|

Clark Nicholls B. G., Opalesque Geneva for New Managers: Now is a good time to take advantage of the inefficiencies of the credit market, according to a London-based portfolio manager who is launching a European long/short credit hedge fund.

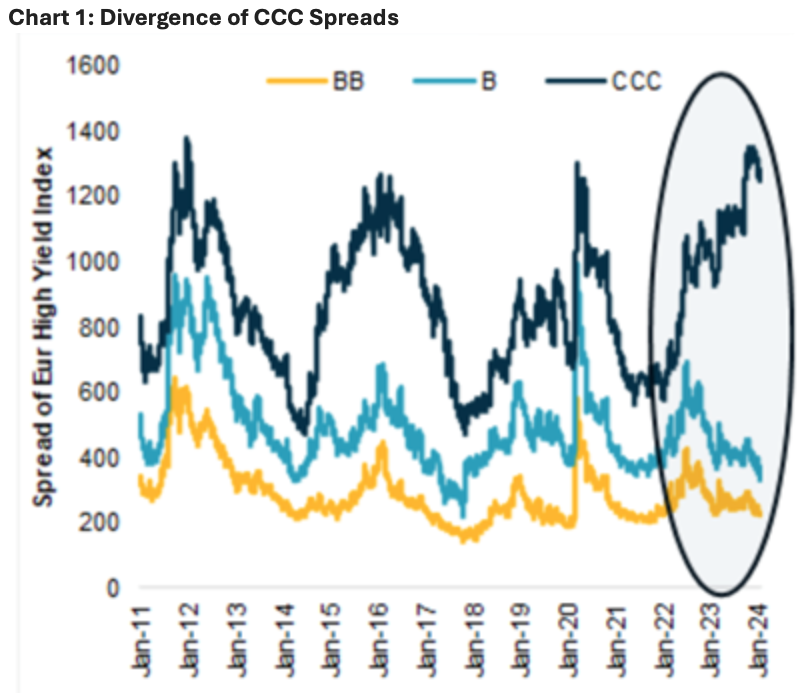

The market opportunity comprises three factors, according to Clark Nicholls, who spoke with Opalesque. Firstly, even though market spreads are at normal levels, there is an unprecedented yield dispersion between weaker CCC-rated credits and better B and BB credits (chart 1). Therefore, conducting a thorough credit analysis to distinguish healthier companies in the stressed space can create greater opportunities than in past markets.

Source: Aucit Investment Management

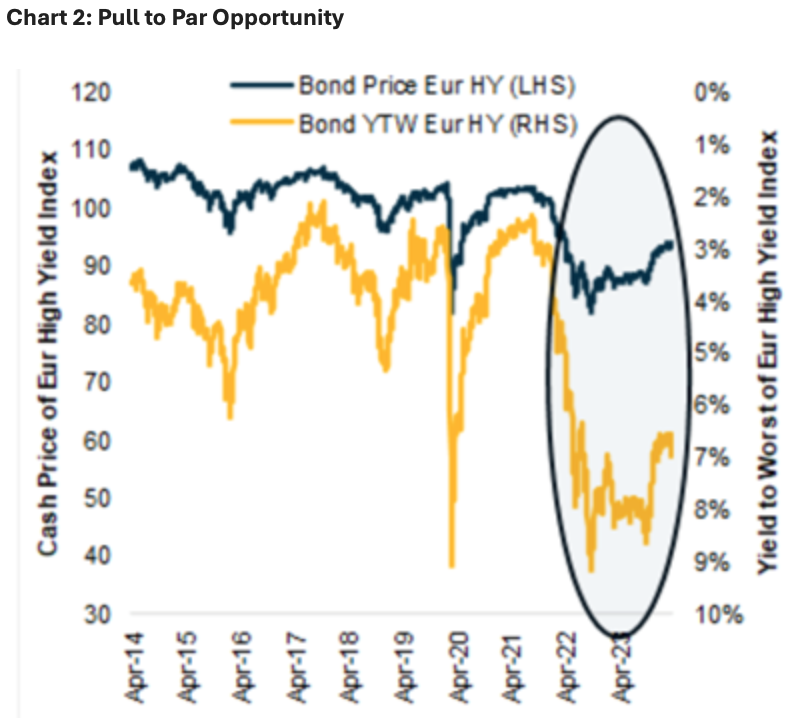

Secondly, there is a pull-to-par opportunity due to the higher interest rate environment, as many bonds have yields much higher than their coupons (chart 2). "In other words, a bond with a very low coupon can only have a higher yield if the bond price is low. So, you get a big 'jump to par' when the bond is repriced for a par refinancing."

Source: Aucit Investment Management

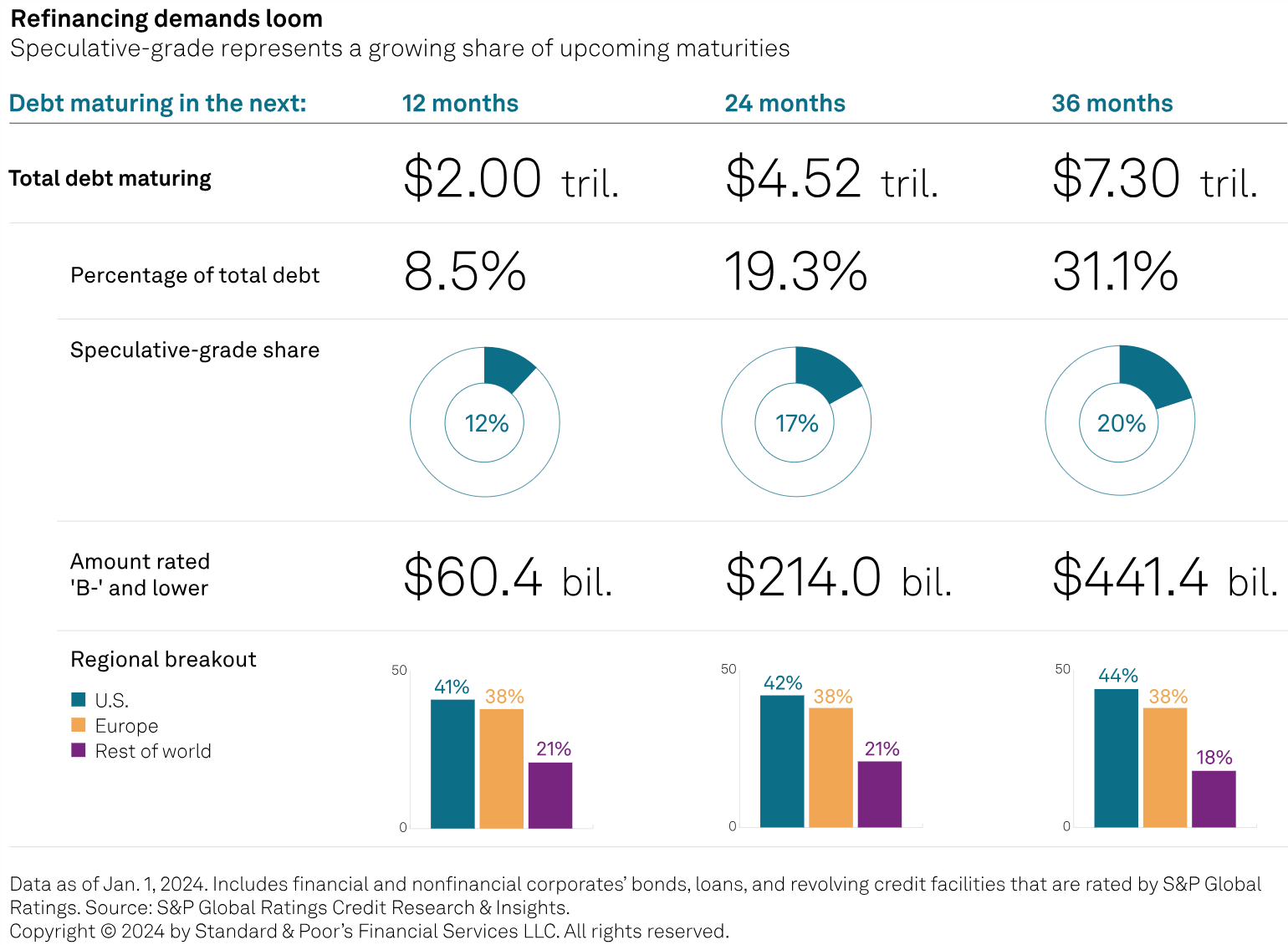

The third opportunity is the near-term maturity wall (illustrated by a bar chart showing yearly buckets when all bonds are due for repayment). For instance, $60.4bn of 'B-' and lower-rated debt is set to mature in 2024. These factors, a weakening economic outlook, and dislocated markets create long and short investment opportunities.

Source: S&P, Feb. 2024

Clark Nicholls, an award-winning bond researcher and portfolio manager, developed and led similar strategies to his new fund at AXA Investment Managers, where he helped raise over €3bn in assets under management and achieved high single-digit returns from 2016 to 2023. His edge stems from his extensive experience. "I've been fortunate to work with some great teams where we achieved exceptional investment performance. I'm employing strategies learned from both the sell and buy side, capitalising on the market's richest alpha opportunities."

Innovative credit strategy

The new fund, Aucit Investment Management, runs a long/short relative value credit strategy focused on short-duration high-yield bonds. These bonds pay higher interest rates because they have lower credit ratings than investment-grade bonds. Analysis indicates that the short-duration high-yield asset class offers the best yield per unit of risk relative to all other fixed-income asset classes. This is because, in addition to higher returns, it has half the systematic volatility. At the idiosyncratic level, the fund generates alpha from fundamental analysis as well as opportunistic and technical trading. It targets pure alpha of 6% above the risk-free rate and aims for returns consistently above 10%.

"The strategy itself is quite unique and innovative," Nicholls says. "We look to source alpha both at the portfolio design level and from single security positions. For instance, we source alpha by ensuring the short-duration high-yield bond risk is fully hedged-having zero duration time spread by shorting longer-duration 5-year CDS. This maturity curve 'free lunch' allows the fund to receive 60% of the market returns without systemic risk. Another rich source of alpha is opportunistic and technical trading at the security level, such as refinancing, new issues, rating changes, and earnings surprises. These differentiated solutions also work particularly well in higher interest rate environments."

The launch target is over €100m ($108.6m) in gross exposure, and the investment vehicle can use SMA Segregated Mandate, UCITS, and Cayman formats.

Trends in credit and multi-manager funds

His launch is part of a trend in the establishment and growth of credit hedge funds, Nicholls explains. Credit long-short strategies - positioned between distressed and investment grade-styled absolute return funds - have not been a part of the hedge fund universe, unlike equity long-short strategies which historically covered about 60% of all strategies. However, these equity strategies have decreased to about 40% of the hedge fund market, primarily being replaced by multi-managers. Credit long-short strategies now cover about 5% of the universe, and Nicholls expects them to grow further.

"Equity markets are becoming more efficient, while credit remains fairly inefficient - particularly within sub-investment grade and outside the US. For example, Trade Reporting and Compliance Engine (TRACE) currently only exists in the US high-yield market, and the European high-yield remains an over-the-counter market. There remains ample opportunity in the credit hedge fund space."

Another trend Nicholls has observed is the improved quality of operational fund platforms, which leverage technology to partner with new fund managers. It has become cheaper and more efficient to launch funds with institutional-quality operations and oversight.

Additionally, this same technology has led to significant and conspicuous growth in the multi-manager model. Multi-manager platforms enjoy greater scale from technology and cheaper funding costs due to strict risk parameters. These platforms employ many specialised hedge fund managers and strategies, collectively operating as one entity where individual units have discrete P&L responsibilities.

***

The HFRI Relative Value (Total) Index is up 2.8% YTD after a flat April, and up 8% in the last 12 months. The Eurekahedge Structured Credit Hedge Fund Index is up 4.2% YTD after returning 1% in April - and 10% in 2023.

|

RSS

RSS

{kind=link}