RSS

RSS|

By Lorent Meksi

Lorent Meksi's work shows that selecting large CTAs based on recent performance makes it difficult to outperform industry benchmarks.

When investing in managed futures, how easy is it to beat the benchmark? Every investment is judged on how well it does not only on an absolute basis, but also relative to a benchmark. In addition to generating profits, the goal of any investment is to beat the benchmark. If you beat the benchmark, whether by luck or skill, you will be viewed as a genius and will be compensated accordingly. If you deviate from a benchmark and fail to add value, you will look foolish and be exposed to significant career risk. As investment professionals, we live with this reality on a daily basis. It is the nature of the game and we accept it. We would all like to think that we can beat our benchmarks. We work hard to create investment processes, follow rules and take calculated risks - all with the purpose of achieving that goal. When the work is done and we see favorable results, we start to believe that outperformance of the benchmark is indeed easy. Managed futures, aka CTAs, have a long history, but the wider investment community became more interested in the asset class after 2008 when it provided dramatic downside equity protection. The typical path for an investor begins with a decision to allocate to the asset class. Once that decision is made, the next logical step is to determine the best way to access the industry's returns. There are many ways to access the industry's returns, including: single managers, multi managers, and platforms. As evidenced by the high concentration of asset under management ("AUM") in the largest CTAs, many investors choose to go with the more established managers. "Many investors evaluate returns and conduct portfolio benefit analysis on managed futures benchmarks that are not investable and then construct their own CTA portfolios with inherent tracking error." Many investors evaluate returns and conduct portfolio benefit analysis on managed futures benchmarks that are not investable and then construct their own CTA portfolios with inherent tracking error. As the research partner with STOXX� in creating the iSTOXX� Efficient Capital� Managed Futures 20 Index, Efficient Capital Management has made a CTA benchmark investable to those seeking to access industry returns while limiting tracking error and benchmark risk. Should investors use an index to access managed futures returns, or should they build their own concentrated portfolio by investing in a few hand-selected managers? With the iSTOXX Efficient Capital Managed Futures 20 Index serving as the benchmark return, how easy is it for investors to create their own portfolio that outperforms that benchmark? It is certainly quite easy to select a group of managers today, run a proforma, and show that the portfolio with full hindsight bias has outperformed the index. However, if you were to step back in time, would you have chosen those same managers using only the information that was available at that time? This article attempts to address these questions and present evidence that suggests that outperformance of the index can be challenging. When investors select CTAs, we believe they value two main factors: size and recent performance. The average institutional investor invests in the large managers ("Biggest") and managers that have performed well recently ("Best"). To model this behavior, we have gone back in time and created hypothetical portfolios based on these two factors. By simulating manager selection decisions based only on information that would have been available at the time of selection, we essentially create the "Biggest" and "Best" portfolios without the benefit of hindsight. These portfolios were then compared to the historical performance of the iSTOXX Efficient Capital Managed Futures 20 Index. The analysis shows that the "Biggest" and "Best" portfolios generally underperform the index. In the remainder of the article we explain our assumptions, show the results and offer some reflections. ASSUMPTIONS & METHODOLOGY The iSTOXX� Efficient Capital� Managed Futures 20 Index ("index") - The Index is developed by STOXX in collaboration with Efficient Capital Management, a leading investor in the managed futures space. The index has 20 constituents, is completely rules-driven and is representative of the Managed Futures industry's leading managers by assets under management. Twenty constituents is a sufficient number to ensure a representative return of the Managed Futures industry at large due to the heavy concentration of assets with the largest managers. STOXX independently constructs, calculates and publishes the index value on a daily basis, while Efficient Capital serves as the research partner. Index Methodology: • Minimum of USD 100 million AUM Monthly Rebalance - The 20 managed futures traders will be equally weighted after adjusting for volatility. This ensures that every manager has an equal risk adjusted impact on the index return. The rolling 36-month volatility is used. "Size" factor - The size factor refers to the AUM for a given manager. Much research has been done on the relationship between size and future performance. Academics aside, most investors tend to avoid small managers. As a matter of fact, many investors have rules to purposefully prevent them from investing in small managers. Asset concentration among the top managers is evidence of this fact. Investing with large managers can mitigate headline risk among other things. And although current size may or may not have correlation to future performance, current size most likely is a reflection of recent performance. "Performance" factor - This factor simply refers to the recent performance of a manager. No matter how you look at things, performance is the most important factor in determining whether to invest. We suspect that few presentations of poor-performing managers (either on a relative or absolute basis) are brought before investment committees. Manager universe - For the purposes of this study we kept the investment universe limited to the constituents of the iSTOXX Efficient Capital Managed Futures 20 Index. Since we make the assumption that investors value size when investing in managers, we believe it is fair to limit the universe to 20 of the biggest managers in the industry. There are benefits to making this choice. The performance data is clean and of high quality given the small and focused data sample. In addition, the performance data is less prone to some of the biases that are typical of hedge fund databases. The universe is comprised of exactly 20 managers every year changing annually to reflect the index constituents. "Biggest" portfolios - We use the size factor to create the "Biggest" portfolios. Every December we rank the 20 managers by AUM and then select the top one, three and five. We hold these equally weighted portfolios for the following year until we rebalance again the following December. "Best" portfolios - We use the performance factor to create the "Best" portfolios. Similar to the "Biggest" portfolios, we create and rebalance one, three and five-manager portfolios every December. We use two measures of performance to determine manager selection: absolute returns and risk-adjusted returns. For absolute returns, we use the average annual return for the past three years and for risk adjusted returns, the trailing three year return-to-risk-ratio. Data - We use monthly net returns throughout our analysis. Data sources include a combination of BarclayHedge, Efficient Capital and Bloomberg. Since we are comparing all the portfolios to the iSTOXX Efficient Capital Managed Futures 20 Index and the look back period for the performance selection criteria is three years, all the comparisons start in January 2003 and end in December 2012. BIGGEST AND BEST vs. THE INDEX The following charts represent the risk-adjusted performance (i.e., normalized to 12% volatility) of the "Biggest" and "Best" portfolios relative to the index. The first chart represents the performance of the "Biggest" portfolios. All three portfolios compete well. The one and five manager portfolios slightly outperform the index and the index outperforms the three manager portfolio.

The second chart represents the "Best" portfolios, using the absolute return selection criteria. This investment strategy has clearly been inferior to investing in the index. The one manager portfolio was a good competitor for a time, but in recent years the index has prevailed over all three portfolios.

The third chart represents the "Best" portfolios as defined by the return-to-risk selection criteria. These portfolios compete better but, in the end, the index prevails.

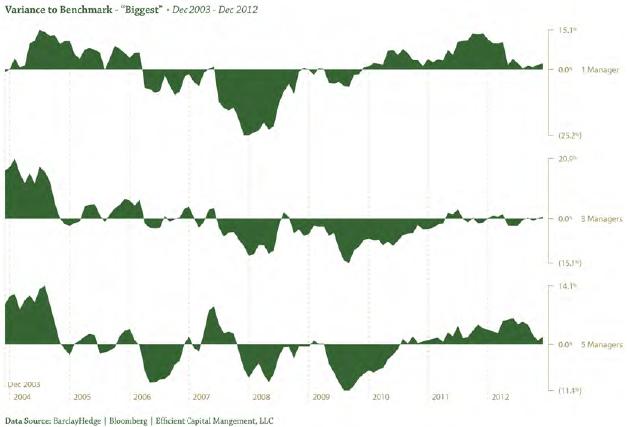

So far we have seen that "Biggest" and "Best" portfolios (chosen based on return-to-risk ratio) compare well with the index. Let's now take a closer look at "Biggest" portfolio variance to the index over time. Although most investors aim to be "long term", the path of each investment (i.e., variance to benchmark and drawdown) tends to matter a lot. THE PATH OVER TIME The following chart shows the rolling annual return variance for each of the "Biggest" portfolios from the index (+10% means the portfolio outperformed the index by 10% over the last rolling year, while -10% means that the portfolio underperformed the index by 10% over the last rolling year). As the following chart of risk-adjusted returns illustrates, there have been periods where the portfolios have outperformed the index, but in all three cases, the underperformance has been larger. This is an important data point since we all know that we tend to feel losses more than gains.

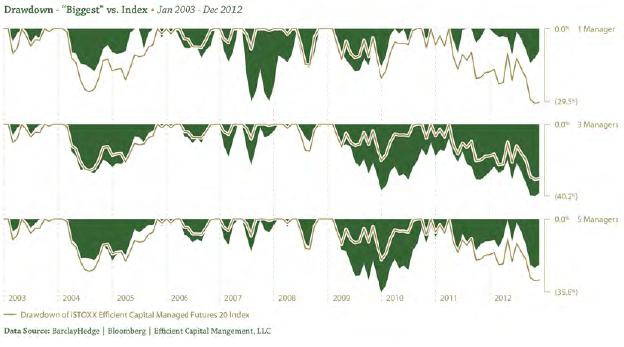

The next chart offers another insight into the path of these investments as we compare the volatility-adjusted drawdowns between the "Biggest" portfolios and the index. The shaded portion of the chart indicates the drawdown of a given portfolio while the line marks the drawdown of the index. As you browse through the charts, you will see that, with a few exceptions, the index tends to have a more robust profile.

REFLECTIONS: Outperformance of the diversified portfolio (index) over a multi-year horizon by constructing a concentrated portfolio of managers based on the "Biggest" and "Best" criteria has been challenging.

This analysis makes some intuitive assumptions about how the average institutional investor may approach their managed futures investment decision. The comparative analysis was completed on portfolios that were created without the benefit of hindsight, using only information that was available at the time of the investment decision. By conducting "honest" backtests, we have demonstrated that the index compares favorably to concentrated portfolios of the "Biggest" and "Best" managers. Although the analysis might indicate otherwise, we are not suggesting that the index is the best way to gain exposure to managed futures. We are simply suggesting that investors should be careful before concluding that it is easy to outperform their managed futures benchmark. Lorent Meksi Background: Lorent Meksiis a Director and a member of the Investment Team at Efficient Capital Management, LLC. Prior to joining Efficient, he wasan options trader for Efficient Capital Overlay, LLC where he started his career and remained until 2006. Mr. Meksi graduated from North Central College in 2003 with a BS in Computer Science and a BA in International Business. He received his MBA degree from the University of Chicago Booth School of Business in 2012.Mr. Meksi holds a Series 3 license, and has been in the industry since 2003. COMPLIANCE NOTES STOXX STOXX Limited, its owners, data sources, business partners and agents (the "STOXX Parties") have no relationship to the Efficient Capital Management, LLC, other than the licensing of the iSTOXX� Efficient Capital� Managed Futures 20 Index and the related trademarks for use in connection with the iSTOXX� Efficient Capital� Managed Futures 20 Index. The STOXX Parties will not have any liability in connection with the iSTOXX� Efficient Capital� Managed Futures 20 Index. Specifically, the STOXX Parties do not make any warranty, express or implied, and disclaim any and all warranty about: the results to be obtained by the iSTOXX� Efficient Capital� Managed Futures 20 Index, and the data included in the iSTOXX� Efficient Capital� Managed Futures 20 Index; the accuracy or completeness of the iSTOXX� Efficient Capital� Managed Futures 20 Index and its data; the merchantability and the fitness for a particular purpose or use of the iSTOXX� Efficient Capital� Managed Futures 20 Index and its data; the STOXX Parties will have no liability for any errors, omissions or interruptions in the iSTOXX� Efficient Capital� Managed Futures 20 Index or its data; under no circumstances will the STOXX Parties be liable for any lost profits or indirect, punitive, special or consequential damages or losses, even if the STOXX Parties know that they might occur. Benchmark Data Benchmark data was obtained from various internal and external sources, such as CTA databases, Bloomberg, International Traders Research Inc., Hedge Fund Research, and Newedge. Efficient believes the benchmark data to be reliable, but can make no warranty as to its accuracy. Efficient has not and cannot verify the accuracy of all such information and the recipient should be aware that the information is presented on an informational "as-is" basis and is subject to change without notice. |

|

This article was published in Opalesque Futures Intelligence.

|

{kind=link}