RSS

RSS|

Forthcoming Rules Under EMIR on Dispute Resolution and Portfolio Reconciliation FROM DECHERT LLS's Financial Services GroupThe European Commission's regulation on clearing of OTC derivatives (EMIR) requires counterparties to OTC derivative contracts that are not cleared by a central counterparty to mitigate their trading risks by using a number of different techniques. The following rules come into effect : => The requirement for counterparties to agree arrangements for the reconciliation of their OTC derivative contracts. => The requirement for counterparties to agree procedures in relation to the identification and resolution of disputes1. The rules have "direct effect", meaning that local regulators are not required to implement the rules into their own rulebooks. Summary of the rules which come into effect

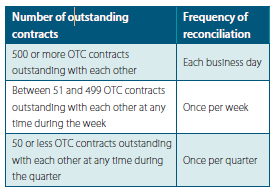

The rule on portfolio reconciliation requires counterparties to agree in writing a process for reconciling portfolios. The reconciliation must cover "key trade terms" and the trade valuation. The agreed process must be in place before entering into a derivative trade. The frequency of the reconciliation depends on the number of contracts outstanding between two counterparties. In the case of a financial counterparty (or a non-financial counterparty exceeding the clearing threshold), this is: The rule on portfolio compression requires counterparties with 500 or more OTC contracts to have in place procedures regularly (at least twice a year) to conduct a portfolio compression exercise. Portfolio compression entails terminating equal and offsetting trades with the same counterparty. It reduces the credit risk faced by each counterparty against the other, reduces fees associated with open positions and "cleans" the derivatives book. The rules on dispute resolution requires counterparties to have agreed detailed procedures and processes in relation to the identification, recording and monitoring of disputes relating to the valuation of the contract and the exchange of collateral, and to agree a process to resolve disputes in a timely manner with a specific process for those disputes which are not resolved within 5 Business Days. Financial counterparties must report to their regulatory authority any disputes in relation to an amount or value higher than EUR 15 million and which are outstanding for at least 15 business days. The FCA has provided guidance on this reporting obligation (see below). To whom do the rules apply? The rules apply to EU financial counterparties and EU non-financial counterparties (regardless of whether the non-financial counterparty exceeds the clearing threshold). Financial counterparties include broker-dealers, insurers, and UCITS funds established in the EU. Non-financial counterparties are any other type of undertaking established in the EU. Non-EU counterparties (called third country entities) are not directly subject to the requirements. ESMA has confirmed that where an EU financial counterparty is trading with a third country entity, the EU financial counterparty must ensure that the requirements are met for the relevant transaction, even though the third country entity is not itself subject to EMIR. This means that EU financial counterparties are likely to ask all their counterparties, including third country entities, to sign the protocol, to assist with compliance by the EU financial counterparty. If the third country entity is established in a jurisdiction which the Commission has determined is equivalent, the counterparties could comply with the equivalent rules in that country. In the case of a third country entity which is a US entity, it is likely (judging from the Commission and CFTC's "common path forward on derivatives" announcement of July 2013) that the Commission will determine Dodd-Frank's risk mitigation rules as equivalent, although the final position on this remains to be seen. Where two third country entities are trading with each other, it is open for the Commission to impose EMIR's obligations on each of the two third country entities, if the contract has a "direct or foreseeable effect" in EU or if it is necessary to prevent evasion of EMIR. ESMA is developing the scope of this power and has indicated in a recent consultation paper that it will adopt this power in fairly limited circumstances (for example, where the third country entity is guaranteed by an EU financial counterparty). Which contracts do the rules apply to? The portfolio reconciliation, dispute resolution and portfolio compression requirements apply to OTC derivative contracts which are outstanding on 15 September 2013 (irrespective of the date on which they were entered into) and to any contract concluded thereafter. What immediate steps should asset managers take? Portfolio reconciliation Counterparties must have agreed in writing a process for reconciling portfolios before 15 September 2013. Counterparties may adopt the ISDA EMIR protocol to implement this process, but should bear in mind that they cannot make any changes to the process detailed in the protocol � it is one size fits all. In addition, the protocol only applies where the other counterparty has adhered. Portfolio compression Counterparties which are subject to this obligation must have procedures to conduct a portfolio compression exercise. ISDA is not proposing a protocol to cover formal agreement of these procedures � any form of written agreement should suffice. Dispute resolution The dispute resolution obligation encompasses (i) agreeing procedures with counterparties to identify, record and monitor disputes, and to resolve disputes in a timely manner, with a specific procedure for disputes which are not resolved within 5 business days and (ii) reporting to the regulator some outstanding disputes. The standard form ISDA Master Agreement does not include a specific dispute resolution procedure. Existing dispute resolution procedures should be checked to see if they cover the specific requirements of the regulation. The ISDA EMIR protocol aims to ensure that counterparties are within the specific requirements of the regulation, whilst preserving the position of any dispute resolution procedures already agreed between the parties. FCA guidance The FCA has published guidance on the manner in which financial counterparties must report disputes between counterparties (see EMIR notifications and exemptions). In order to report, financial counterparties must register with the FCA EMIR web portal. By the 15th day of each month, financial counterparties must ensure that any disputes outstanding in the previous month have been submitted to the EMIR web portal, including details of the amount (in euros) of the dispute. The FCA provides guidance on registration with its EMIR web portal. Financial counterparties should have procedures in place to identify disputes which need to be reported, and should register on the web portal in advance of actually reporting any disputes. ISDA protocol The ISDA EMIR portfolio reconciliation, dispute resolution and disclosure protocol was released on 19 July 2013. The protocol enables parties to amend their ISDA Master Agreements (and other agreements) to comply with EMIR's obligations relating to portfolio reconciliation and dispute resolution. The protocol contains the parties' agreement to reconcile portfolios in accordance with EMIR, with a process for parties to do a data reconciliation. Parties adhering to the protocol either do so as a "Portfolio Data Sending Entity" or "Portfolio Data Receiving Entity". Dealers which have adhered to the protocol to date have adhered as Data Sending Entities. If a buy-side participant adheres as a Data Sending Entity, that means that each counterparty will send portfolio data to each other and will each perform the reconciliation process independently. If a buy-side participant adheres as a Data Receiving Entity, that means that it alone will be responsible for the reconciliation. Counterparties must have arrangements in place to reconcile portfolios. A party which adheres to the protocol can specify that it will delegate the reconciliation function to a third party. The protocol also contains the parties' agreement to a procedure to identify and resolve disputes. If a counterparty identifies an issue that it wishes to dispute with its counterparty, it may send a dispute notice to that counterparty. The parties must then try and resolve the dispute in good faith and in a timely manner. This may include using pre-agreed dispute mechanics, such as (for margin disputes) the existing dispute resolution procedure in the standard Credit Support Annex, or any negotiated dispute resolution provisions in the ISDA Master. If the dispute has not been resolved within five business days, the protocol provides that the dispute must be escalated within the counterparties. The protocol does not over-ride any dispute mechanism already agreed between parties. There is no obligation for market participants to adhere to the protocol. An alternative would be to negotiate and agree procedures for portfolio reconciliation and dispute resolution with each counterparty. Footnotes 1Articles 13 (Portfolio reconciliation), 14 (Portfolio compression) and 15 (Dispute resolution) of the Commission Delegated Regulation No 149/2013. Contact :

Antoine Sarailler, Partner, Dechert (Paris) LLP Marie H�l�ne Cr�tu is the co-founder of Codiese and has developed an innovative solution to respond to EMIR's requirements for corporates and asset managers. With GMEX group, the UK based market operator, CoDiese has built a robust software allowing its clients to fulfil their regulatory obligations. Marie H�l�ne, what do you see as the critical issues for fund managers today ? The key challenge for most fund managers is to implement a control system in order to fulfil their obligation of direct reporting responsibility. Most asset managers thought initially that their service providers would do the job. They realise that EMIR includes a compliance obligation to control the data sent to the central trade depositary. The detailed implementation rules around EMIR and their implications were exposed to market players relatively late. Most service providers such as clearers, administrators as well as the providers of LEIs (Legal Entity Identifyer) have hard time keeping up with the 12th February's deadline. Once this deadline has been passed, we see a large demand for solutions like ours to respond to the critical need of reporting and controlling of data. More on www.codiese.com |

|

This article was published in Opalesque UCITS intelligence.

|

{kind=link}