RSS

RSS|

Heeten H. Doshi, CFA is the founder of Doshi Capital Management, a private investment management firm where he manages the Doshi Systematic Strategy Fund. He also worked as a senior equity strategist in Brown Brothers Harrimans Portfolio Strategy team, where he focused on the US economy, equity market and sector/industry investment recommendations. Before that he worked at Morgan Stanley as a research analyst where he conducted bottom-up fundamental analysis covering the transportation industry and at Lehman Brothers where he was a fixed income trader, managing Lehmans loan risk exposure through the use of loan sales and derivative products. Heeten received an MS in Accounting from the University of Illinois and an MS in Management from Babson F.W. Olin Graduate School of Business and has obtained the CFA designation.

Heeten H. Doshi, CFA is the founder of Doshi Capital Management, a private investment management firm where he manages the Doshi Systematic Strategy Fund. Together with this team, Heeten runs a market timing strategy which with a live track record of almost nine years, defies conventional wisdom that you cannot time the market. While market timing may not (yet?) work on a daily basis, he believes that his nine years track show that with the right data and algorithms you might as well succeed in identifying risk on and risk off market periods on a weekly and monthly basis. Based on 7.5 years of fine-tuning and trading prop capital, the strategy opened up to outside investors in 2020, ending up 147.5% that year and continuing its positive run in 2021, up over 9% YTD by mid July. Matthias Knab: How would you describe your strategy and its benefits? And can you also tell us how you developed it and how it has evolved over the years?

Heeten Doshi: My investment approach has been formulated on the back of the 2000 dot- com and 2008 housing crisis with the aim to allow investors to stay invested through cycles through a diversifying, absolute return strategy. The algorithmic model both contrarian and momentum brings together several investing disciplines into a multi-factor composite that forecasts short to intermediate-term risk on and risk off periods of the market with the aim to grow and preserve capital in any market environment: True diversification, but without giving up performance. I founded Doshi Capital Management in 2011 with the goal that investors should be able to generate absolute positive returns regardless of the market environment or the economic environment. Our view and our belief was that investors should not have to suffer through corrections youll remember we had two 50% corrections, the housing and the tech bubble), and then in 2020 we had a 35% correction during the pandemic. The typical buy and hold investor will have to suffer holding through that volatility, and so our goal was to be able to create a strategy that is more dynamic and provides more diversification while generating absolute positive returns year in and year out. We think that an attractive absolute return strategy should really diversify the entire portfolio and lower overall portfolio risk, but it should also generate positive returns for the portfolio. The secret to a high Sharpe: Produce Alpha, when markets are down - which the S&P is 45% on a weekly basis. Believe it or not, over the past two decades the S&P 500 has had negative weeks 45% of the time. Thats pretty amazing if you think about it! Whats special about our strategy is that we not only avoid many of those weeks, but we generate alpha during those weeks, and thats how the strategy is able to have such a high risk reward ratio and a high sharp ratio, simply because we also generate alpha when the market is actually down. Matthias Knab: Thats fascinating. Tell us more how the strategy actually works?

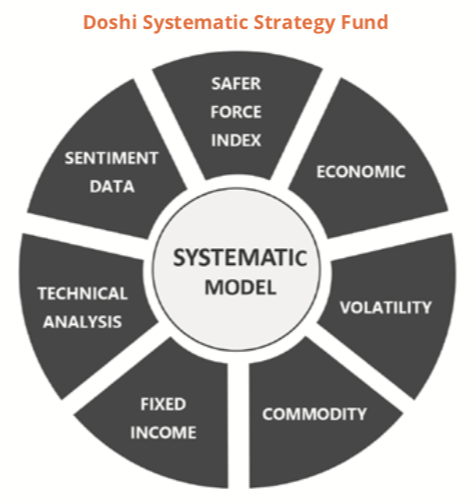

Heeten Doshi: So, you heard that right, our strategy is a market timing strategy. Its a systematic and algo driven model that determines risk-on and risk- off periods for the overall U.S. equity market. How the model works, is it takes into account a multitude of investing disciplines and basically breaking it down into the following main components. First of course is data, we use contrarian and momentum indicators and market data and behavioural data. We then also look into the speed and the different frequencies of data. There we use different speeds of algorithms to gauge that short to intermediate term and forecast the market. We also developed a proprietary earnings revisions indicator which is a very powerful tool. Theres a lot of academic research behind earnings revisions and the behavioural impact that it has on investors. We also look at macro data from fixed income to commodity prices, from interest rates to volatility, economic data, sentiment data, trader positioning, and so on. All that wide array of data goes into the model to forecast the risk on risk off periods. Matthias Knab: Tell us also more about the execution side of the strategy and which instruments do you actually trade? Heeten Doshi: To execute the strategy we use e-mini futures. We use the S&P futures and long-term treasury bond futures for liquidity reasons and also for the tax efficiency.

One of the biggest benefits of this strategy that is that it provides a lot of diversification. In our view there are two types of risks, theres unsystematic risk, for example single stock risk, and then theres also systematic risks, the macro risks. Our strategy diversifies away both of those because we invest in the overall index we are not taking single stock risk as were not investing in single stock names and then we also diversify systematic risk by the nature of the market timing strategy. You could also say our model is a macro model and it looks to avoid, or better, exploit those larger events. In fact, our focus has been on cycles and in my past history and career I have done a lot of work on macro cycles, and so embedding that cyclical work into this model allows us to forecast these sort of mini cycles in the in the market. Just summing up again, the strategy provides a lot of diversification, its uncorrelated to almost any other asset class, whether its equities or fixed income or REITS, bonds, gold or even other alternative assets, youll see that the strategy has a low correlation to almost anything else. At the same time, it also generates a lot of alpha. As I mentioned before, we use e-mini futures to execute our strategy. These are 1256 contracts that have tax benefit. Despite the short-term nature of our strategy, as per IRS code, investors are taxed 60% at the long-term capital gains rate and 40% at the short-term rate. This provides a significant tax efficiency to our investors. Matthias Knab: Walk us through how your strategy did in 2020. With a return of 147.5%, you certainly trumped the market and many other strategies.

Heeten Doshi: During the pandemic our strategy was risk off going into the pandemic. Obviously the model did not predict the pandemic, but looking at the indicators the model takes in we were actually in long-term treasuries entering the pandemic. We benefited on the way down and then also towards the correction the model then went risk on and it actually stayed risk on for almost the remainder of the year. So we benefited on the way down and on the way up. As I explained, the model is contrarian and also momentum, so going into the pandemic it was contrarian, it saw the market as overbought with elevated indicators, so it had a risk-off view. But if we look deeper, the model was actually changing on a week-to-week basis and timing the market moves on the way down, and when the rebound started to happen in the overall market, the model went risk on and it stayed risk on for weeks and months. Thats the momentum effect of the model. And so, for me, thats the beauty of the model that it takes into account contrarian data, momentum data and then also behavioural data, because if you look at just the absolute data at that time job numbers were still pretty bad, unemployment was very high, the economy was still shutting down and we were still learning the effects and the impact of COVID, but sentiment was already changing. After that 35% correction investors quickly started to believe that the worst was behind in terms of the market correction and thats what the model picked up. You may recall the confusion in the market about the quick and complete rebound at that time. Certainly, a lot of people that we have spoken to didnt understand and questioned why the market was rallying in a V shape when the economy was still cratering. Its really about forward expectations and behavioural expectations. Many investors did not understand or missed this because they were only looking at the absolute data and not only said, Wow, this is horrible! but also missing out on the rebound. As I said, we built the strategy not just to look at economic data but also at sentiment positioning, how are other investors positioning, because at the end of the day, the market has a mind of its own. You may also recall that I mentioned speed and frequency, so by having shorter term frequency data and shorter term calculations were able to exploit that week to week down move that we saw from February through March when the market was correcting, but then also having those longer term data, the longer term algorithms and the momentum data we were able to ride the wave up and stay invested early on when the market was rallying. We had a lot of investors calls who told us they were selling when the market corrected 35% and then when it started to bounce they continued to trim their positions as the market was moving up thinking that it was going to correct again. But it never did, the market never went back down, it just continued to rally relentlessly.

See, thats the advantage of having a systematic model: we follow the model, we follow the data, and the model said to stay risk on throughout and as a result we had an amazing year. To be honest, if we didnt have that model to follow behaviourally, we probably would have also said, Hey, we should trim our position on the way up because theres a lot of uncertainty out there regarding the pandemic and COVID, but you know the model had it right, it stayed fully invested on the on the way up. So for us, the great COVID pandemic of 2020 turned out to be a great example of market timing and the systematic approach that takes away the discretionary and the emotional biases that we all face. Thats why we built this model as systematic, without any emotional bias and without interference, so that we are hopefully able to produce returns year in and year out. Matthias Knab: How is the strategy expected do in rising interest rate environments? Heeten Doshi: Thats a question that we get a lot! Our strategy is primarily an S&P index strategy and so people ask how would it perform in a rising rate environment? The way we look at it is that investing in treasuries is a hedge against equities, its a view on being risk off. So we are not taking a view on treasuries or on where interest rates are going, we are using it as a hedge. We also have stop losses underlying the strategy. Even in the beginning of 2020 when interest rates were already very low when the 10-year was 60-70 basis points, it went down to 30 basis points. I mean, if theres a reason for the market to be risk off, interest rates will continue to go down, no matter how low they already are. So we are not taking a long-term view on treasuries, they are a week to week hedge in a risk off environment. The core of our strategy and our performance engine is really our capability to focus on where the S&P is going, not where rates are going.

Heeten Doshi, CFA will be a featured speaker at the interactive Small Managers - BIG ALPHA Episode 4 webinar on October 21st. Register here for his detailed presentation, with Q&A: https://www.opalesque.com/webinar/ You will be able to tune in to this webinar from any computer, tablet, or smartphone. The webinar will be recorded - in case you are not able to join, all registered participants will be provided a link to replay the webinar. | ||||

|

Horizons: Family Office & Investor Magazine

Market Timing: Defying conventional wisdom |

|

{kind=link}