|

Matthias Knab, Opalesque for New Managers: Robert Rubinstein built TrustVC.org after years of watching fake VCs, data-room poachers and phantom family offices abuse founders with impunity. Now he wants the industry to fight back.

Read on to discover the three crucial questions every founder must ask before a single meeting, and why shifting the narrative around bad investment practices is essential for the future of fundraising.

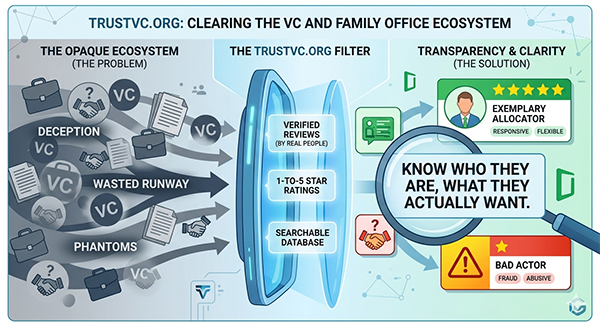

Every investor screens deals. Most will say no far more often than yes - that is not just acceptable, it is how the industry is supposed to work. What is not acceptable, says Robert Rubinstein, is the significant number of people operating inside the VC and family office ecosystem who were never legitimate investors in the first place: deal packagers misrepresenting themselves as principals, data-room tourists mining proprietary information, conference-circuit phantoms with no capital and no intention of deploying any, and outright fraudsters using term sheets as marketing tools while founders burn through their runways waiting for cheques that never come.

"It's not a problem if an investor says, I'm sorry, it's not for me, I don't want to invest, I think it's too risky," Rubinstein told Opalesque. "That's a legitimate answer. The problem is a different game altogether - one where people are not being honest about who they are or what they actually want."

Rubinstein has spent three decades educating asset owners and fund managers about sustainable investing and helping raise capital for funds, fund-of-funds, and direct deals. Over those years, the abuse he witnessed accumulated to the point where he decided to create a structural response: TrustVC.org, a not-for-profit investor review platform modelled on Glassdoor. Any founder, emerging manager, or LP who has dealt with a VC, private equity firm, or family office can post a verified review. The site checks that reviewers are real people, not bots, and allows the community to rate investors from one to five stars - surfacing both exemplary allocators and bad actors in a single searchable database.

Abuse that costs founders years - and leaves LPs in the dark

The damage done by bad actors is not limited to wasted meetings. Rubinstein draws a sharp distinction between the honest rejection - which costs a founder an afternoon - and the sustained, deliberate engagement by someone who was never going to invest and knew it from the start.

"Some investors are not really interested. They listen to a pitch because they need to write a report about the industry and want free advice. Or they've already invested in a competing company and want to benchmark their bet. There are far too many fund managers who have never run a company in their lives, who have no idea what it means to make a payroll - and they are quite abusive with other people's time because of it."

The injury extends well beyond the founders themselves. LPs, Rubinstein argues, are the industry's most systematically underserved constituency. "The greatest disservice is to the LPs. They invest in these funds and they never hear about all of the companies that were rejected. They just either get a check or they don't. Every month they're paying a 2% fee, whether money is deployed or not."

He argues that LPs should demand that fund managers publish a full account of every deal reviewed and rejected - with reasons. "I want you to publish a report of all of the companies you rejected, how you rejected them, and why. You'd see a lot of them say, oh no, we don't have time. Yeah, but you're using my money."

The wider context, Rubinstein notes, makes the abuse even harder to excuse. With global wealth estimated at roughly five times global GDP, there is no shortage of capital chasing good deals. Founders with genuinely compelling propositions have more negotiating power than they typically exercise - and far more choice of investor than they tend to realise. "There's five Swiss francs chasing one Swiss franc. People are very abusive in that context."

The taxonomy of bad actors

TrustVC.org was built in part to document the various models of extractive or fraudulent behaviour that Rubinstein has catalogued over his career. He identifies several recurring archetypes.

The term-sheet fraud. Among the most egregious cases documented on the platform is a fund manager who signed a term sheet with a healthcare and healthy lifestyle company. The company, believing investment was imminent, began spending against the anticipated funds. The money never arrived. The company eventually went bankrupt. "That fund manager never had the money," Rubinstein said. "They used the term sheet to promote their fund and attract LPs, listing the company as a portfolio holding when it was nothing of the sort." The fund manager initially denied the account; Rubinstein tracked down the company's CEO directly, who confirmed every detail posted on TrustVC.

The fake multi-family office. A second pattern, particularly prevalent in Switzerland according to Rubinstein, involves organisations claiming to represent family office capital. "They pretend to be a multi-family office, look around for deals, get into data rooms, collect that data to build up their knowledge base, and then shop around among families they actually know - hoping to earn a finder's fee as an intermediary." The problem is not acting as an intermediary, Rubinstein clarifies - it is falsely representing oneself as a principal with discretionary investment authority.

The conference circuit phantom. A third type attends family office events - name-dropping foundations, endowments, and philanthropic mandates - purely for social access. "They say, I have this big endowment, we want to invest in education in India. There was never any money. In Switzerland, if you're a foundation, you're supposed to publish your annual report online. They never did. It was just a way of toasting with champagne at family office events." Rubinstein notes a reliable heuristic here: "The ones really doing the most talk the least. The ones doing the least talk the most."

The sustainability greenwasher. Rubinstein reserves particular criticism for what he calls the "Impact Mafia" - fund managers who brand themselves around climate or sustainability while making no genuine effort to align investments with those goals. He cites a major European fund manager's now-deleted SDG reporting exercise, in which a mid-market mortgage product for Swedish consumers was classified as contributing to poverty elimination, and oil-sector turbines were counted toward climate action. "You want to be part of a fitness club of sustainability, but you don't want to do the exercise. You just want to show everyone your membership card." The deleted reports, he notes, remain visible via the Wayback Machine.

How to use TrustVC.org - and the three questions every founder must ask

The platform allows users to search for any VC, private equity firm, or family office, filter by star rating, and browse by sector. Rubinstein walks through a live example: APG, one of the world's largest pension funds with roughly 500-600 billion euros in assets, earned a strong rating after creating a dedicated vehicle that invested as little as 3-6 million euros into early-stage European decarbonisation companies - a level of flexibility unheard of for an institution of that scale. "Size has nothing to do with social skills," Rubinstein observed. "Some of the biggest fund managers I know - General Atlantic, for instance - were always very responsive. This is not a size issue. It's a character issue."

Beyond the platform, Rubinstein offers founders and emerging managers a simple three-question framework before engaging with any investor:

One: Do you actually have money? The question sounds blunt, but Rubinstein says it is asked far too rarely. "How many times have you met somebody who claims to be super rich and they're just frauds?"

Two: Have you invested in this space - in the area where I operate? Establish whether the investor has any genuine track record in your sector before investing further time in the relationship.

Three: Where exactly have you invested in this space? Get the names of specific portfolio companies, then contact them directly. "Contact those companies to find out: is this fund manager or this investor a good partner? Because, as you know, it never goes according to plan."

That last point is the real test. Rubinstein is not asking whether the investor made money - he is asking what kind of partner they were when things got difficult. "It's always worse or better than expected. If it's worse, will your investor help you dig out of the hole, or will they run you over?"

He also offers a more fundamental piece of advice: delay external fundraising for as long as possible. "Even though raising money is our main business, I tell all startups: don't raise money. Bootstrap as long as you can physically do it. People completely underestimate the time it takes - researching, finding, contacting, meetings, follow-up meetings, due diligence, paperwork, legals, investor relations, and then finally getting rid of them."

Building the database - a call to action

Rubinstein is candid about TrustVC's current constraint: the framework exists, but the reviews must come from the community. He cannot write them himself - only those with direct experience can post. "I had a founder in Latin America who'd built a social enterprise providing healthy food at 25% lower cost in favelas, raised $20 million, had plenty of terrible investor stories to tell - and he never posted a single one."

The hesitancy to go public is, in his view, largely irrational. Founders fear that posting a negative review will cost them future investment. "What, that they're not going to invest in you? They're not investing in you now. If an investor won't fund you because you told the truth about a bad actor, they were probably not the right partner."

He argues it does not take a large volume of reviews to shift behaviour. "It doesn't have to be 100 reviews per fund. It has to be only a couple of reviews to start people to rethink - should I really approach this firm?"

The platform can be accessed at TrustVC.org.

See also how the industry is discussing this problem with 30+ comments and re-posts on LinkedIn.

|

RSS

RSS

{kind=link}