RSS

RSS|

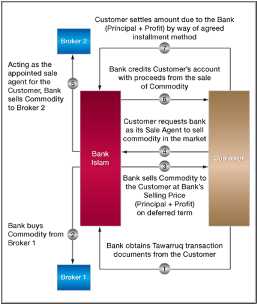

Mohammed Khnifer is regarded as part of a 'second generation' of Islamic banking practitioners who have a solid academic background in Islamic finance. He is a holder of an MSc in Investment Banking & Islamic Finance from Reading University and is a Chartered Islamic Finance Professional (CIFP) from INCEIF. He is one of the most prolific and well-known journalist specializing in Islamic Finance today. For the past six years he has been in charge of the editorial content for the Islamic Banking section of Al Eqtisadiah (Kingdom of Saudi Arabia). The principle of Maslahah (public interest) may be used to determine the desirability of a particular Shariah interpretation in such matters as the use of Murabahah-based structures in Islamic finance. Respecting, understanding and implementing Shariah are the backbone of the trillion dollar Islamic finance industry. Shariah scholars are deemed to be the gatekeepers for the Islamic finance sector. With their guidance, legitimacy can be fulfilled and confidence in the industry achieved. While Shariah advisors themselves come from four prominent Sunni schools of thought, or fiqh, they together attempt to achieve Ijtihad and Maslahah, that is, finding common ground over their respective rulings on some of the controversial financial instruments of our time. Within this framework we argue the need of favouring Maslahah with Murabahah-based structures in spite of the landmark 2008 ruling by the OIC (Organization of Islamic Countries) Fiqh Academy, a ruling that declared organized Murabahah (Tawarruq) as non-compliant with the principles of Shariah. Maslahah can be defined as the "unrestricted" public interest, which is one major component of the framework of Islamic law, or Shariah. The objectives of Shariah are commonly defined in Imam Ghazali's classification of "unrestricted" public interest in terms of the protection and preservation of religion, life, intellect, property and progeny (Dar, 2009). Thus, Islamic financial products based on (the objectives of) Shariah must attempt to enhance "unrestricted" public interest. In reality there is a disagreement between liberal and conservative scholars over the necessity of applying Maslahah on some Islamic banking products. This disagreement (i.e., on when to apply Maslahah with specific products such as Murabaha) has moved from closed doors meetings to the public, resulting in creating the biggest Shariah risk this industry has ever seen. In 2009, the OIC, and through its powerful line-up of senior Shariah scholars, sent shock waves across the industry. The OIC Shariah committee, comprising more than 50 scholars, of which few are directly involved in Islamic banking, disregarded the public interest of Islamic financial institutions by declaring organised Tawarruq impermissible as it has elements of interest-based lending. So rather than clarify issues and state what steps needed to be taken in order to ensure compliance, the entire practice was at once ruled non-compliant (Firoozye, 2009). Nonetheless, it is imperative to hear their justification over the ruling. The OIC considered it a "trick" to get cash now for more cash paid later, which is prohibited in Islam. While it may be considered a hiyal (legal strategem or ruse to circumvent Islam's most basic prohibition on riba) the combination of purely legal strategies as a means of arranging financing was sufficient to legitimize it (under very specific circumstances according to the majority of jurists) (Firoozye, 2009). What makes this ruling especially injurious is that Tawarruq and commodity Murabahah have become essential financial instruments in wholesale banking. The OIC ruling implies that the banks are not really interested in delivery of underlying assets, which in any event has questionable overlapping ownership by brokers. To illustrate, Muddassir Siddiqui (2009) defines organised Tawarruq as the purchase of commodities from local or international markets and their onward sale (on a deferred payment basis) to the customer. The seller then (as agent for the customer) on-sells the commodities (to a person who must be different from the first supplier) for a price that is lower than the deferred payment obligation owed by the customer. The result is the customer gets a cash amount for his required business or personal purposes. The OIC scholars made it clear that even though organized Tawarruq may comply with the letter of Sharia, it is does not comply with the spirit of Sharia. That is, commodity Murabahah is legitimate because it involves the sale of assets, rather than a lending operation. But what if the assets are just an entry to the broker's book? It begs the question: is anyone interested in the actual assets? Firoozye (2009) capitalizes on this point by saying that banks themselves are not generally equipped to take delivery of tons of palladium or gold; rather, they use the services of brokers & custodians. These same custodians can potentially make all necessary changes of title in milliseconds before the price of the underlying can actually change, and before either the bank or customer might take much in the way of market risk. Before embarking on the argument favouring Maslahah and ignoring the OIC ruling, one should take a profound look at the wide utilization of Murabahah within the Islamic banking industry. It is the basis of many credit card transactions (primarily in the GCC region). It is used in covered drawings, in top-up facilities, in mezzanine financing, in liquidity management and in working capital finance (among other things) (Firoozye, 2009). Furthermore, modern Shariah supervisory boards (SSBs) have engineered and approved a host of hybrid nominates, using a single nominate such as Murabahah in different configurations (such as parallel Murabahah, reverse Murabahah, back-to-back Murabahah, and reverse parallel Murabahah contracts) (DeLorenzo, 2007). Having witnessed their young industry being shaken up with the OIC fatwa, a group of prominent scholars, led by Nizam Yaquby, stood up and challenged the establishment's ruling. These scholars went public and appealed to the principle of Maslahah. They made an argument that commodity Murabahah is the backbone of the industry and it should be legitimized on the basis of social usefulness or social needs of the Islamic Ummah. To compliment the above view, other observers profess that OIC scholars had a narrow view on the usage of commodity Murabahah. That is, the product can be used to serve customers in the retail banking. Further, the product itself can be used in the wholesale banking. OIC fatwa on the impermissibility of organized Murabahah takes into consideration that this product is used mainly in the retail division. Thus, it ignores the use of this product as a liquidity management in the wholesale banking division. Islamic banks can not function properly without inter-bank transactions. Banks use Murabahah to borrow and lend from each other from as short as overnight to as long as one year and even more. Murabahah is a fundamental element in the liquidity management process. If you condemn Murabahah as non-Shariah compliant, then the Shariah inter-bank market might collapse, forcing these banks to channel their excessive funds to the conventional system, which would essentially be the end of Islamic banking as we know it. In addition to that, Murabahah is one of the Lender of Last Resort facilities. All in all, the benefit of continuing using Murabahah contracts, despite some Shariah reservations, outweighs the call for its impermissibility as they fulfil a useful purpose. Organized Tawarruq Structure Diagram:

Source: Bank Islam Organized Tawarruq Step by Step

How can Islamic financial institutions manage the risk of non-compliance with Shariah ? Over the past decade the Islamic finance industry was increasingly exposed to the risk of creating banking products that might be deemed not in compliance with established Shariah principles, thus losing customers and profits in the process. This is what we now term Shariah compliance risk. A heated debate among practitioners over some of the more innovative products (which sometimes mimic conventional ones) led to the creation of the term "Shariah risk." In recent years banks and other Islamic finance institutions (IFIs) have become increasingly sensitive to Shariah risk as more and more respected Islamic scholars began to openly criticize certain types of Islamic banking practices (Firoozye, 2009). Indeed, the short history of Islamic finance is embedded with anecdotes of high-Shariah-risk products such as commodity Murabahah and to some extent asset-based Sukuk. Recognizing and mitigating Shariah risk, which is sometimes not understood very well even by some industry experts, is not especially different from managing market risk, credit risk, liquidity risk and operational risk. Shariah supervisory boards (SSBs), which certify finished products with a fatwa, play a vital role in managing such risk. Also critical to managing Shariah risk is the active role played by an IFIs Chief Risk Officer (CRO). The concept of mitigating Shariah risk rests jointly on the shoulders of the CROs and SSBs. With the increasing recognition of Shariah risk among IFIs over the last decade, there have been concerted efforts to understand, analyse and control Shariah risk within every jurisdiction that Islamic finance is active.

Shariah risk management is identical in process and procedures to general risk

management, of which there is an abundance of professional reference works to

refer to for guidance. Basel II, the ultimate risk-management system, is now

nearly universal in identifying, measuring, and protecting against any and all

risks that affect a bank's operations. Furthermore, at the ex-ante Shariah compliance stage, a developer may incur considerable costs for a new product, including costs directly related to Shariah compliance and, in order to retain first-to-market status for the business, will insist on keeping the fatwa out of the public eye for a time (DeLorenzo, 2007). Shariah risk is also managed ex-post compliance, i.e., after a product is approved and launched. Shariah risk management involves, at this stage, continuous monitoring and testing of the rationale originally used to issue the product's fatwa. As we know, opinions can change within the community of respected Shariah scholars, and when enough opinions change there can be a sizeable shift in attitude toward one type of product or service. Staying close to the community of Shariah scholars and their professional dialogue is critical to proper Shariah risk management. Some industry observers believe non-compliance risk is more likely with ex-post shariah compliance. In response to such potential risk, many Islamic banks try to strengthen their Shariah risk management, i.e., controlling the functions where identification and assessment of Shariah risk would be systematically monitored and controlled to avoid non-compliance of Shariah (Ibrahim,2009). Shariah compliance is a shared responsibility, where both CROs and SSBs must be involved ex- and post-compliance. All IFIs are encouraged to set up dedicated Shariah compliance risk divisions (Ibrahim, 2009). Within this division, there should be a Internal Shariah Compliance Unit (ISCU) which compromises a Shariah Compliance Officer and staff well trained in and with knowledge of Islamic finance. To compliment the ISCU role, the Internal Shariah Review Unit (ISRU) should operate like other typical internal audits, but report to the SSB (Hussain, 2009). The objective here is to provide checks and balances in ensuring all operations of a full-fledged Islamic financial institution are Shariah compliant, achieved through an effective Shariah review and audit (Ibrahim, 2009). It is often the case that Shariah advisors possess little knowledge of advanced accounting and auditing. In some cases, Shariah auditors are recognized as a second line of defence in the process of managing Shariah risk. As an example, Aznan Hasan, the well-known Malaysian scholar, demonstrates how these auditors once managed to uncover non-Shariah practices by brokers on the London Metals Exchange (LME). In his interview with the Saudi newspaper Al Eqtisadiah (Khnifer, 2009), Hasan exposed what he termed "Fictitious Murabahah" activities undertaken by some LME brokers. He discovered the frequent overlapping ownership of underlying assets. After a Shariah audit he illustrated how commodity broker (A) when selling a commodity, involved multiple and simultaneous ownership, meaning one particular commodity was sold to more than one buyer (Khnifer, 2009). Indeed such non-Shariah activities may not have been discovered and eliminated if it were not for the Shariah auditors. Do these risk management methods lead to desirable outcomes in line with the public interest? Given a heightened sensitivity among banks to be socially responsible generally, whether Islamic or not, it appears that a bank can manage Shariah risk and try to simultaneously attain Maslahah. Every bank has what we term its own internal micro-Shariah risk. That is the risk that can be confined and eliminated through the process of ex ante and post-shariah compliance described above. Hence, if a bank properly applies Shariah risk mitigation, then most risks will likely be eradicated during the process to create Sharia-compliant products, and then during the management and administration of those products. Like a canary in a coal mine, Shariah risk management is meant to spot risks before they occur, or at least before they become a problem. The result of a committed effort to plan and implement a Shariah risk management program is directly and indirectly a public good. Not only are bank customers enjoying increased protection from non-compliant products and services, they are equally protected by a bank whose own capital is better protected from failures in the risk management process. There is in fact no difference in the outcome of good Shariah risk management than credit risk, information risk, property risk and regulatory risk management. Thus, Maslahah is definitely being served by banks that adopt methods to manage Shariah risk as a fundamental part of overall risk management. The correlation between managing the risk and Maslahah can be appreciated more if we assume a scenario where a bank fails to mitigate such risk. Just because other banks are better or worse in credit management, other banks can be better or worse in Shariah risk management. Nobody wants to see an Islamic bank violating Shariah principles as this will create chaos and confusion, which ultimately erodes shareholder capital and the bank's ability to function efficiently.For example, if a Muslim community has concerns regarding religious compliance of a banking product, it will definitely reflect on the other related products in the same category, thus affecting the profitability of the bank. The consequence of such spillover is that depositors will withdraw their funds, as they take this issue just as seriously as rumors of bad credit. With that in mind, it is noteworthy that any bank that prudently and proactively manages Shariah risk, and better than other banks, is performing a public service as it is increasing customer confidence. Therefore, ensuring the complete implementation of Shariah risk management can lead, from the micro-level on up, to a desirable outcome. At the same time, banks need to simultaneously consider macro-Shariah risk. This risk arises when an established entity such as the OIC issues a fatwa which might lead customers think that a bank's already issued fatwa on certain product has been overturned by a higher authority. No bank can overturn an OIC ruling on Tawarruq, for example. This controversial OIC ruling exposed Islamic banks to the most significant Shariah risk in recent history, significant as it had the potential to nullify hundreds of billions of dollars of yearly transactions (Firoozye, 2009). In this scenario, a bank formerly comfortable with its own Shariah risk management system, and the interaction of its CRO and SSB in managing the bank's internal Shariah risk, would find itself potentially losing large volumes of formerly stable revenue because an outside authority, such as the OIC or AAOIFI (the Accounting and Audit Organization for Islamic Financial Institutions), delivered a ruling that at once undermined one major form of its conventional Islamic banking. To illustrate such macro Shariah risk, Muhammad Taqi Usmani, chairman of the AAOIFI board of scholars, brought the Sukuk industry to its knees when he declared in early 2008 that about 85% of Sukuk in the GCC region did not comply with Islamic law because of a then-standard repurchase undertaking agreement. Following his pronouncement, sales of sukuk plunged to US$13.9 billion in 2008 from a record US$31.0 billion a year earlier, according to Bloomberg's data (Khnifer, 2009). Any bank that had counted on revenue from new Sukuk issuances would have been sorely disappointed. Being now aware of the potential magnitude of losses from macro-Shariah risk, bank managements must establish contingency plans in order to counter or minimise the effect of such risks. In order to manage such risks prudently, banks need to measure exposure to macro Shariah risk on an ongoing basis. This requires both a bank's CRO and its SSB to proactively maintain close tabs and constant surveillance of the body of Shariah scholars and organizations that make rulings that might affect a bank's operations. The business of risk management at banks is well established, and there is abundant literature available to support a conventional, acceptable risk management system inside any bank. Just as CROs constantly evaluate "what if" scenarios, mapping out for example the potential loss of customer deposits if the failure of a certain product or service causes reputation risk, so can CROs duplicate this process for Shariah risk, both from internal and external sources. In conclusion, a desirable outcome can be achieved through managing Shariah risk at the micro level, but Islamic financial institutions also need to include macro Shariah risk in their planning. The results will be a stronger, more stable banking enterprise, which over time fulfils the public good. References: Dar, Humayon (2009). At the crossroads, from NewHorizon Khnifer, Mohammed (2009). LME brokers practice non-Shariah Murabaha activites, from Aleqtisadiah newspaper Khnifer, Mohammed (2009). US$ 31 billion vaporised after Usmani Sukuk comment, from Aleqtisadiah newspaper DeLorenzo, Yusuf Talal (2007). Shari'ah Compliance Risk, from Chicago Journal of International Law Firoozye, Nikan (2009). Tawarruq: Shariah Risk or Banking Conundrum?, from Opalesque Hussain, Madzlan Mohamad (2009). Regulatory Approach to Shari'ah Governance System, from ISRA Ibrahim, Muhammad bin (2009). Managing Shariah Risk through Shariah Governance, from ISRA Laldin, Mohamad Akram (2009). Shari'ah Governance from Scholars' Perspective, from ISRA Siddiqui, Muddassir (2009). Islamic finance update, from Denton Wilde Sapte Your feedback and comments are very important to us, please feel free to contact the author via email. |

Opalesque Islamic Finance Intelligence

Featured Structure: Maslaha and the Permissibility of Organized Tawarruq Mohammed Khnifer |

|

{kind=link}