|

Parsa Kiai Opalesque Geneva: Most hedge funds lose money short selling or don't generate alpha - diluting returns, increasing volatility, or failing to capitalize on declining stocks. Earlier this year, the Financial Times wrote: "Even established short sellers such as Enron's foil Jim Chanos have thrown in the towel. Trying to call out bad behaviour when the stock market is hitting new highs is a little like entering a party and telling everyone to turn down the music. No one wants to hear it."

"All of us are figuratively speaking looking into the abyss," one prominent short seller told the paper. "All of the short sellers are at each other's throats on Twitter. I equate it to playing the fiddle while Rome is burning."

Short-selling is difficult, out of favour, faces academic and practical challenges, and has few practitioners remaining.

Yet Steamboat Capital Partners, a New York-based investment manager founded in 2012, has consistently generated alpha from its short book, proving that well-researched short positions can still deliver alpha.

Steamboat Capital Partners Fund, LP is an opportunistic, fundamental, value-oriented investment fund focused on a long portfolio of undervalued and catalyst-driven investments. It applies an event-driven investment philosophy, principally in listed equity and debt securities, with a focus on capital preservation and alpha-oriented short-selling. The manager seeks to minimize risk by investing with a margin of safety and achieve low-correlation with conservative portfolio positioning and active short-selling. The fund has annualised 11% over the last 13 years, with a correlation to the S&P 500 of 0.29, according to documents seen by Opalesque.

CIO Parsa Kiai, who has 20 years of direct investing experience and a majority

of his liquid net worth invested in the Fund, will present his case on the world of short-selling in an Investor Workshop webinar on September 9th (details below). Meanwhile in this interview, he explains why shorting in general can be a losing game, and the current opportunities as he sees them.

Opalesque: Why is shorting a losing game?

Parsa Kiai: Short selling has always been difficult because of:

(a) unfavorable asymmetric risk reward,

(b) natural tendency for markets to go up and

(c) the incentives of management teams, regulators, insiders and policy makers to prefer markets going up instead of allowing short-sellers to point out misconduct and assist in policing wrongdoing.

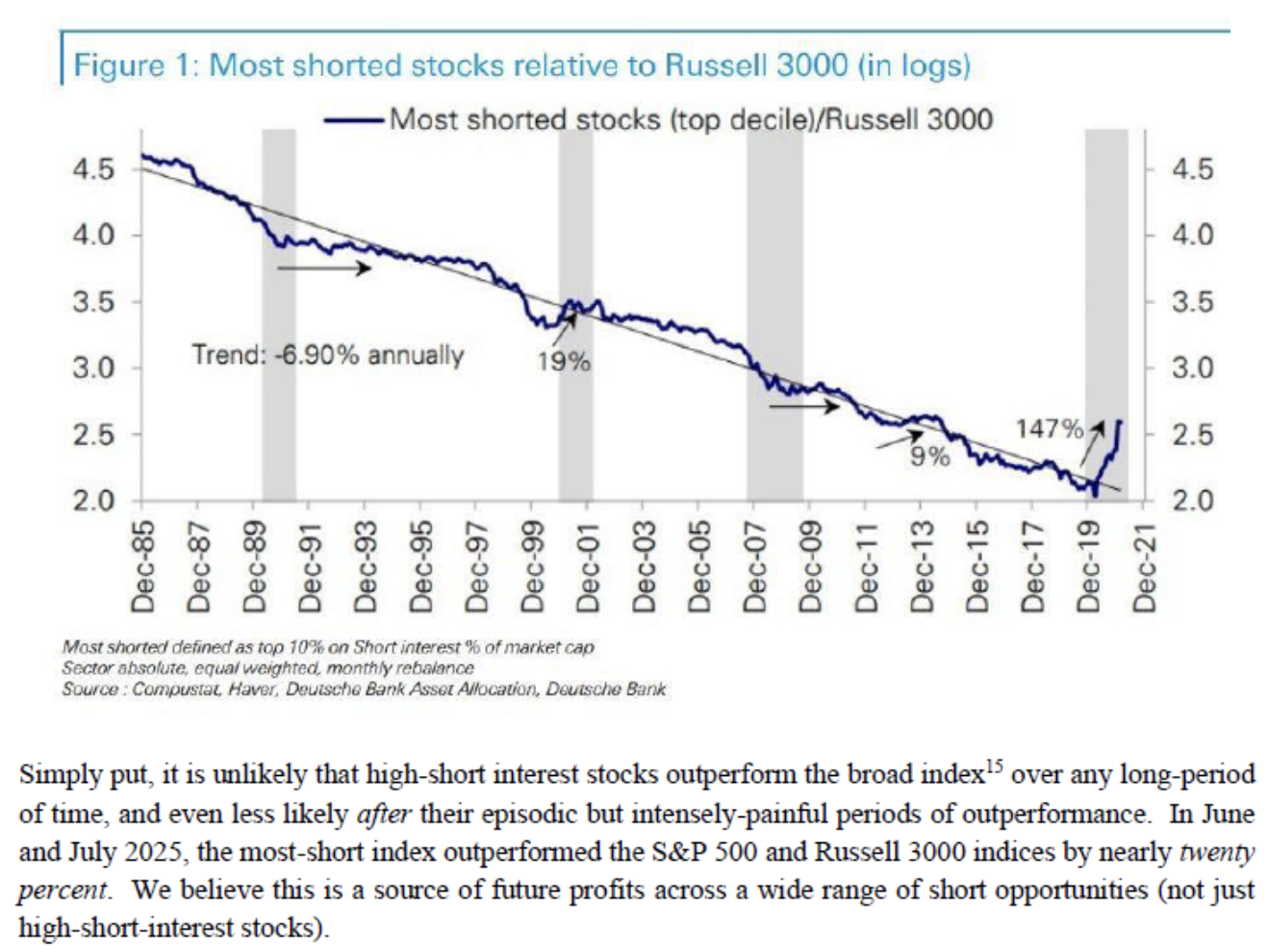

Furthermore, it is well documented that short-selling has been challenging since the 2008 financial crisis because of persistently low interest rates and exceptional returns within the equity markets during that period, with brief interruptions during COVID in 2020, the 2022 bear market, and the 2025 tariff sell-off. For the better part of 15 years, investors have given up on short selling.

Opalesque: What are the long and short opportunities that you see?

Parsa Kiai:

Partly because so many people have given up on short selling, we think there's some opportunity in conducting active short-selling, especially if it is paired with a well-crafted long portfolio in a long/short strategy. Right now, we think there are exceptional medium-and-long-term opportunities in the short market because of how frothy markets have become, in both mundane businesses as well as among highly shorted stocks.

Here is an excerpt from our upcoming 2Q letter:

We also believe there are very good opportunities on the long side and generally, in higher interest rate environments, the opportunity for profits among long/short strategies is actually the highest:

Throughout our history, we have had very good long/short alpha generation, even during this period of low interest rates and extremely difficulty in shorting - so we believe that the next few years are likely to be even more fruitful.

Opalesque: How does an event-driven, catalyst-based approach differ from generic short-selling?

Parsa Kiai:

While we have a broad approach to short-selling, catalyst-driven shorting is productive because it controls one of the most important factors in shorting: timing. Sometimes, the longer the short investment time horizon, the more opportunity for something to go wrong, either because management desperately tries to do something and perhaps it goes right, or the company gets lucky, or the market moves substantially.

With a specific catalyst, you can mitigate that risk. These catalysts include:

• Dividend reduction/eliminations - such as the shorts we had in Cable One (CABO), Xerox (XRX), and Medical Properties Trust (MPW)

• Balance sheet restructuring - such as Wolfspeed (WOLF) shorts

• Litigation / legal catalysts

• And a host of others.

Opalesque: How do you detect mispricing and a resolution?

Parsa Kiai:

We use many techniques, but it includes (a) screening, (b) opportunistic, ad-hoc origination, and (c) relationships. We look for many things including unsustainable dividends, over-levered balance sheets, hidden liabilities, deceptive management teams engaging in fraud or aggressive accounting and more traditional factors such as secularly declining or zero-terminal-value business models.

Opalesque: Why is value investing a good investment opportunity now?

Parsa Kiai:

With 4-5% interest rates, there is very good alpha generation in a long/short strategy. In addition, investing in genuine value investments made up of well-capitalized, quality businesses with good management teams at attractive valuations is even more attractive today for several reasons:

• Less competition from marginal players as the cost of capital is higher and strong incumbents can better withstand any challenges

• Less competition from private equity for M&A

• The simple math of a discounted cash flow (DCF) analysis is more attractive for near-term cash flows versus distant terminal values with 4-5% risk free rates - so boring cash-generative companies with good capital allocation are much more valuable than cash-burning distant growth stocks.

Upcoming webinar:

In this exclusive Investor Workshop, Steamboat Capital Partners' Parsa Kiai (Founder & CIO) and Farhad Dalvi (Director of Research) will share key insights on short selling.

Free registration: www.opalesque.com/webinar/

|

RSS

RSS

{kind=link}