RSS

RSS|

The writer completed his MBA (Investment Management) from Concordia

University and is a CFA Level 3 candidate. He was recently awarded the Islamic

Finance Qualification (IFQ) designation. Mobasher has had four articles

published in the Journal of Strategic Studies, Bahrain Center for Studies and

Research. The first three dealt exclusively with Islamic finance topics namely:

Sukuk (see

reference link), Islamic Hedge Funds (see

reference link) and the impact of the current financial crisis on Islamic

banks (see

reference link). The last paper dealt with the rise of sovereign wealth

funds.

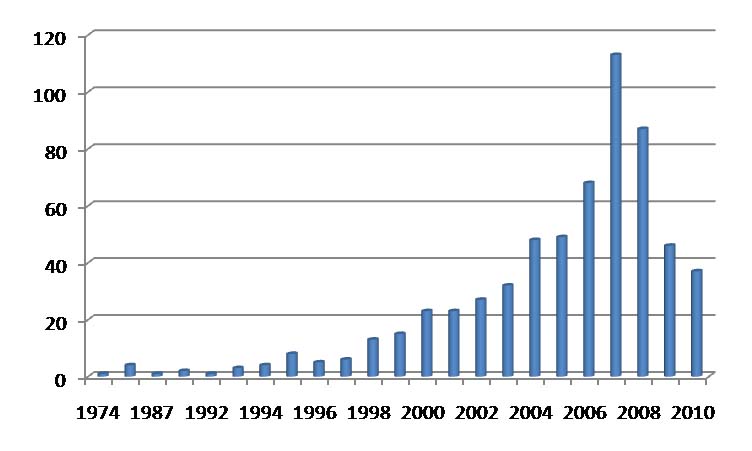

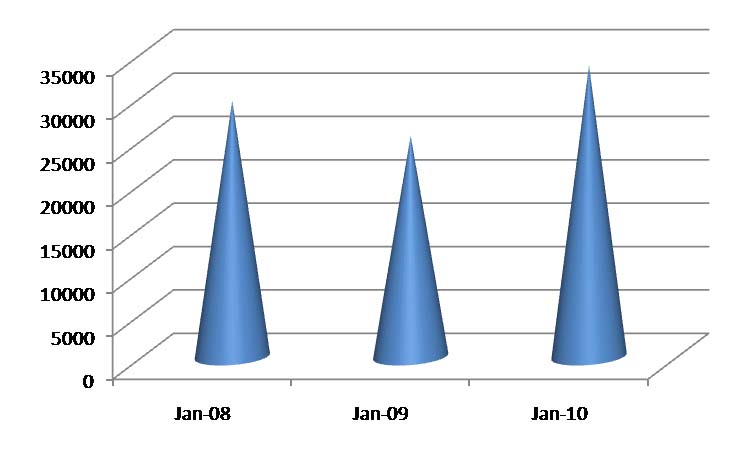

Source: Thomson Reuters-Lipper

Note: Net Asset Values based in $ Millions

Source: Thomson Reuters/Lipper

Return indicators from major international Islamic benchmarks display

resilience in the face of troubling economic conditions. With the global

financial architecture undergoing an uncertain transformation fund managers must

exhibit prudence in asset selection. This is particularly acute given the

discernable limitations of dedicated delivery channels in emerging markets where

the breadth and depth of various fund offerings has yet to become part of the

financial planning tools available to the average investor. In similar vein fund

managers operating in developed markets are equally constrained as Islamic funds

remain sidelined to the sphere of socially responsible investing. Overcoming

fund raising constraints necessitates aggressive rebranding and streamlining of

distribution channels to ensure selection of Islamic funds as the investment of

choice while helping managers build scale. |

Opalesque Islamic Finance Intelligence

Industry Snapshot: A Study of Islamic Mutual Funds Mobasher Zein Kazmi |

|

{kind=link}