RSS

RSS|

After completing an MSc in Financial Management from Reims Management School and the first Islamic Finance degree of the Durham University, Mehdi belongs to the new generation of graduates that pursues an equilibrium vision of the financial services industry. His combined background of conventional and Islamic finance is illustrated by its preceding experience at Societe Generale CIB in the Structured Products Department and his involvment in CFA level 3 Programme in parallel with the Islamic Finance Degree and a close collaboration with BMB Islamic UK. The first time I read about Shariah stock screening in the Islamic Finance Qualification textbook, I remembered thinking that it was logical, understandable and actually quite simple. As the economic model of Shariah seeks the welfare of society and Justice among human beings, any financial involvement in unjust practices such as riba or in harmful industries (alcohol, gambling, adult entertainment...) should be prohibited. Therefore companies whose principal activities are the prohibited ones, or which utilize excessive interest-based debt, should be screened out. How simple! I closed the textbook, felt confident and went to the family dining room with a relaxed mind. Then, after dinner my younger brother, trying to test my knowledge asked me: Shall we invest in a separate capitalized subsidiary, which main activity is the conception and designing of gaming and gambling softwares, and which parent company is heavily financed through interest-based debt?... -Where is my textbook?? Actually it not as simple as it appears. One question leads to another and I realized afterwards that Shariah stock screening is probably one of the most challenging areas in the Islamic financial services industry. Screening a company according to the principles of Islamic Law (Shariah) is conducted through two axes: financial criteria and business activity criteria. I suggest we run through the financial criteria part first, as it is requires less (but not few) qualitative considerations than the business activity screening. The rationale behind the Islamic financial analysis is to verify that interest-bearing securities are not predominantly used in the cash investment, that the interest-based debt does not contribute significantly to the financing of the operations and that the company is not in majority composed of liquid assets. In Islam liquid assets can only be traded at par, therefore the value of the company can only be negotiable if it has illiquid assets. Let us have a look on the financial screening process by taking the example of the company Fujifilm:

Source: Amiri Capital Nevertheless, as the global Islamic financial services industry is hampered, so far, from the lack of a centralized regulatory body, there are many different ways to financially and mathematically express these ratios. The first main debate is around the denominator of these ratios, which is supposed to represent the total value of the company. Some Islamic finance players claim that as we want to measure the proportion of debt in the value of the company, and debt is based on the market, so should be the value of the company, thus taking the market capitalisation; other players consider the total value of the assets of the company as a more reliable and representative variable, and less subject to market fluctuations. As a point for the latter, it has to be noted that, and especially following the last three years of financial turmoil, the market capitalisation is nowadays a very sensitive variable which does not necessarily correspond to the economic and financial fundamentals of the company. I will always have in mind when, in the late 2008, the stock of Volkswagen increased by more than 400% in one day, and that I regretted at that time, not to be a stock visionary!!! The market capitalisation literally burst out, turning in one day a non Shariah compliant stock into a compliant one only due to the incredible "increase in value"! To temperate this argument, some scholars agreed on a relative flexibility about the calculation of market capitalisation, increasing the considered time lane, but it only affect the consequences and not the causes. Besides the denominator consideration, the complexity regarding the treatment and the inclusion or not of certain items (derivatives, preferred shares...) raised significant issues and debates. The other main challenge in the Islamic financial analysis is actually not related to the Islamic perspective. Having pointed out the lack of harmonization in Islamic financial industry in the ratio calculation, in order to be fair, I must highlight the fact that the conventional financial reporting is also concerned with different accounting rules and treatments making the comparison and thus the calculations challenging. The same financial item would be accounted differently, if we take the IFRS rules or US GAAP rules, raising issues of consistency, transparency and comparability. The second set of criteria on which a company is screened is the business activity. Any company making more than 5% of its revenue from any of these activities: conventional finance and insurance, alcohol, pork, gambling, adult entertainment (pornography, night club....), tobacco, weapons, non Halal meat, should simply be screened out. These industries, which do not contribute to the welfare of the society, could not be accepted in the Shariah framework explaining why no more than 5% of the total income should be derived from them. The question is: how do we classify with precision each company, according to its operations, and establish the compliance or not to the Shariah principles? While not knowing all about business screening, I will base the following discussion on Amiri Capital's business screening process (Amiri S3). The first step is to determine in what industry sector, the company should be included in. Financial institutions and bodies have developed a range of "business activity codes that breakdown the exact nature of the activity. For this purpose, we used the SIC codes. Standard Industrial Classification (SIC) codes are four digit numerical codes assigned by the U.S. government to business establishments to identify the primary business of the establishment. The classification, circa 1,100 pre-defined industry categories, was developed to facilitate the collection, presentation and analysis of data; and to promote uniformity and comparability in the presentation of statistical data collected by various agencies of the federal government, state agencies and private organizations. Having done that, the second step consists in determining, with the help of a Shariah scholar, the Shariah-compliant and non Shariah-compliant SIC codes, screening in the case of Amiri S3 10,000 sub-activities. The close collaboration with a Shariah scholar is vital to correctly assess the Shariah-compliancy of any activity. Let us take an example. The weapons industry is generally classified as a non Shariah-compliant activity. However, if we go back to history of Islam and principles guiding the well-functioning of the State, proper means of defense are necessary to guarantee the sake and safety of the citizens. Thus, how can we strictly and entirely prohibit the military industry involvement? Only the views and the clarification of a Shariah scholar can help sorting this important issue out:

Now, let us have a look on the business activity screening process:

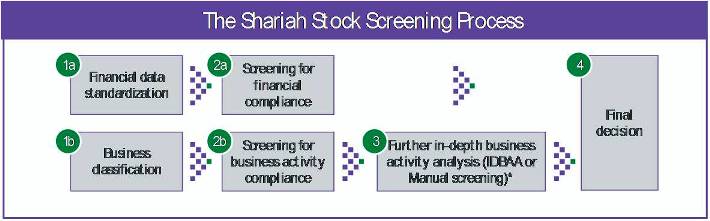

Source: Amiri Capital The problem is that most of the publicly-traded companies are engaged, due to diversification purposes, in many activities not necessarily clearly disclosed by the SIC classifications, as shown above by the Fujifilm example, This raises two questions leading to the last (but not least) step of the business screening criteria: Is the "non-core activity" Shariah-compliant? And if not, "What proportion does it represent in the overall income generated? Manual screening, or In Depth Business Activity Analysis (IDBAA) as we name it in-house, is the last and probably the most challenging part of the business activity review. It mainly occurs when screening analysts are not able to determine with exact precision each segment of the company’s business activity and the corresponding generated income. The objective is to use any available means to come up with a clear decision about any "ambiguous" company. The process involves further investigation into: the most recent annual report ("Financial information", "Publication", "SEC fillings" for US companies...), company website, and in last resort contacting investor relations, for missing information. As we can easily imagine, although not being a difficult task IDBAA is extremely time consuming but in many cases decisive in the final investing decision. The Shariah stock screening process:

Source: Amiri Capital Now, we can easily state that the Shariah stock screening process is not that easy as it initially appeared. It requires analytical judgment, thorough research, a well elaborated process, and obviously, time to dedicate. To save this time-variable, precious for fund and investment managers there are different alternatives to the manual in-house screening. Let us have a look to each of them. The easiest to way to pick up Shariah compliant stocks is to choose those utilized by the Indices providers such as Dow Jones, FTSE, S&P or MSCI. The guarantee provided to the stock-picker that any stock integrated in their Islamic indices has been subjected to a thorough Shariah-compliant analysis, is satisfying. However the main drawback in using these Indices is the limited available universe of stocks. For diversification and low-volatility purposes, fund managers cannot be restricted to a short list of Shariah-compliant stocks, making the use of Indices providers a less than ideal option to consider. The second option is to outsource the Shariah stock screening to external consultants like Shariah advisory companies. Although the universe of stocks considered can be much wider, the cost inefficiency of this option and the time to managers before investing can be detrimental. Finally the Shariah stock screening semi-automated system is the last alternative to the manual in-house stock screening. It combines an in-depth research by analyst teams with efficient computerised processing of standardised data, to create the largest universe of pre-screened stocks. However, by using this alternative, fund and asset managers face a significant Shariah risk, if the construction process has not been thoroughly followed by a Shariah scholar and has not been issued a fatwa on its own. The Shariah risk mixed with the reputation risk could prove costly to the financial institution (Islamic or conventional). To conclude, I would like to draw your attention on the importance of the Shariah stock screening as a key element in the development the Islamic financial services industry. The Islamic capital markets need to increase the diversity of the available investment solutions, by the set-up of more Shariah-compliant equity funds. Therefore we need to pursue our efforts on this path, which would enhance the depth, the liquidity and the efficiency of the global Shariah-compliant equity market. Your feedback and comments are very important to us, please feel free to contact the author via email |

Opalesque Islamic Finance Intelligence

Industry Snapshot: Opening the Black Box of Shariah Stock Screening By Mehdi Popotte |

|

{kind=link}