RSS

RSS|

By Amira Roula

Amira Roula researches trends

among systematic CTAs.

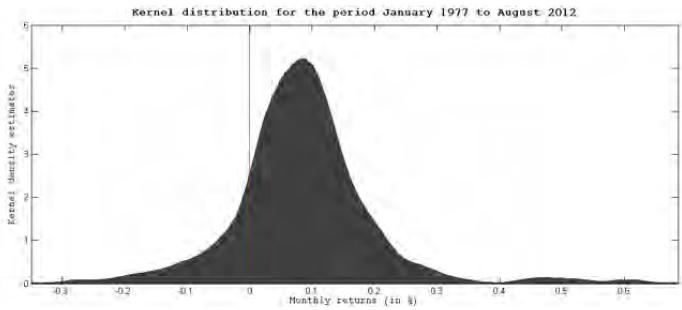

It is an interesting and much talked about combination of strategies, the systematic and trend following one. A small review may be in place, regarding qualitative as well as quantitative aspects. Systematic models and processes build on psychological regularities seen in the financial markets. These regularities are made into trading rules with which a systematic manager trades upon. For trend followers in particular, such regularities are defined as up and down trends. Being a trend following fund does not by necessity entail being systematic; discretionary trend following strategies do exist, and one is advised to keep in mind that there is a technical difference. You do of course have the programs where a mix between systematic and discretionary decision making is used. Being a trend follower is one of the most common strategies used by CTA managers, and in general, it would be quite difficult to build a managed futures portfolio that does not exhibit trend following attributes. One can see differences among trend following funds of course, something which comes mainly from the trading horizon used and the way the trading strategy is designed. These two factors, trading strategy and trading horizon play a differentiating role between the funds discussed. What does this entail in terms of fund categorization? It was mentioned earlier that the quality of a systematic trend following lies much in time horizon as well as the strategy plan laid out for that fund. Such parameters are not easily gained, as such information is rarely distributed in the databases available and the material provided by the managers. The information provided is not enough to do a quantitative analysis on. For example, when a manager states the trading is done on a "long-term" basis, what does that mean in terms of holding period? Are we talking about weeks, months or years? "Short-term", is that nano-seconds or days, even weeks? The second factor we mentioned, strategy plan, is much more difficult to come to grips with. Usually, a fund is described in more or less layman terms, and in the rare case where more detailed information is given, it is still difficult to make a clear judgment about how sound the strategy is. Fund descriptions in general make lousy variable inputs when one wishes to do an in-depth quantitative analysis. It is of course difficult to balance the need for secrecy and transparency; to do a deeper analysis, a more qualitative approach is what one would have to use. Writing about how this strategy combination has fared, in past tense, cannot be done without mentioning past returns. The mean historical annual return has been quite average at 8.43% compared to the CTA sphere overall which had an annual return of 11.58%. And here comes the discussion about survival rate versus returns. Though they do not seem to yield the best performance (as compared to peers), the systematic trend followers do have a lower tendency to simply "blow up". The more quantitatively inclined reader might want more numbers explaining why trend followers appear to have such a return and survival rate, something a kernel density plot might provide us with. In short, a kernel density estimation takes a sample (ex. our returns from our selected funds) and makes an inference about how these funds would behave in general, in terms of returns.

The systematic trend following programs analyzed have a kurtosis of 7.91 and a skewness of 0.892. Of interest to note is that different CTA strategies have quite diverse figures regarding higher moments such as kurtosis and skewness. A high kurtosis indicates a higher probability for extreme outliers, which we also see from the tails in the figure above. The skewness of the plot is not straightforward to interpret; we see a short but fat left tail, and a long right tail. That this asymmetry evens out is also shown by the skewness being positive but quite small and close to zero. We still have the case that the plot estimates more positive outliers than negative ones. The structure of its probability density might explain its traction with managers; that, and the fact that setting up a trend-following strategy is in theory quite easy. As we know however, how this is interpreted in terms of implementation and risk management, i.e. the strategy plan, is important in setting you apart from the rest of the flock. One would at this time take note that we have yet to mention variance or standard deviation; for the curious reader, semi-standard deviation does not deviate much from the standard deviation, at 5.76% and 5.71% respectively. Such point-in-time figures are nice to look at, but the overall structure and distribution of the returns is much more interesting. Taking the quantitative and qualitative aspects of the individual funds and managers together, you will get a fair idea of what you might get yourself into. Simply looking at the numbers though, one might get lost in the false assurance of temporarily nice numbers. The values we have discussed are mean values, over a certain period in time (from January 1977 to August 2012). Furthermore, we have not touched upon the issue of market allocation and fund size. Or fund organization. And many other aspects that in the end are the criteria with we actually asses particular or mixes of fund allocation. One does look forward to ways in which to better assert whether one particular fund or manager is worth investing in, or how a smaller pool of managers would do in a portfolio. For the more adventurous investor, wanting higher yields but the burden of "fund-blow-up" becoming a larger threat, other strategies may be of interest. If one does wish to invest in CTAs, it is of course interesting to ask oneself if a mix of strategies might be of interest, and continuously looking at calibration and fine tuning of that mix. Amria Roula Background: Amria Roulahas an MSc in Finance from Stockholm School of Economics (SSE), a BSc in Industrial Engineering / programming design from the Royal Institute of Technology (KTH), an MSc in international management from CEMS/HEC Paris and a BSc in accounting and finance from SSE. With a fascination for alternative investments and risk management, Roula focuses on creating order out of chaos. Amira has worked in a fund of hedge fund, the corporate finance division of a large Swedish bank and the IT-department of another, worked with health economics and other fields in finance as well as IT. When not working, Amira loves to do sports in a multitude of formats, going out for coffee and learning new languages. |

|

This article was published in Opalesque Futures Intelligence.

|

{kind=link}