|

Edouard Mercier B. G., Opalesque Geneva: The Asia equity markets have not been at their best so far this year, with the MSCI Asia index down almost 13% YTD, but many managers remain buoyant about the region, as indeed there are many enduring mispriced opportunities and they know where to find them: small and mid-caps.

Small-cap companies in Asia operate in a space that is relatively shielded from regulations designed to tame practices such as market dominance or monopolistic tendencies, according to PineBridge Investments. Small caps are also better equipped to deal with protectionism, as they are relatively more domestically focused or regionally oriented than large caps and thus less exposed to potential shocks to international trade.

The Asian small and mid-cap universe offers higher alpha opportunity, says Swiss bank UBS. As indeed, the small and mid-cap companies are under-researched by sell-side analysts, and this provides more opportunities to outperform by exploiting knowledge inefficiencies. Over the last 10 years, almost half of the fastest-growing Asian companies had very limited or no analyst coverage at all.

Asian public equity markets (notably mid and small caps) offer a deep pool of quality businesses trading at attractive valuations, says Ascender Capital, a Hong Kong-based investment boutique.

"With over 22,000 listed businesses across the region, our investment strategy has been designed to identify pricing inefficiencies systematically. These are primarily linked to a lack of sell-side coverage, increased retail participation, and a high level of family ownership. Two-thirds of Asian listed companies are family-owned, which is double the global average. We like to work with these long-term stewards; however, it can reduce a company's free float, meaning these unique opportunities are only accessible to smaller more capacity-conscious investment firms such as ourselves."

Ascender was founded in 2012 and manages a single equity strategy, which is available in long-only or absolute return versions. The strategy invests in high-quality businesses, defined by a track record of high returns on invested capital, earnings growth and profitability, trading at a significant discount to intrinsic value.

Before founding Ascender, Edouard Mercier was an entrepreneur in the telecom sector, an investor, and the co-founder of Piton Capital in 2009. He will present at the Small Managers - Big Alpha episode 9 webinar on July 7th.

Expect an additional tailwind

The Ascender Asia Fund is a long-only, Caymans-domiciled fund with a portfolio of 30 businesses. It has annualised 10% net since its inception in December 2021. It covers Asia including Japan and produces its returns from acquiring stocks at temporary discounts thanks to mispricing. The process mixes quantitative and qualitative phases.

The Ascender Global Value Fund (AGVF) has the same strategy but is long/short. It has annualised a net return of 7% since inception in December 2012 - compared to 6.2% for the MSCI Asian Small-Cap index and 4.8% for the HFRI Asia incl. Japan index.

The MSCI AC Asia Small Cap Index, which covers 2,400 constituents in three developed markets countries and eight emerging markets countries in Asia, was positive over the last couple of years. This year, however, it is down -13%, after flat returns in May. As for the HFRI Asia with Japan Index, it is up 0.9% YTD - and virtually flat in the last 12 months.

"Ascender Capital launched its strategy via an absolute return fund in 2012, providing investors with exposure to Asian equities while maintaining an ongoing focus on capital preservation," Mercier tells Opalesque. "The portfolio's short positions are comprised of index hedges, successfully reducing the impact of market selloffs (drawdown capture of 28% since inception) and delivering positive performance over every calendar year to date.

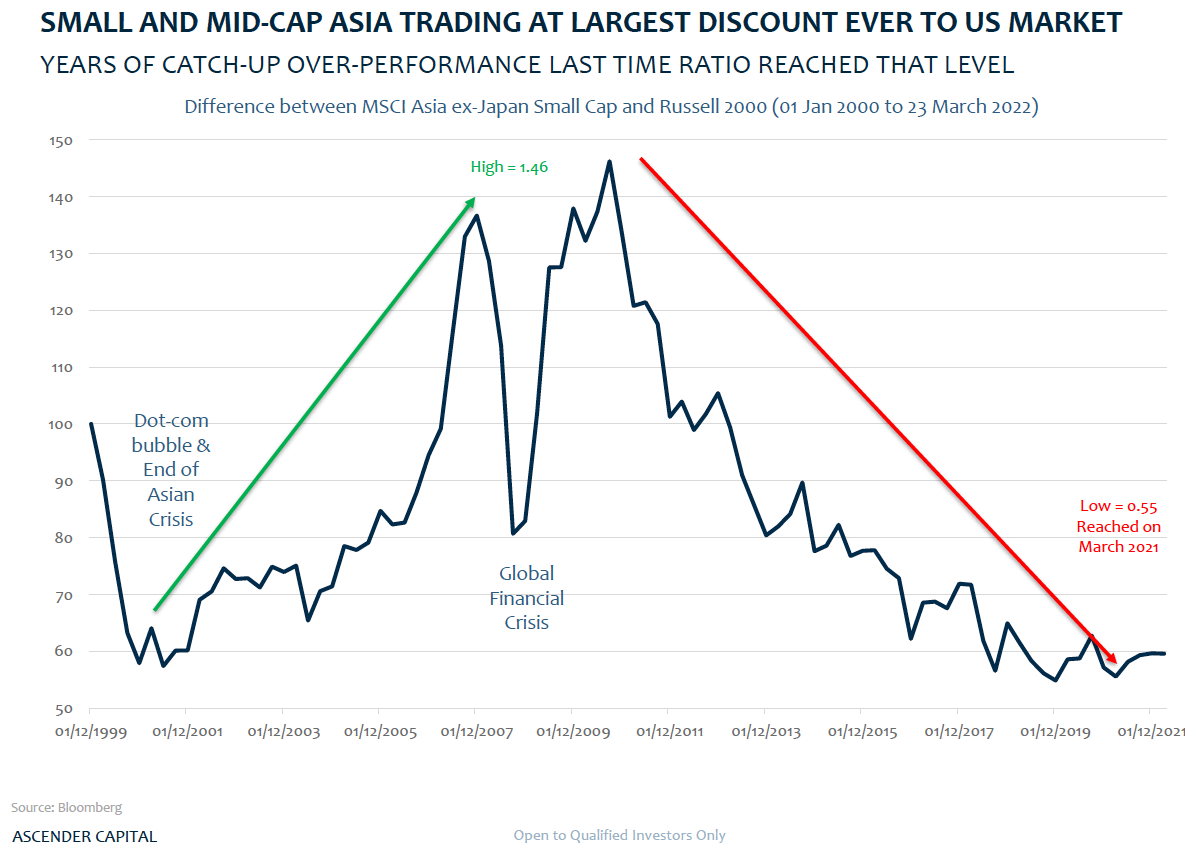

"Going forward, we expect an additional tailwind due to a narrowing of the discount between the US and Asian small caps, which is currently at an all-time high (see graph below)."

On a year-to-date basis, the hedge fund continues to significantly outperform its benchmark (-2.7% vs -13.1%) with the fund's short positions contributing positively (+6.1%), he adds.

When asked about the investment process which mixes quantitative and qualitative phases, Mercier explains that Ascender's bottom-up quantitative model allows the investment team to efficiently identify quality Asian companies (i.e. those with a track record of high returns on invested capital, seven years of earnings growth and strong balance sheets) that are trading at attractive valuations.

"From this high-quality universe," he continues, "the investment team then implements a rigorous checklist process (i.e. accounting forensics, corporate governance, etc.) to eliminate potential red flags and businesses that don't meet the internal criteria. An investment analyst then conducts a qualitative fundamental analysis on the shortlisted companies before force-ranking each new candidate against existing portfolio companies. This systematic discovery and force-ranking enable the team to focus on value-adding analysis."

Upcoming webinar:

Small Managers - BIG ALPHA

Episode 9 of this groundbreaking webinar series presents another carefully screened panel of investment managers. In one hour, you'll meet them all, get to know their top quartile strategies, and since this is an interactive session, you will be able to ask questions.

Edouard Mercier, Ascender Capital

Bastian Bolesta, Deep Field Capital

Gerald Balboa, Skylar Capital Management

Elias Nechachby, Icon-MoSAIQ-Carmika

When: Thursday, July 7th at 11am ET / 4pm UK time / 5pm CET

Free registration here: www.opalesque.com/webinar/

|

RSS

RSS

{kind=link}