RSS

RSS|

Bullion Management Group Inc. (BMG) established in 1998, offers the world's most secure, convenient and cost effective way of owning precious metals bullion. Currently, national and international investors can participate in the BMG Bullion Fund, the world's first open-end mutual fund trust that invests in equal dollar amounts of gold, silver and platinum bullion. As of 2009, this is Canada's largest Shariah-compliant mutual fund and the second largest in North America. Investors can also buy and store gold, silver and platinum bullion through BMG BullionBars. This is the most secure way to buy and store large amounts of bullion privately. Finally, BMG recently launched the BMG Gold Bullion Fund, which holds only allocated gold bullion. There are many ways of buying precious metals bullion. New, exotic investment vehicles appear each day as the price of precious metals rises and gold once again regains its status as an alternative currency. BMG has maintained its reputation as one of the world's safest and most secure bullion ownership companies by selling and managing only unencumbered bullion-we do not sell any form of proxy for gold, silver or platinum. Most people buy precious metals as insurance against the systemic failure of other currencies or markets. Were this to occur, these proxies would be difficult to exchange for the underlying asset they claim to represent. Q1. Can you provide some background to the philosophy behind the development of your bullion product range? What were the key deciding factors in developing such a product offering? I started this project (setting up BMG) in 1998 for a couple of reasons: First of all, looking at how the trends would change and I thought that equities and real estate were already overblown in 1998 but I was a couple of years wrong and I looked at what the opportunities were going to be going forward and I concluded that the opportunities were going to be in: Precious metals, Energy Sector (Oil, Gas & Uranium) and Water. This was because those sectors would do well regardless of where the economy was going. Secondly, my belief at the time was that the economy was not going to do well for a very long time. I came to the conclusion that someone entering a secular bear market would face serious financial issues along the way. So with that in mind I looked at the issue in Canada where investors could not hold Bullion in a Registered Retirement Savings Plan (RRSP) - which is the Canadian pension program for individuals. Being from the 'old school' where I look at Bullion as being money and I always consider you hold bullion in the same way that you hold cash in a portfolio, but this allocation would not depreciate with inflation. Given that you could not do that in Canada I looked at what was the best way to structure a securitized product that would qualify for RRSP and at the same time NOT compromiseany of the fundamental attributes of Bullion. We did not (at the time) set out to create a Shariah compliant fund, instead we wanted to create a fund that would not compromise the benefits of Bullion. The key attributes that we wanted to maintain where:

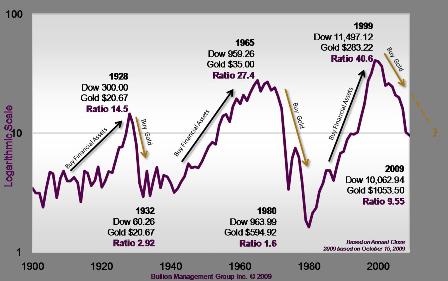

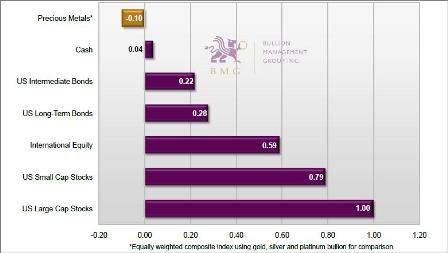

Q2. The development of your BMG Bullion Fund as a Shariah compliant product follows a very innovative approach, where you have retained your existing fund (which was launched in 2002) as opposed to launching a new one. Can you provide some background to this process, in particular with regards to the Shariah board? Has this been applied to other products under your suite? The three essential components of our investment philosophy mentioned earlier (and part of our legal structure) provided is with the ability to accomplish Shariah compliance because the underlying principles are the same. The Shariah compliant review did not require any changes and the overall turnaround was extremely quick. As a matter of fact the Shariah Scholars highlighted to us that “this has always been Shariah compliant without knowing it". For instance, part of he process to satisfy the compliance of the product involved obtaining supporting documentation from the custodians to certify that no interest was being paid on the cash balance. The Islamic Finance Advisory Board is an independent self-regulatory non-profit body, which provides Islamic Financial consultation services in Canada, and our team. This includes Shiraz Ahmed who is in charge of MENA business development and who worked closely with their scholars to ensure compliance (in fact it was Shiraz who initiated the compliance process). Their board includes Dr. Mohammad Iqbal Masood Al-Nadvi (Shariah Scholar & Board Chair), Dr. Hamid Slimi (Shariah Scholar), and Shaikh Nafis Bhayat (Shariah Scholar) and the overall experience has been very positive. Q3. Where do you see a bullion fund fitting within a Shariah compliant portfolio (or a conventional one)? Does one follow a similar allocation approach or have you found that Islamic portfolios are over/under allocated to this sector? If you think of Bullion as an investment then you would think of it is a commodity (like copper or zinc) and you will have difficulty understanding it. Bullion is not an investment per se but has been (and continues to be) money. It as been money for several thousands of years and indeed across all cultures and religions. Clear evidence of this lies with central banks across the globe which still hold just as much gold today as they did back in the 1980's. Although there has been much press giving the impression that they are all only selling. Precious metals are traded in the currency desks of all the major banks and brokerage houses, and not on the commodity desks. When you look at the $24 Billion turnover in the London market, it is clear to see that these are not jewelry buyers but instead currency traders. If you take the position of bullion as money-you do not lose purchasing power through inflation (in most cases you gain purchasing power). From a risk-reward perspective the decision is whether to put bullion at risk (i.e. invest it in stocks or bonds) and this implies that I might not get my money back. Hence if gold is going to be put at risk, one needs to be convinced that (based on an acceptable level of risk) I'm going to get more gold ounces back (on top of the principal investment). For example, even though it seems that the stock market has gone up, the dow/gold ratio was 44 to 1 in the year 2000 and now it is approximately 9 to 1. So investing 44 ounces in 2000 would receive 9 ounces back if the investment was cashed in today - so there is little incentive to invest in equities with that type of relationship. In that sense many questions that could be asked of a fund manager do not apply to us. Overall I would be hard pressed for someone to convince me that some investment right now is a better alternative than sticking to bullion. When looking at the vulnerabilities in the global financial system (currencies, equities, bond markets, sovereign debt, etc) there is more than enough evidence to say now is the time for bullion. Clearly at some point in the future, when P/E ratios approach 5, real estate has returned to normal levels, and interest rates are up 16 then maybe it will be time to deploy some of that bullion out. Figure 1: The Dow : Gold Ratio;  Source: BMG Q4. Have you explored diversification into other metals and/or commodities? Would this be feasible for a follow-up product? This might not be applicable to our overall strategy based on the three principles of bullion (which we outlined earlier) that we seek to benefit from. Q5. Would you prefer to consider deploying the current BMG fund in a different way? How does this relate to the fee structure? We have different classes of units suitable for retail, institutional, fee-based wealth managers, high net worth investors, etc. Curiously from our analysis of Shariah compliant investment products there is a stark limitation in the number of share classes offered (in fact most of the time there is only one, at best two share classes). This provides great flexibility in terms of offering this product to a wide range of investors so there is no great incentive to redeploy the same product. However if there was a institution that wanted to have a gold fund they could easily explore a white-label solution. Our retail management fee is 2.25% (and we pay 1% trailing fee to advisors) whereas our institutional management fee goes down to 0.5% (with a $50m investment). With regards to investors outside of Canada we are typically only open to accredited investors and this is our area of focus at the international level. Q6. Does the BMG Bullion Fund follow a specific benchmark and if so, how do you select it? Does this also impact the way by which correlation and/or diversification would be measured? Since we are a physical commodity fund, there is no real benchmark to be used. However that being said, a benchmark that could be used is a percentage of the London pm fix price: 33% gold, 33% silver, and 33% platinum as that is our fixed investment policy for the fund. Gold is the most negatively correlated asset class to the overall market and currencies (see the attached chart). For further reference, Ibbotson and Associates carried out a study that suggests having a portfolio allocation of anywhere between 5% to 15% would be considered fair (depending on a clients overall risk tolerance). Correlation Coefficients of Annual Total Returns, 1972-2004 Compared to US Large Cap Stocks  Source: Ibbotson Associates, Portfolio Diversification with Gold, Silver and Platinum, 2005 Q7. There are no derivatives of any kind being used under your strategy, it could even be labeled as a classic long-only, does this suggest it is a high beta or even a beta-only offering? Would an investment in the fund need to be reassessed periodically or is it meant for a long-term allocation? This is is not a classic fund, rather it is a classic "I don't want to invest" fund. Instead of delving in a money market fund or a cash fund, which is losing purchasing power every day, simply stay with bullion. When we receive inquiries as to why don't we hedge the canadian dollar, consider gold as the ultimate currency so why would we want to hedge? Hedging entails huge risks - in particular if the markets move beyond the parameters of your modelling. We leave it up to investors and their advisors to consider any particular hedging. Moreover, hedging using conventional derivatives would undoubtedly make the fund non-compliant with Shariah law, as this incorporates a speculative view on currencies (which would also increase your overall portfolio risk and ultimately increase the expenses for the fund). Q8. How important are the custodial and fund administration arrangements to ensuring the Shariah compliance of the product. What is the role and importance of these service providers in ensuring that the bullion fund maintains compliance? The custodian relationship has gained importance ever since the Bernie Madoff fraud. Our custodian for bullion is the Bank of Nova Scotia, but this does not mean we are renting vault space form them, rather they are acting as a trustee. There is a big difference since the trustee is responsible for the unitholders for the safekeeping of the bullion. Furthermore, under the OSC Securities Law (81 - 102) not everyone can be a custodian, only the five major banks in Canada can be custodian and others under certain exemptions. RBC Dexia does our fund accounting calculation of NAV, and they have sole signing authority on the fund's cash. We as managers focus on reviewing the statements, approve expenses, but have no ability to sign any checks on the fund. In terms of the flow of funds, money arrives from a financial advisor through the fund's trust account that is managed by RBC Dexia (as a sub-custodian), we then place call to to Bank of Nova Scotia to purchase the bullion and the confirmation slips (thru RBC Dexia). If this is as agreed-we authorize RBC Dexia to send payment for the bullion to Scotia. In the case of a redemption, we indicate to Scotia the redemption details and they the money back to RBC Dexia, and they in turn know who the redeeming financial advisor is so as to send the money to the client's account. This flow of funds and relationships makes it impossible to have a Madoff-type situation from occurring. Last but not least, KPMG as our auditor performs a third party audit of our fund and the bars-ensuring that the bars are all there and that the documentation matches (serial number, weight, purity, refiner etc). Q9. You maintain a maximum of 5% position in cash. Does this include any cash-equivalents? Does this allow sufficient flexibility in managing the fund's liquidity (matching inflows/outlfows, etc)? How do you mitigate any potential issues of concentration, liquidity or idiosyncratic risk? There are no cash-equivalents it is simply a non-Interest bearing cash account-while the maximum allocation is stipulated as 5% we have typically held less than 1%. This has been possible because of low levels of redemptions, so there is no need to maintain a large position in cash. Nevertheless we retain the ability to increase to 5%, which provide ample room to manage both inflows/outflows in the fund. Q10. What are the issues to be considered in terms of ensuring an effective placement/liquidation of positions? This is a good area of inquiry, ScotiaMocatta itself is one of the ten market-making members of the London Bullion Marketing Association (LBMA) and as a result they only deal in 'good delivery bars'. Their definition of a good delivery bar is outlined in an extensive document by the LBMA. Not only will they set out the specification for London good delivery bars, but in addition frequently perform audits of the refiner and further scrutiny/approval of facilities. These specifications are crucial and make bullion instantly liquid - as long as the bullion remains within the LBMA trading system. If it doesn't then it must undergo an additional audit to ensure that it meets LBMA standards again. Q11. Since the fund has an established AuM (of well over CAD $280 million) this presents an interesting dynamic. What would you consider the critical size for such a fund, what is the overall target size for the fund and when would the fund reach capacity? If we ran into size constraints then the price of gold would be 10,000 an ounce. There are no size constraints, if indeed we ran into a point where Scotia was unable to deliver any physical bullion then we would be forced to close the fund and investors will just have to sit there and watch the value of their investment goes upwards to 10,000 an ounce. Q12. How do you differ from other similar offerings in the market place today? There are other offerings in the market although there are some significant differences. For instance some gold funds, not to be confused with a gold ETF, which are basically closed-ended funds that will be listed and periodically they will issue new shares and use the money to purchase bullion. However this type of structure compromises our first point (that being the liquidity of bullion), since liquidity relates to the traded volume and for a listed fund of that size this won't be as liquid as pure bullion. For any large investor that wants to exit such a fund will result in a discount of the shares (and this would have an impact on other unitholders as well). We trade at NAV, we sell and redeem into the bullion markets, and it can't be anything but NAV. Our specific structure took time to setup as it had never been done before. We developed this particular structure over the span of three years, although we analyzed many other legal structures (we could have setup a closed-end fund in sixty days!) but this would compromise the very principles of bullion. The again the characteristics of an ETF lend it to be traded multiple times a day, but that is not what our fund is about. Your feedback and comments are very important to us, please feel free to contact the author via email. |

Opalesque Islamic Finance Intelligence

Fund Manager Interview: Interview with Nick Barisheff, President & CEO, Bullion Management Group Inc |

|

{kind=link}