RSS

RSS|

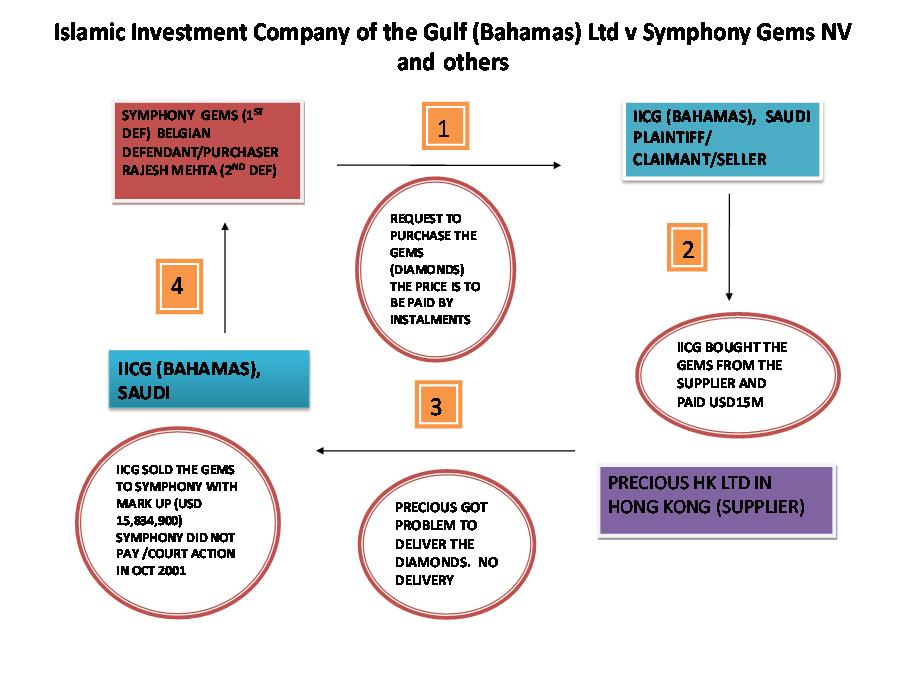

Hakimah Yaacob and Edib Smolo are both Associate Researchers at the Islamic Banking Unit, International Shari'ah Research Academy (ISRA) for Islamic Finance. Hakimah holds a Bachelor of Laws (Hons), Bachelor of Syariah (Hons), a Master in Comparative Laws, from International Islamic University Malaysia and a diploma from Tokiwa International Institute, Japan. Previous positions held include Head of Law Reform & International Treaties, SUHAKAM, legal practitioner, as well as being the Drafter of International Standard Organisation 26000 on social responsibility. She has published many articles on alternative dispute resolution (ADR) in Islamic finance including arbitration, mediation and hybrid ADR. Edib obtained his undergraduate double-degree in Economics and Islamic Revealed Knowledge (Hons) as well as Master in Economics from International Islamic University Malaysia. He has published several papers on Islamic microcrediting, economics, and finance. Their combined areas of specialization are in Islamic banking and finance, law, microcrediting, fiqh muamalat, risk management, Islamic capital market products, mediation, ethics and social responsibility (among others). Reviewing the decision in Islamic Investment Company of the Gulf (Bahamas) Ltd v Symphony Gems NV and others, which was decided by the Queen's Bench Division (Commercial Court) on 13th of Feb 2002, is a must for Islamic finance practitioners since it provides a significant precedent for the Islamic finance industry. Everything started with a murabaha agreement executed between the parties consisting of IICG as the claimant or the seller or the plaintiff and Symphony Gems and Others. The purpose of this short article is to highlight few triable issues concerning the validity of Shari'ah law in the eyes of English court. Regardless of whether we name it a murabaha or a wakala, for the English court it is just a contract. The terms bound the parties as long as it does not contravene any legal provisions and law (of course not Shari'ah law). In this case, the purchaser requested the seller to purchase the supplies and sell them to the purchaser through a murabaha arrangement and the seller agreed to make such purchases and sell the supplies to the purchaser on the terms and subject to the conditions set out in the so-called "murabaha agreement." The brief summary of the case can be seen from the table below:

Source: Author's own

The murabaha contract is viewed as an alternative to the lending practices within conventional banking. The transaction involves two types of promises: a promise by the client to purchase the goods (wa'd) and a promise by the bank to sell him the goods. The payment may be in cash or deferred. The two parties will conclude the sale after the purchaser has the goods in his possession. Although it is generally argued that the purchase orderer may or may not be obliged to conclude the sale, some modern scholars have allowed the promise in this type of sale to be binding for the purchase orderer. Today, this practice is known as wa'd. Imam al-Shafi, in his book al-Umm, held that this transaction is valid provided that the bank receives the purchased items. The validity of wa'd is based on the Maliki school held by Ibn Shabramah that any promise that does not results in permitting that which is forbidden or forbidding that which is permitted is binding. This applies whenever the promise leads another person or entity to undertake a financial obligation. The bank also must hold the risk of destruction of the goods prior to delivery to the final buyer. The court discussed several issues including the validity of the agreement and the illegality of the contract executed. It is very interesting to note that most of the cases in Islamic finance will delve into the defense of non-compliance when the party or the defendant fails to comply with the contract or in other words fails to pay. The two experts were called to testify the ingredients and the validity of a murabaha contract. After a deliberate discussion, the experts said that underlying contract is not based on a murabaha transaction. In the end, the court ignored their expert views and considered a contract as valid from English law point of view. This is due to the express terms in the contract saying that even without delivery of the goods, the seller is still entitled to claim the price (refer to the Clause 4.3, 4.4, 5.1, 5.2 and 5.6 of the agreement executed between the parties stating that delivery of goods is not a prerequisite for the seller to recover the sale price from the purchaser). As a result, the court judged in favour of the plaintiff.

Table 1: Relevant clauses of the case

Source: Murabaha Aggreement between Islamic Investment Company of the Gulf (Bahamas) Ltd v Symphony Gems NV & Ors [2008] EWCA Civ 389 (11 March 2008), ([2008] EWCA Civ 389, From England and Wales Court of Appeal (Civil Division) Decisions; 31 KB)

The total amount of US$ 10,060,354.28, up until 13 Feb 2002 inclusive of both principal and the compensation for late payments, was awarded to the Plaintiff. This was calculated on a basis more favourable to the defendants than the contract required. This case observed the consistency of the practice of English law in the tendency towards a literal interpretation of commercial agreement. If the reference to Islamic law is made, it is a less likely that the murabaha agreement constructed in this case would be enforced because of the issue of non-compliance to Shari'ah. This is according to AAOIFI Standard No. 8 (3) on murabaha, which states that "The institution is prohibited from selling any item in a Murabaha transaction before having acquired the item. Hence, it is not valid for the institution to conclude a Murabaha sale with the customer...before actual or constructive possession of the item..." Therefore, the reasons for stating that in this case it was not a murabaha transaction are as follows: i) According to the agreement, the delivery is not a prerequisite for payment. In murabaha contract, the payment for the goods ordered takes place after the delivery of goods. Here the possession of goods never took place and the goods were never delivered. ii) The risk is supposed to be borne by the bank and properly insured. However, in this case, the risk was solely borne by the purchaser, i.e. the client.

Therefore, we believe that the choice of parties to be adjudicated by a non-Islamic court in a non-Islamic jurisdiction shows that a due recognition was not given to the validity and the principles of Shari'ah law. Even though the contract is deemed as being non-compliant with Shari'ah law, the court still validated the transaction based on normal contract and made it enforceable. This decision may be harmful to the Islamic finance industry as its aims to comply with Shari'ah are seemingly being defeated. Furthermore, this case could easily be used as a precedent in future disputes whereby the Shari'ah rulings will be abandoned in favour of prevailing English law (or any other law depending on the jurisdiction). For example, in Shamil Bank of Bahrain v Beximco Pharmaceuticals Ltd and others, Shari'ah is not a choice of law because it is considered a non-national law. If parties to a contract want to apply Shari'ah for the Islamic financial contracts it must be specifically incorporated in the contract itself. If the parties give the right to an English court to try their case then the English court will interpret the sukuk contracts (and any other contracts for that matter) according to the law of England except where specific peculiarities of Shari'ah have been expressly added in the contracts. The reference to the "Glorious Shari'ah" in the governing law clause was merely intended to reflect the Islamic religious principles according to which the Bank held itself out as doing business. It was not a system of law designed to trump the application of English law as the governing law. Having said that, this case was decided on the construction of the governing law clause, which incorporated English law. Hence, the Court did not need to consider and apply Shari'ah. Consequently, the judge held that even if the plaintiff (Shamil Bank) acted in contradiction of the Shari'ah and this may have contributed to the defendants subsequent default, it was no matter for English courts to decide and therefore they must decide only in accordance with English Law. Nevertheless, in the recent case of The Investment Dar Co KSCC (TID) v Blom Developments Banks SAL, TID claimed that the agreement is not Shari'ah compliant being an agreement for deposit taking with interest and therefore null. Even if it is valid, according to the agreement, profits payable to Blom should be limited to 5% and any extras should be retained by TID as its own profits. If there are any losses, on the other hand, it will be borne entirely by Blom. The court allowed the appeal (dismissed the summary judgment and ordered full trial) on the condition that TID first pays Blom the principal amount invested by Blom. The court refused to discuss on the Shari'ah compliance of the deposit products, as the Shari'ah committee of TID has already ruled on its compliance, and the court relied on the expert evidence by the Shari'ah committee. This case also invites ethical issues that play a major role in Islamic finance, and it is a very interesting case since the parties argue the validity of a Shariah contract in an English court of law. In short, it is not an issue of contract being Shari'ah compliant or not, it is a contract that reads in the eyes of English law. The Shari'ah validity may not be relevant in this case as the English court will not bother to determine whether the contract is valid or not. Finally, if we make it a practice to have Shari'ah issues being heard at the English court and if we leave to the English court to decide on its (Shari'ah) validity, then the above cases provide strong indications of the potential results. Should this continue, the industry will be presented with a serious legal dilemma in the future. Your feedback and comments are very important to us, please feel free to contact the author via email. |

Opalesque Islamic Finance Intelligence

Lex Islamicus: It is not a murabaha contract; it is just an English law of contracts By Hakimah Yaacob and Edib Smolo |

|

{kind=link}