often followed by civil law claims for compensation. In times when the company has financial problems, needs to be liquidated, a receiver is appointed or the company has already gone bankrupt, the management is facing a larger risk of being held personally liable for losses that shareholders, the entity or third parties have suffered. As the members of the management are thus putting their private assets at risk3 , such scenarios can turn into a very threatening situation.Even if the claimant has to prove that a wrong managerial decision or omission is the cause of such loss the manager will most probably defend him or herself immediately and incur substantial legal defence costs. Claims filed against board members of the PE-firm, of a fund or of a PC can originate from various sources: investors, competitors, suppliers, vendors, the PE-firm, the fund or the PC itself, its employees and management as well as other board members. Conclusions The liability risks a PE/VC-firm or their directors can be exposed to are many. As part of an enterprise-wide risk management, the directors of a PE-firm or a fund should evaluate how to mitigate these risks. This can be done by setting up a state of the art IT system, enhancing internal procedures and protection measures, training employees or adding audits. With respect to the residual risk after such mitigation efforts, a decision will have to be made on how much of the risk shall be transferred to external parties by e.g. concluding an insurance. For a director it is crucial to establish if the portfolio company, which he/she is joining as director, has D&O coverage in place. If in place, it is sensible to get specialist advisors to review and determine the coverage and the limits of liability provided. Alternatively, the director should request the PE-firm to arrange D&O insurance coverage extending to all mandated director positions on the board of multiple PC. With complex contracts, the devil is in the detail. Expert advice from an independent insurance broker is recommended. It is essential to have the terms of the insurance contract, definition of terms, exclusions, as well as obligations of the parties to the contract carefully reviewed in respect of the specific situation of the PE-firm. In addition to reviewing the policy terms and conditions, the board should take into consideration the insurer�s financial strength, underwriting expertise and claims-paying reputation. Editors Note: This article was abridged slightly for length. The full length article is available here. | |

|

This article was published in Opalesque's Private Equity Strategies our monthly research update on the global private equity landscape including all sectors and market caps.

|

Private Equity Strategies

How private equity firms and their directors protect themselves in case of liability claims |

|

{kind=link}