|

Matthias Knab, Opalesque for New Managers:

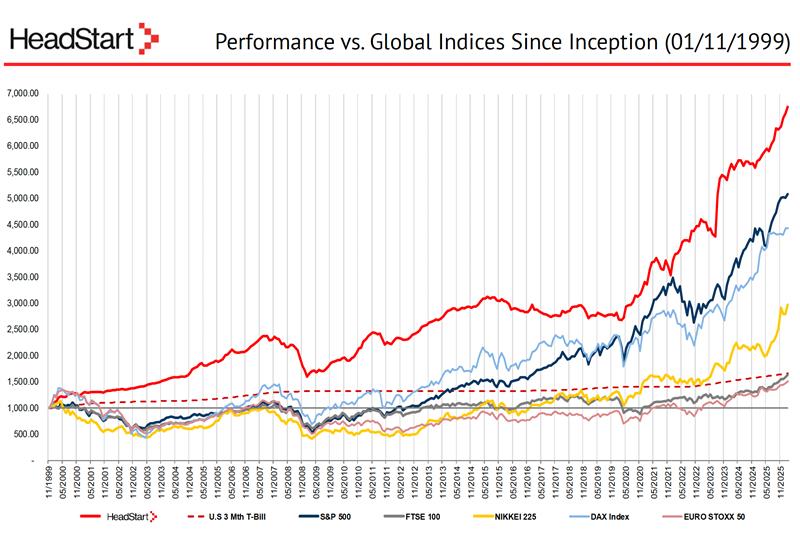

Najy Nasser and Henry Watkinson of London-based HeadStart Advisers explain how their fund of hedge funds has evolved into a high-conviction, alpha-centric vehicle - one that was up in both March and April 2020, outperformed the S&P 500 by more than 40 percentage points in 2022, and continued to prove its defensive construction during the Liberation Day sell-off of 2025.

Going a bit further back, the HeadStart Fund of Hedge funds has almost tripled the HFRIFOF Index (312% vs. 112%) since 2009. Not only that, this fund of hedge funds also comfortably beat the single manager index HFR Fund-Weighted Composite Index (HFRIFWI): 312% vs. 188% over all those years.

Matthias Knab: Let's start with something fundamental. When institutional investors hear "fund of hedge funds," many still carry a mental image from before the financial crisis - slower, less transparent, burdened by a double layer of fees and liquidity lag. How has your model evolved, and is that picture even accurate anymore?

Najy Nasser: The line between a fund of hedge funds and a multi-strategy fund has blurred considerably. Both structures add value, what really counts is how you do it: how you select the managers, how you combine them, the risk management, the allocation style, and the leverage you end up using.

One thing worth noting on liquidity is that the perception has actually reversed. For instance, we offer monthly liquidity with 65 days' notice, while some of the major multi-strategy platforms have increased lock-ups anywhere up to five years. So the age-old argument that funds of funds are the illiquid option no longer necessarily holds true.

Henry Watkinson: That's right. Multi-strats have significantly less favorable fund liquidity terms now. We know of several with up to five-year locks. That's a pretty important distinction - and it tends to get overlooked in the conversation about the two structures.

Matthias Knab: On the transparency side, multi-strategy funds obviously have an edge through separately managed account structures. Is that something you're working toward?

Henry Watkinson: We're not at the SMA scale yet, so we can't offer the same look-through that the multi-strat platforms provide. But that's actually one of the things we want to grow into. And interestingly, the SMA question touches on a big shift we've seen in the industry. Ten years ago, managers would launch a fund first and then develop SMAs on the back of their track record. Now it's the complete opposite - the SMA comes first, and the fund launches second. The institutional capital is there from day one, which puts the manager on firmer footing when they do launch, and makes them more willing to offer generous founder share class terms when they launch funds.

Matthias Knab: You mentioned founder share classes. Can you explain how significant that is in practice for your investors?

How A Fund of Funds Can Reduce Costs For Investors

Najy Nasser: It's very significant. When you invest early in a manager's journey, you typically secure discounted fee arrangements - lower management fees, lower performance fees, or both. In a normal year of performance, our entire management fee at the fund-of-funds level is effectively covered by the fee savings between those founder or seed classes and what an investor would pay going into the same underlying funds at standard terms today. So the double-fee argument evaporates pretty quickly when you look at the actual numbers.

To give you a rough sense of scale: approximately 45% of our portfolio by AUM is invested in funds that are now closed to new investors. Around 65% of our positions have these attractive founder or early-bird share classes. Investors coming into our fund today inherit both advantages - the access and the economics.

Henry Watkinson: The compounding effect of better fees over a number of years is substantial. We have several funds where the fee advantage over what's available to new investors today is meaningful enough that it drives material outperformance on a compound basis over time.

Matthias Knab: And the access to closed funds is equally important - because it can't simply be replicated by an SMA arrangement?

Najy Nasser: Exactly. Many of the underlying hedge funds in our portfolio are closed to new investors. We can get capacity for our fund, in many cases on a best-efforts basis, because of the relationships we've built over many years. Whether those managers would accommodate a separate investor with their own SMA - that's a different question entirely. So there's a genuine structural advantage to investing directly in our fund, not just a fee story.

We've had a recent example where a manager launched with an initial founder share class target of $100 million. Because of the pedigree and the following that came with it, the founder class was oversubscribed to $400 million and is now closed. That entire class filled in the first two months.

Matthias Knab: Let's talk about portfolio construction. What types of hedge fund strategies do you focus on, and how do you think about building the overall portfolio?

Najy Nasser: We focus on true alpha-centric hedge funds - strategies where the manager is genuinely running a balanced book, not simply carrying significant market beta. Most of our long-short equity managers operate within roughly plus or minus 30% net exposure. It follows something like a distribution curve around that midpoint, with some on the fringes, but the core thesis is that these managers can navigate both sides of the market rather than riding a long bias.

On the credit side, all of our positions have some form of hedging. That might be long-short credit, long credit versus short equities, or more sophisticated derivatives-based hedges. The entirety of our credit book is hedged.

Then we have dedicated convexity positions - strategies specifically designed to generate returns in dislocated or sell-off environments. These tend to be long-volatility by nature. And we have a range of uncorrelated strategies: capital structure arbitrage, various forms of event-driven, and global macro.

Our global macro managers are particularly sophisticated in how they express their positions. They work predominantly through OTC options rather than standardized futures contracts, which lets them avoid the crowded maturities you see in listed markets and position across the full volatility surface - finding the most attractive points across that surface rather than being forced into the benchmark expiries.

Henry Watkinson: The portfolio currently holds 34 underlying positions. It's a concentrated, high-conviction book - not a diversification exercise for its own sake.

Matthias Knab: You also use leverage. How does that interact with the defensive positioning you're describing?

Najy Nasser: The leverage is deployed specifically for the convexity and uncorrelated positions. When we last reviewed this, more than our entire leverage allocation could be attributed to positions that would either perform well in a market shock or would be genuinely uncorrelated to directional moves. So rather than amplifying risk, the leverage is essentially funding the defensive layer. We only charge management fees on the equity, not on the levered notional, which is important context for investors thinking about the fee structure.

Matthias Knab: How has that construction performed when it's been genuinely tested?

When Real-World Stress Tests Result in Outperformance

Najy Nasser: The real-world stress tests have been the most instructive. During COVID, we were up in both March and April 2020. That combination was genuinely rare - the violent reversal in April caught many managers who had profited from the initial sell-off. We navigated both months positively, before the broader market recovery that benefited almost everyone in the second half of the year.

In 2022, we ended the year up over 20%. We outperformed the S&P 500 by more than 40 percentage points, the Nasdaq by more than 50 percentage points, and we outperformed both the Bloomberg US Aggregate Bond Index and the fund-of-funds indices, which were themselves down on the year. At year-end we had 29 underlying positions, of which 18 were positive.

And in 2025, the notable moment was during the Liberation Day sell-off. At the lowest intraday point in the markets, we were up. Most hedge funds escaped any real scrutiny because markets recovered by month-end, making April look like a quiet month. But we know what happened underneath. Our portfolio construction was stress-tested again - and held.

So if you look at the significant market dislocation events over the past six years - COVID, 2022, and the Liberation Day period in 2025 - we have a clear empirical record across all three.

Matthias Knab: What's your process for finding managers early? And what does due diligence look like when you're investing day one into someone who doesn't yet have an institutional track record?

Najy Nasser: The first thing to understand is that we're not looking for genuine startups in the conventional sense. The managers we back day one have typically been running $1 billion or more at a major multi-strategy firm, or running a proprietary trading book at a major bank - often with 10 to 20 years of verified performance history. The investment strategy risk is close to nil. What you're underwriting is the business risk of the new vehicle, not the question of whether this person can generate alpha.

When those managers launch independently, they usually have enough personal capital to run the business for several years while they build assets. The AUM risk is minimal. And because they want to launch their own fund - not just manage an SMA where their name isn't really on the door - they tend to offer attractive founder share class terms to early backers who help them get established.

Henry Watkinson: Skin in the game is non-negotiable for us. If a manager worth a significant amount of money hasn't put their own capital into their own fund, that's a red flag we won't look past.

Najy Nasser: And we check references through our own network rather than through the references the manager provides. We speak to people in adjacent areas of the market who know this person's work - colleagues from previous firms, counterparties, people who've sat across the table from them. That gives us colour that a standard reference check won't reveal.

Governance: More Than A Nice-To-Have

Matthias Knab: You practice what you preach on governance. Can you explain your approach to independent oversight?

Najy Nasser: We've had a fully independent board of directors since our launch - something that used to be more the exception than the rule in this industry. The majority of hedge funds used to have managers sitting on their own boards, which fundamentally undermines the governance function.

The value is partly what I'd call proving a negative - it signals to our shareholders that there is an external check on management decisions that doesn't report to us. But there's also tangible practical value.

Henry Watkinson: One of our independent directors has a non-executive role at a fund administration firm. When we were reviewing our administration costs, he was able to benchmark us against current market pricing and suggested we go back to our existing administrator for a reprice. We did - without switching - and brought the cost down significantly. That kind of external intelligence pays for itself.

And historically, if you look at the funds that suffered the most severe blow-ups in 2008 - not the 20-30% drawdowns, but the genuine blow-ups - an unusually high proportion of them didn't have independent boards. That's not coincidental.

Matthias Knab: How do you think about portfolio turnover and ongoing management of the allocations?

Najy Nasser: We think about it in two layers. There's the binary layer - funds in, funds out - and there's the micro-adjustment layer, where we increase or decrease allocations to existing positions based on our macro view, which we build through close dialogue with our underlying managers. They have real-time information on pricing and opportunity sets in their specific areas. That intelligence feeds our allocation decisions.

Our turnover is elastic in both directions. We don't need to exit a fund in order to add a new one. If something meets our high bar and we have conviction, we add it and let the portfolio grow. Conversely, if a fund crosses one of our triggers - it's getting too large, or there's style drift, or something in the team or process changes adversely - we'll exit without waiting to find a replacement. We're not managing to a fixed number of positions.

Investors Rediscover Hedge Fund of Funds

Matthias Knab: Where does the investor base stand today? Is the reawakening of interest in hedge funds and funds of hedge funds you've observed translating into real allocator engagement?

Najy Nasser: We're seeing a slow but real evolution. Until around 2022, it was difficult to get a serious conversation with many investors. And the reason for that was entirely rational - hedge funds struggled throughout the QE era, and the reasons are worth understanding rather than dismissing.

Quantitative easing created two structural headwinds for hedge funds. First, the Fed put crushed volatility, which compressed the trading ranges available to long-side strategies. Active managers had less room to work with. Second, zero interest rates removed the natural catalyst for short ideas - companies with weak fundamentals could refinance indefinitely at trivial cost, so short theses stopped resolving. Both legs of a long-short book were impaired at the same time.

Once we returned to a normal volatility environment - really starting with COVID and accelerating through 2022 - alpha-focused managers started performing again. And allocators have slowly begun to update their views. We're seeing genuine reawakening since 2022.

What we still encounter, though, is what I call the Groundhog Day problem. There are investors who repeat the same 2008 narrative, apply it to the entire hedge fund universe without differentiation, and don't want to reassess. But that cohort is shrinking. A new generation of allocators is coming to the fore - people who weren't in the industry in 2008, who are more open-minded about the data, and who evaluate funds on their actual characteristics rather than category.

The Art of Getting There First

Matthias Knab: Last question: what advantage does being an early-stage investor provide beyond the fees and access you've described?

Najy Nasser: The relationship. Being there from day one builds a loyalty that you simply cannot buy into later. Many of the managers in our portfolio today - who are closed, who are hard to access, who are selective about the capacity they share - we were there when they needed support most. That translates into transparency, into preferential capacity treatment, and into an alignment of interests that a new investor entering at scale can't replicate.

There's also an academic point worth noting. Research consistently shows that alpha generation is highest in the early years of a fund's life, precisely because smaller AUM allows the manager to trade across market caps, move quickly, and exploit opportunities that become unavailable as the asset base grows. At a certain scale, the fork in the road appears - does the manager optimize for performance, or for building a large fee-generating business? Getting in before that fork means you're fully invested during the highest-alpha period, and you have the relationship to understand which direction they're likely to take.

For us, it's not about investing in startups for the sake of it. It's about being there for the journey - and building a portfolio where 26 years of relationships with the best managers in the market translate into returns that investors simply cannot access any other way.

|

RSS

RSS

{kind=link}