RSS

RSS|

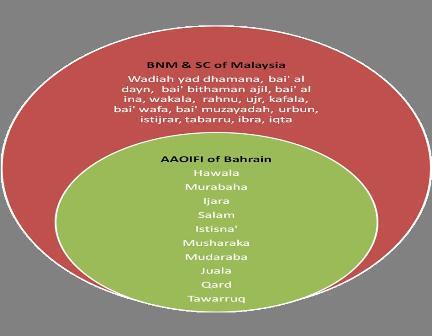

Anne-Sophie has recently submitted an MPhil on Islamic finance at the Center for Arab and Islamic Studies of the Australian National University titled 'The Sources of Variation in the Application of Shari'a Compliant Finance Contracts'. Her research interests are Islamic finance in the Gulf Cooperation Council and Southeast Asia and she has conducted extensive fieldwork research with Islamic finance practitioners in the UAE and Malaysia. She was awarded the National Australia Bank Sheikh Fehmi El Imam scholarship of 2008 and is currently writing a book on Islamic Finance with Edgar Elgar Publishing. The following article is a brief overview of the conclusions of her MPhil thesis based on research and material gathered between 2007-2009. In essence, Shari'a-compliant finance supports activities in the financial system that are in line with the principles for transactions and contracts detailed in Islamic commercial law. It has a clear set of approaches in contractual structures and product structures for financing operations. These financing operations share the same economic objectives as those of the conventional financial system yet do so with different underlying structures and customer-institution interactions. In Sheikh Delorenzo's words, 'while the economics are the same, the mechanics are different' (1). Islamic finance in its applications has adapted to regional circumstances beyond the overarching prohibitions against riba, gharar and maysir in Shari'a-compliant transactions. A sign of this adaptability is the spectrum of perspectives on the permissibility of the implementation of some key Islamic transaction contracts. This variation has been the source of debates among practitioners in the industry, particularly and most notably recent debates around the permissibility of the tawarruq arrangement and certain sukuk structures. Within the diverse cultural and socio-economic contexts in which Islam is practiced, and beyond regions where Islam is the predominant religion, the ways in which Shari'a-compliant finance is practiced varies around key yet narrow areas. True to the characteristics of adaptability reflected in the diversity of regions that Islam is practised in, Islamic finance, considered in the realm of secondary matters in which a variety of opinions is permissible, arguably reflects a corresponding capacity for adaptation to regions as diverse as the Middle East and Southeast Asia. The consequense of this adaptability is that a variety of interpretations are needed to suit and mediate between specific environments in which Shari'a-compliant finance is practiced and between interpretations of what should or ought to be done in different parts of the world by various groups of Shari'a scholars, some of whom have differing opinions. Some would argue that the ways in which Islamic finance is practiced reflects and demonstrates a dynamic adaptation to distinct local norms and local regulatory environments. Variations in Islamic Finance Between the GCC and Malaysia Malaysia and the GCC are key to analyze these overarching trends in the application of Islamic finance contracts to financial products. As the two regions cover a major portion of the total market share of global Islamic finance, a comparative analysis of Islamic finance contracts applied by IFIs and their links to members of the Shari'a boards is representative of broader global trends. Studies of the Shari'a-compliant financial system have presented the system as a whole while neglecting to understand certain pockets of divergence within the field. Such neglecting does not facilitate a clear understanding of the underlying structures of the sector in the transactional structures. Nor does it facilitate an understanding of the human and regional dynamics of the sector through the involvement of the members of the Shari'a boards of differing backgrounds. Convergence Between the GCC and Malaysia Universally accepted contracts in Islamic finance across the GCC and Malaysia, that are accepted in practice by Shari'a scholars of differing backgrounds and nationalities across the two regions, are the mudaraba contract to both project-financing and deposits; the musharaka contract to project financing; the musharaka mutanaqisa contract to asset financing; the ijara contract to asset financing; the murabaha contract to asset-financing and the istisna' contract to manufacturing and construction financing. Looking at the composition of the countries of origin of the Shari'a boards of banks for this study, the permissibility of these contracts is recognized by jurists across the two regions: Saudi Arabian, Kuwaiti, Qatari, Egyptian, Bahraini and those operating in the Malaysian regulatory context (including a Sudanese and a Syrian). They are from a broad range of institutions, having being trained both in the Middle East and Malaysia and working on the boards of the institutions in Malaysia and the GCC. As such these contracts do not seem to pose any issue from a Shari'a perspective as scholars from a variety of backgrounds, working in a variety of regions, for institutions headquartered across the two regions of interest, are in agreement on its permissibility. The contract of mudaraba is broadly accepted across the two regions and can be applied in the context of project-financing but is more commonly applied in the context of deposits or investment accounts in banking. It is especially applied to deposit accounts in Islamic banks headquartered in the GCC. The mudaraba contract in deposit accounts has a corresponding function to the wadiah yad dhamana contract which often is used for deposit accounts in the Malaysian market. It is recognized as permissible in institutions which have Shari'a boards made out of scholars of differing backgrounds. The study also indicates that the musharaka contract as the basis of project-financing is recognized and applied by IFIs across the GCC and Malaysia and so is musharaka mutanaqisa. Slight Divergence in Interpretations Differences of opinion may be identified in contracts that are exclusively offered in some regions or by particular IFIs and an analysis of this was made based on the composition of background of their Shari'a boards. These differences included those surrounding the application of the wadiah contract, the application of the mudaraba contract to the takaful model, the application of the contract of qard to deposit accounts, the use of the bai' al ina contract for cash-financing and as the basis of the deferred payment scheme of the bai' bithaman ajil scheme, the use of the tawarruq financing contract, the use of the murabaha contract in asset-financing underlying the bai' bithaman ajil scheme, the application of the wakala contract in the takaful model and the use of bai' al dayn in the Malaysian secondary market. The wadiah contract is a readily available Islamic finance contract in the Malaysian market for savings and current accounts. From a sample of Malaysian Islamic financial institutions: all are Malaysia-based Islamic banks, and the contract of wadiah, as applied to deposits and current accounts, is approved by Bank Negara Malaysia's Shariah Advisory Council. Two Islamic banks headquartered in the GCC with regional subsidiaries in Malaysia were observed not apply the contract of wadiah for deposits and current accounts, but they both use the mudaraba and qard contracts for such purposes. Wadiah is not used for banking products in GCC-based Islamic banks. In Islamic insurance or takaful, the mudaraba contract is predominantly used in Malaysia. The GCC has seemingly a preference for the use of wakala (agency-based) takaful. There is however evidence that the preferred structure is moving towards a hybrid of wakala and mudaraba. Although there seems currently to be a trend towards the mudaraba-wakala takaful model, the single use of the contract of mudaraba as a base structure for the takaful model is popular mainly in Malaysia. From the information available from the study, it is mainly GCC-based companies that offer wakala-based takaful products. The qard ul hassan contract, which is meant to be benevolent in nature, is generally not used by Malaysian Islamic banks for savings accounts. The contract of qard is applied by banks originating from the GCC in Malaysia but not by Malaysian Islamic banks. There is a general view in Malaysia that the use of the qard ul hassan contract, due to its benevolent nature, should not be for financing as the Islamic bank offers financing facilities with customers' deposits who expect returns. The use of the contract of qard or qard ul hassan for deposits is prevalent in the GCC-based Islamic banks. From the study, the make-up of Shari'a boards approving these is Saudi Arabian, Kuwaiti, Bahraini, Egyptian, Qatari, and Emarati. The contract of bai' al ina in its application for cash-financing is widely utilized in the Malaysian Islamic banking context but not in the GCC. In Malaysia, it is also applied as the basis to facilitate the transaction of the bai' bithaman ajil product offering. Bai' bithaman ajil technically refers to a form of deferred payment arrangement between the bank and its customer out of a prior underlying transaction that can be either bai' al 'ina or murabaha. Thus bai' bithaman ajil is neither a financing nor a trading contract. Yet in Malaysia it has become a normal product term used by Islamic banks for specific asset-financing products. The murabaha-based bai' bithaman ajil is applied only in Malaysia by a Saudi Arabian bank as an answer to the broadly used Malaysian bai' al 'ina-based bai' bithaman ajil. With regards to tawarruq (commodity murabaha or reverse murabaha), it is a recognized concept in the two regions and is increasingly regarded as a viable alternative to the bai' bithman ajil based on the bai' al 'ina contract in Malaysia, but there still is a considerable amount of debate among Islamic finance scholars on its permissibility. The concept of bai' al dayn as applied in the secondary market is only applied in Malaysia and is rejected by scholars from the Middle East. There is no application of bai' al dayn in the GCC Islamic financial system, and there is therefore no Islamic money market in the GCC. The Islamic financial institutions of the GCC have to function with the conventional money market to some extent. In Malaysian Islamic financial institutions bai' al dayn refers to the sale of two types of debt: the sale of debt arising from the sale of a commodity and the sale of debt arising from credit. That the debt is sold to a third party at a discount is the main point of divergence between scholars of the GCC and Malaysia. With regards to the sukuk market, discussions at a February 2008 meeting among Shari'a scholars of the board of the AAOIFI in Bahrain resulted in much confusion in the sukuk market about the permissibility of certain sukuk structures. What came out of the research was that the sukuk ijara structure was univerally recognized by Shari'a board members as Shari'a-compliant. The Influence of the Shari'a Framework Islamic finance is is applied in regions as diverse as Southeast Asia and the Middle East. With such a variety in the contexts in which it is practiced and implemented, it is to be expected that there be variations at the level of the use of Islamic finance contracts. It is to be expected too that there will be disagreements and a divergence of perspectives on the permissibility of contracts based on the context and the time at which Shari'a pronouncements or fatawa are made. The variety in regions reflects a variety in needs, a variety in socio-economic and political contexts as well as differing economies and regulatory environments, to which Islamic finance was adapted at a particular point in time in the evolution of the sector. Shari'a board members who are predominantly experts in fiqh al muamalat have played a key role in this process of adaptation as the contemporary financing needs of Muslims are as diverse as the regions they are based in. Additionally, the financing needs of Muslims have required interpretations beyond the classical contracts pre-existing the implementation of conventional finance in the Arabian Peninsula and the Indian subcontinent and this interpretative process has required Shari'a board members to exercise interpretation. With interpretations come variations and divergence of opinions and this divergence is respected in subsidiary matters in Islam. These subsidiary commercial matters are not core to the faith such as the tenets of the faith and its rituals. Secondary matters or subsidiary matters, such as those covered by Islamic commercial law, allow for this wealth and divergence in perspectives. The Shari'a boards of the institutions offering particular Islamic financial products showed a distinctive composition or pattern based on the nationalities and backgrounds of Shari'a board members of the type of products likely to be permitted. An analysis of the regions of origin and regions of training of Shari'a board members revealed that a significant portion of the Malaysian members of the Shari'a boards have studied in the Middle East, and as such that they would be familiar with the opinions of members of the Shari'a boards in the GCC. As such the regional differences could not be linked only to the states of origin of the Shari'a board members. A reflection on the regulatory structures at the level of the formal and the informal Shari'a framework indicated that the difference in the centralized approach to guiding Shari'a interpretations in a jurisdiction, as in the case of Malaysia, and the decentralized approach in the GCC states, contributed most significantly to the regional variations observed. The Malaysian Shari'a framework is broader and more encompassing of the perspectives of the GCC Shari'a board members than the converse. Malaysia-specific applications of contracts such as bai' al ina and bai al dayn are likely to remain localized to Malaysia and more steps are taken for Middle Eastern interpretations to be integrated to the local market by welcoming GCC-based Islamic financial institutions into Malaysia. Additionally, dialogues among Shari'a experts have been conducted on a regular basis by both the private sector in Islamic finance – for instance the forums organized by Dallah al Baraka – and also at the level of international standard setting institutions such as the AAOIFI and the Islamic Fiqh Academy of the OIC and at the level of central financial authorities. These have been organized in Malaysia by the central bank of Malaysia, Bank Negara Malaysia, in the form of dialogues between Shari'a scholars of Middle Eastern and Malaysian backgrounds. The emergence of international Islamic financial hubs as well as these forums or dialogues indicates a harmonization and internationalization of Shari'a standards is taking place. It is at the regulatory level of the Shari'a framework that either a form of harmonization of fatawa will be carried out or a form of internationalization of fatawa from the GCC into other regions, such as Malaysia, will take place. And such a development can already be observed for the international dimensions of the Islamic fnancial sector, reflecting the internationalization of Middle Eastern perspectives into the Islamic financial sector of Malaysia. The internationalization may be interpreted to be one form of harmonization and it is likely that certain pockets of the Islamic financial sector will remain as they are, localized and Shari'a compliant based on the local Shari'a framework, primarily in the retail sector where there is less international interaction. Beyond these variations - which include some divergence of opinion on the permissibility of Islamic contractual applications to transactions and financial products - the linking thread is that all these instruments are considered Shari'a-compliant by different Shari'a board members. These variations could be due to the diversity of backgrounds, schools of jurisprudence, regions and regulatory environments in which Shari'a board members need to function. Considering such contexts, they may diverge in their sanctioning of products and divergence of opinion for subsidiary matters is permitted. The divergence of opinion that is existent regarding the application of certain Islamic financial contracts can be regarded as a simple adaptation of Islamic finance to distinctive local norms and at distinctive local regulatory environments, or simply put, divergence is a local adjustment that is necessary for Shari'a-compliant finance to function in different environments. (1) DeLorenzo, Yusuf. 'Shari'ah Compliance Risk', Chicago Journal of International Law 7 (2), Winter 2007, pp.1-12, p.1, 2 Figure 1: Commonalities in contract approval by Shari'a boards of key Malaysian authorities and the international standard-setting body AAOIFI  Your feedback and comments are very important to us, please feel free to contact the author via email. |

Opalesque Islamic Finance Intelligence

Kulliyyah Korner: Regional Variations on the Permissibility of Islamic Financial Instruments |

{kind=link}