RSS

RSS|

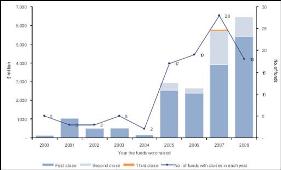

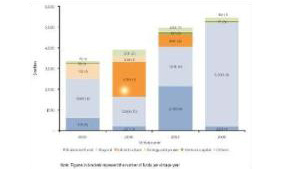

Sanad Islamic Investments is a Shariah compliant venture capital firm based in Jordan which provided VC fund management, venture creation, and advisory consultations on technology, media, telecom, education, and healthcare in the MENA region. Ahmed is Chairman & CEO of Sanad II, he completed his Ph.D. in 1996 in EE from the University of Alabama in Huntsville. He joined Photronix (Malaysia) as the R&D manager for the period 98-02 where he helped in starting up this venture, developing its products, securing funding and introducing it to the world. Later, he joined the Hashemite University where he served as the chairman of the ECE then EE departments for the period 03-07. He was short listed for both ASTF business proposal competitions in Riyadh '04 and Kuwait '06. He was invited as a jury member for QRNEC, QR scholarship program, SABEQ and other national committees. He also served in organizing committees of several international conferences. He has published about 20 technical articles and he recently was involved in starting up four ventures dealing with different technological-based products & services. He was recently certified by the American Academy on Financial Management as a Certified Private Equity Specialist. Q1. It has been often noted that the MENA region has a high degree of exposure to private equity investments' but not necessarily venture capital. Does this reflect an untapped market or do regional investors simply shun away from investing in start-ups or early stage companies? Private Equity in the MENA region is still facing challenges as the financial crisis unfolds both globally and regionally. Figures from GVCA, KPMG 2008 annual report shows (Figure 1) an increase in size of funds raised in 2008 compared to those in 2007. However, as 2010 is emerging, de-leveraging continues and cash available for the finance of this industry is scarce. Fund managers are having a hard time closing announced funds and it is more difficult for new funds to raise capital. It is further illustrated (Figure 2) that the VC industry is still facing more critical challenges. Although public and selected private organizations are trying to adopt and encourage establishment of western model of VC in the region, this industry is not bouncing back. The case in my opinion is challenged by many issues. Failure of regional governments on acting according to their belief of the critical role that the VC industry plays in building a sustainable economy comes on top of the list. An 'ecosystem' to help this industry flourish and to support currently seen entrepreneurial movement in the region is very much required. In particular, introducing entrepreneurship to the education system is of extreme importance. Not to forget the need to have continuous awareness of significance of knowledge-based economies. Consequently, weak deal flow suitable for VC industry has resulted. I also find it important to underline the risk-aversion business culture in the region being one barrier in the way of having the region to establish this much sought-after VC industry. Moreover, the business sector in this region has a strong appetite for quick returns. In summary, PE/VC industry in this region is not guided by long term economic strategies, and fund managers shun away from investing in start ups and early stage deals. However, we don't blame them since they act on the cash (short-term) interest of their investors, we appeal before them and all stakeholders to have hands together to solve this problem and face these challenges.

Q2. When it comes to identifying investment opportunities, do you observe any significant differences between conventional and Shariah compliant VC? What are the significant distinctions? Shariah finance continues to prosper and gain momentum worldwide and particularly in the region. According to the Ernst & Young 2008 World Islamic finance report, assets of this class is forecasted to exceed $2.7trillion by 2010. However, most of this growth has been so far on the development of As Shariah compliant VC firms come to the scene, we recognize significant differences when compared to their conventional counterparts. In regard to investment opportunity identification, we see that Shariah compliant firms avoid investing in unethical and Shariah unlawful products or services. These include the production and distribution of alcohol and pork-related products, arms industries under the current world regime, hotels, casinos, and conventional banks and insurance companies. Beyond that, it is generally accepted that any haram (improper) revenue of target investment counting for up to 5% of total revenues is considered a viable investment. In such a case, purification of income to count for this percentage of haram is commonplace. and this is usually done under the supervision of a Shariah board. Q3. The scope of Shariah compliant investment products now spans the entire globe, however do you find any specific areas (i.e. geographies, sectors, currencies, etc) which are still not properly covered by venture capital firms? Although Shariah compliant investment has widely spread, there are certain areas in MENA region that are considered of potential for growth. Some regional countries have taken more steps toward developing this industry than others. Jordan for example has taken the initiative of calling for proposals for managing two VC funds. The funds are anchored by Jordanian Government and European Investment Bank, and the fund is expected to be announced soon. However, countries like Syria, Iraq, Yemen, Sudan, and Algeria are of potential for VC industry deal flow. As to sectors, most of deals at the current stage are of IT field. This is justified due to many reasons including relative low barrier to innovated entry in this field. The huge market for social web services is another driver. Descent IT education in the region has helped as well. However, other sectors like agriculture, healthcare, and media are areas to be looked at carefully and require unleashing their potential. Some funds have started looking into these sectors specifically. Q4. Would you maintain that this universe of compliant investments carries a problem of quantity (more products needed) or quality (better managers needed)? Or both? In the context of improper industry avoidance relating to Shariah compliant VC, such sector restriction is not a foreign concept to investors. Fund investment diversification is a well-known practice in this investment arena. This implies having few sectors only under consideration of the fund managers. Moreover, alternative structures for Shariah compliance that is continuously developed by Shariah boards constitute a way to mitigate the quantity issue of this universe. However, I do believe we suffer a quality issue according to which more experienced people are to be attracted to this domain and trained on Shariah compliance rules. Meanwhile, Shariah boards are bridging some of this gap. Q5. The VC industry in conventional/traditional finance has matured over several decades, does this present Shariah compliant VC with a distinct limitation with regards to attracting experienced professionals and having the relevant background in seeding activities? It is widely accepted that the use of PE and VC within a properly constructed partnership is a true manifestation of Shariah business principles. This makes utilizing conventional VC experienced professionals seamless. However, and as I mentioned elsewhere, training on Shariah rules and guidelines to better perform their jobs is all what it takes those professionals to adapt to this universe. In fact, has the situation been otherwise, Shariah compliant VC would have suffered serious issues regarding experienced professionals and consequently regarding the performance of the industry as a whole. Q6. VC is by definition an illiquid investment product - to what extent can this be mitigated and are there any other issues (such as sector concentration, lock-ups, idiosyncratic risk, etc) that investors should be aware of? Shariah compliant fund based investment is as illiquid as its conventional counterpart. Nothing much can be done to manipulate this fact. Moreover, there are industrial sectors that are avoided due to Shariah rulings which ultimately come from the simple objectives of causing no harm and protecting the societies (these sectors were mentioned previously). However, due to structuring and ethical issues, Shariah compliant VC may be considered as lowering for example some of the conventional risk associated with this type of investments. In structuring deals, investors are given equal rights and borne equal risk although profit shares might vary. Leveraging is restricted to a situation where riba or interest is avoided. Q7. How do you see the VC industry developing in the MENA region �€“ in particular with regards to industry support for entrepreneurs and the level of innovation in the project pipeline? The VC industry is growing in the region. Reason behind that is improvement in deal flow especially in the IT field. This has been further motivated through the realization of success stories such as Maktoob. Furthermore, more people are realizing the importance of having a VC industry after the financial crisis has stripped-off some of the improper invested liquid allocation and the need to establish real economy. In addition to that, a strong VC industry is required if PE industry plans to sustain and prosper in the region. On the other hand, we have seen more public and private initiatives, in some countries like Jordan and UAE, targeting a complete 'ecosystem' in this domain which ultimately will support entrepreneurs and encourage innovation. We have started to see some of the fruits of these efforts manifested in the level of innovation in business plans seeking funding. Q8. What are some of the key trends that you are monitoring in the industry (with regards to new products, new markets, etc)? Which would you argue holds more opportunity and where is the greater potential for growth? Most of the MENA countries are relatively new markets for the VC industry. Some of these countries haven't seen any VC activities yet, although potential innovation in deal flow does exist. We look forward to tap such deal flows. Recession-resistant industries like healthcare and education are promising sectors that have not been fully explored yet as well. Other sectors like agriculture hold promise in this region especially if implemented in countries like Sudan. Turkey is one of the most promising markets in the region as well. If we extend our interest beyond this region, then areas like Southeast Asia and Central Asia are of potential markets to PE/VC industries. Overall, we are likely to see more of regional and global funds interested in Shariah compliant investments. |

Opalesque Islamic Finance Intelligence

Allocator Interview: Ahmed Muhammed Almanasreh, CEO, Sanad Islamic Investments |

|

{kind=link}