RSS

RSS|

In 2013 UCITS absolute return funds display their best annual performance since 2009 with an average progression of 4.12% as measured by the UCITS Alternative Index Global. The good returns are largely driven by the strong returns of equity markets. With an average progression of +11.07% long/short equity funds perform particularly well. Multi-Strategy and Event - Driven managers also benefit from the robust equity market performance and finish the year up 5% and 4.18%. Macro and Fixed Income funds are up a modest 2.27% and 1.90% respectively. Within the fixed income space, credit focused managers return the best performance. The worst performing strategies in 2013 are Commodities, Volatility and FX with results ranging between -3.5% and 4.2%. With a progression of +4.27% funds of funds record their best annual return since 2008. The strong allocation towards long/short equity funds explains the good result.

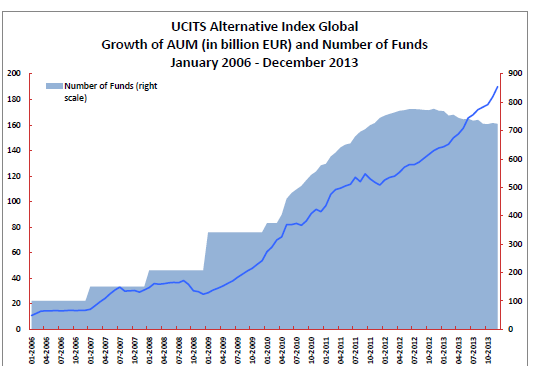

Growth of assets and number of funds2013 is another year of strong inflows for UCITS absolute return funds with a progression of 34%. The total assets managed grow from 142 billion EUR to 190 billion EUR. When adjusted for outflows, the net new assets equal 62 billion EUR, a progression of 43%.Without surprise the best performing strategies attract the larger part of new assets while all strategies that returned negative performance in 2013 saw a decrease of their assets under management. The size of the fund itself seems to remain an important factor when it comes to attracting new assets. The largest funds again account for the bulk of the increase. For instance the 10 largest funds by assets at the end of 2013 account for about 55% of total net new assets. The largest asset gatherer in 2013 is again Standard Life through its GARS funds, with almost 7 billion EUR of inflows bringing its total assets under management to north of 30 billion EUR. This demonstrates that high level of assets under management; strong distribution capabilities and top quartile performance are more and more important when it comes to attracting new assets. Given that more than half of UCITS absolute return funds manage less than 50 million EUR a large portion of them has to fight hard to increase their asset base. For the first time since 2008 the number of funds decreased from one year to the other (-6%). The decrease is explained both by poor performance and by the difficulties to attract enough assets to make the fund profitable from a cost perspective. However as in any Darwinian selection process if the absolute number of funds decreases the average quality of the remaining funds should increase. The recent performances and growth of assets under management seem to confirm this.

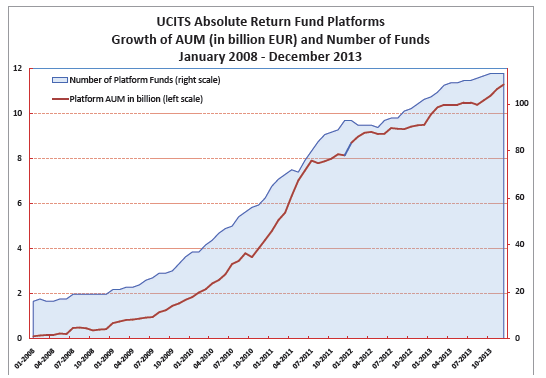

Fund platformsFund platforms showed a high level of activity in 2013 and the total level of assets managed by UCITS absolute return funds available on platforms grew by 17%. While positive, the level of assets growth is lower than the one of the broad market which stands at 34%. The first reason lies in the difference in the strategy distribution of the funds available on platforms compare to the broad market. Platforms tend to have a lower tilt toward strategies such as Fixed Income, strategies that have attracted large sums of assets in 2013. In the other hand they have larger allocation to strategies that have experienced a difficult year in term of performance and thereof witnessed a drop of assets like CTA. Secondly the majority of the funds available on platforms are still relatively small in terms of assets. They therefore face the same challenges to attract assets as described earlier. With close to EUR 200 billion assets under management the UCITS absolute return market is now a major component of the European alternative investment market. The good results of 2013 coupled with the increase interest for highly regulated products will with no doubt further fuel the growth of this market in 2014.

Louis Zanolin, Alix Capital |

|

This article was published in Opalesque UCITS intelligence.

|

{kind=link}