RSS

RSS|

By Galen Burghardt, Ewan Kirk, Lianyan Liu In a recently released strategy note, Newedge researchers Galen Burghardt and Lianyan Liu teamed with Ewan Kirk of Cantab Capital Partners to consider an often discussed issue: Is there a capacity issue with managed futures. The research team dives deep into issues of futures market open interest relative to a variety of factors, including its flexibility, distribution over various time horizons, as well as examining liquidity and capacity spill-over effects. To view the full report, click here.

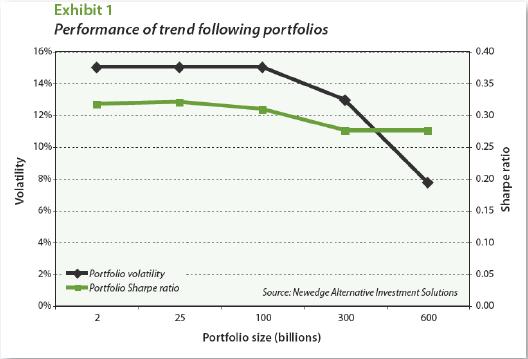

Galen Burghardt (left), is director of research at Newedge, and Lianyan Liu (right) is a quantitative financial analyst at the firm. Ewan Kirk of Cantab Capital (not pictured) was the motivating force behind the research note. Our purpose in writing Managed Futures for Institutional Investors in 2011 was to help clear the way for the possibility of doubling the size of the industry. While ambitious, the goal seems well within reach. Since then, the industry has grown somewhat and now manages roughly $330 billion. At the same time, the industry finds itself in a drawdown that is, by the industry's standards, relatively deep and relatively long. The current drawdown at this writing is two years long. And at its worst (so far), the drawdown was -9.3%. The growth in assets combined with the current drawdown has prompted investors to ask three related questions. What is the industry's capacity to deliver uncorrelated returns with a reasonably high Sharpe ratio? How large can an individual manager be? And, a truly interesting question for a large institutional investor, how large an investor can I be? This note mainly addresses the first question, although the framework we work with allows one to think about the second two questions as well. To do this, we explore the position sizes that an industry dominated by trend following would require to meet a return volatility of 15% and compare them with open interest in a wide range of markets.  Probably the most useful insight gleaned from this exercise is that if open interest constrains the industry's position, we can conclude that the first thin. But, as shown in Exhibit 1, the degradation of the industry's Sharpe ratio would bottom out once maximum position sizes had been reached in all tradable markets. At this point, increases in the size of industry would serve only to dilute the industry's returns and, as a result, its return volatilities. Every dollar added to the denominator of the industry's return calculation, with no increase in the returns that constitute the numerator, simply spreads the industry's returns over a broader asset base. The work described here is meant to be a framework for thinking about the problem of capacity. The final product should be useful in a number of ways.

We conclude with a discussion of three points that we think would mitigate concerns about capacity constraints. These are:

Futures markets are generally very liquid and likely would have no trouble accommodating a much larger industry's positions or the trading that would accompany changes in market direction. The single medium-term trend following manager approach For the purposes of this discussion, we will assume that the entire industry can be treated as if it were a single manager who employs a medium trend following model - in particular, the Newedge Trend Indicator model - that uses a single set of look-back parameters over a broad set of markets and that is always in the market.1 Using a slightly modified version of this model, we can calculate hypothetical position sizes for the industry at various levels of assets under management, compare them with the sizes of the various futures markets, and consider how the model's performance characteristics would decay if its position sizes are constrained by open interest in those markets. The main argument for such an approach is that the industry is dominated by trend following - much of which can be described as medium-term to long-term trend following. Trend following returns are the dominant signal in any index of CTA returns. Perhaps the single greatest strength of the Newedge Trend Indicator model - or any similar medium-term trend following model that trades a wide range of markets - is that it allows us to approximate the sizes of the positions that trend following CTAs take in various markets. Thus, even though trend followers tend to enter and exit markets at different times, at some point, most successful trend followers' positions sizes and market directions will overlap much of the time. And at these times, the approximations afforded by the Trend Indicator will allow us to glean insights into where the stress points might be. The arguments against such an approach are several.

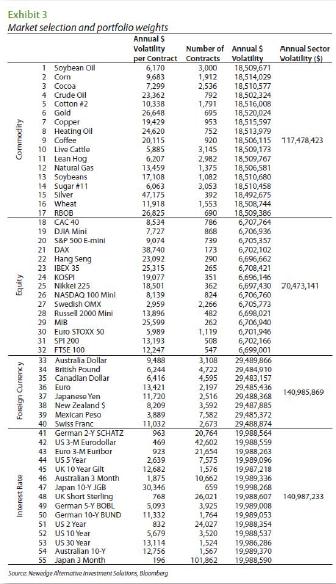

Even so, as we have been reminded many times, if one doesn't assume something, one cannot even begin to answer questions about the industry's capacity. In fact, the assumption that underpins this discussion is hardly the worst and has the redeeming virtue of allowing us to learn something useful about how the industry's growth may influence its risk-adjusted returns and return volatilities. For that matter, a simple model allows you to get some insight into a more complex problem. The Universe may not be one sun and one planet, and they may not be point masses, but this simple model can give you a great deal of insight into the more complex Universe. A broadly diversified trend following portfolio The key elements of any trend following model are the markets that it trades, the momentum rules that it employs to trade those markets, the risk that it allocates to each market, and the overall risk that the portfolio strives to achieve. For the purposes of this work, we use the same 55 markets that are used in the construction of the Newedge Trend Indicator. This is a broad and representative set of markets that cover currencies, interest rates, equities, and commodities. We also use the same momentum rule - a 20-day/120-day moving average model - that we use

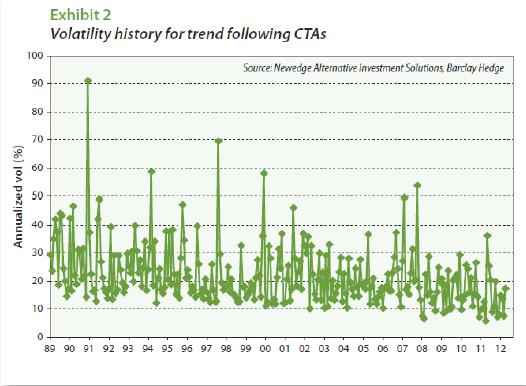

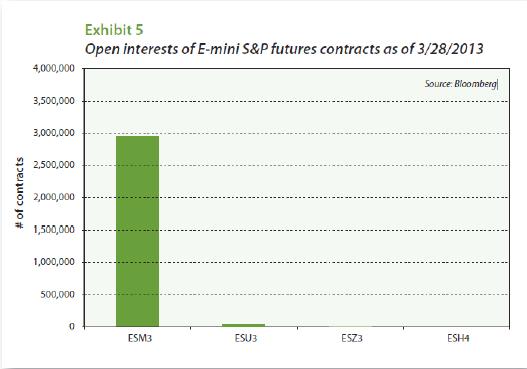

And within these sectors, we strive to allocate equal amounts of risk to each market traded within a sector. Our experience suggests that these allocations vary widely across trend following CTAs, but that the set we have chosen yield portfolio returns that are reasonably well correlated with trend followers' returns.  The last piece of the puzzle is the overall risk target, for which we have chosen a 15% annualized return volatility. As shown in Exhibit 2, such a target falls roughly in the middle of the range of return volatilities that trend followers have delivered for the past decade or so. To finish the job of constructing the portfolio, we chose a notional portfolio size of $2 billion and used Before leaving this section, we should note that the position sizes shown in Exhibit 3 are the product of two kinds of volatilities. One, of course, is the portfolio's volatility target of 15%. The other, though, is the expected volatilities of the 55 markets traded. The portfolio shown here is based on 2012 market volatilities, which were relatively low when compared with many earlier years. One consequence of an increase in market volatility would be a decrease in overall position sizes to maintain a target volatility of 15%. Open interest Open interest in futures markets measures the open long (or short) positions at any given moment and represent, in a sense, the amount of risk that traders - both long and short - choose to take in the form of futures contracts. Before embarking on the work of seeing how CTA returns might be affected by a substantial increase in assets under management, we would like to touch on three matters that merit consideration. These are: (1) the fluid nature of open interest; (2) the varied distributions of open interest across contract months; and (3) the CTA industry's preference for trading currencies in the over-the-counter forward market.  The fluid nature of open interest In practice, the number of open positions is fluid rather than fixed and varies over time as new positions are taken or old positions are offset and closed out. Unlike a market for equities or bonds, where the total amount of risk that must be taken is determined by the value of equities or bonds outstanding, the amount of risk taken in futures markets - as measured by open interest - is a matter of choice. And any given trade can produce either an increase, decrease, or no change in open interest. For example, if someone who is already long futures buys futures from someone who is already short futures, open interest will increase. If someone who is already long futures sells to someone who is already short futures, open interest will decrease. And if someone who is already long futures sells to someone who is also already long futures, the result will be no change in open interest.2 To illustrate this point, we have provided open interest histories for four commodities in Exhibit 4 - one for crude oil, one for British pounds, one for the S&P500, and one for 10-year treasuries. All four have been normalized so that open interest in 1995 is indexed at 1.0. Notice first that open interest in all four markets has grown substantially over the period shown, although the path taken by 10-year treasury futures has been radically different from the other three. With the exception of the equity futures contract, open interest today is substantially larger than it was ten years ago. It is a bit odd that open interest in equity futures has fallen over the past five years, but as we will find, equity futures markets will prove to be the least constraining in this exercise. The distribution of open interest across contract months In government bond, equity index, and currency futures, nearly 100 percent of the open interest will be either in the “lead” contract (i.e., the contract that is about to expire) or in the “first deferred” contract (i.e., that contract that is about to become the lead contract). An example of what the distribution of open interest in e-mini S&P500 futures looked like on March 28, 2013, is provided in Exhibit 5. This pattern will hold until market participants want to shift their risk taking to the next most active contract month. In the case of equity index and currency futures, this shift typically takes place in the week before the lead contract expires. In government bond and note futures, the shift depends on the market. In the case of U.S. Treasury futures, the shift takes place during a few days toward the end of the month before the lead contract expires - chiefly because most futures participants want to avoidany possibility of taking delivery of actual bonds. In the European and Asian markets, where delivery rules are different, the shift tends to take place closer to the lead contract's scheduled expiration.

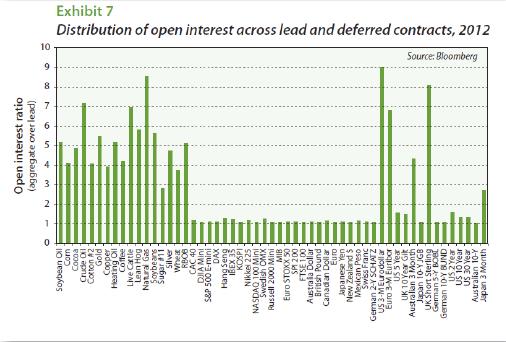

Commodity futures, on the other hand, make much fuller use of deferred contracts. Exhibit 6 provides an example of the distribution of open interest in crude oil futures across contract months. As you can see, there are ample open positions in many of the deferred contracts. A summary of these patterns is provided in Exhibit 7, which shows the ratio of total open interest to lead contract open interest for the 55 markets traded by the Newedge Trend Indicator. In the work that follows, we use each market's total open interest. Foreign currency markets Perhaps the only market in which transaction economics favor over-the-counter trading over futures trading is the currency market. For this reason, the greater part of currency trading done by CTAs is done in the forward market. This raises a practical problem for us because there is no analog for open interest in the over-the counter market. At least no analog for which there is a useable measure.

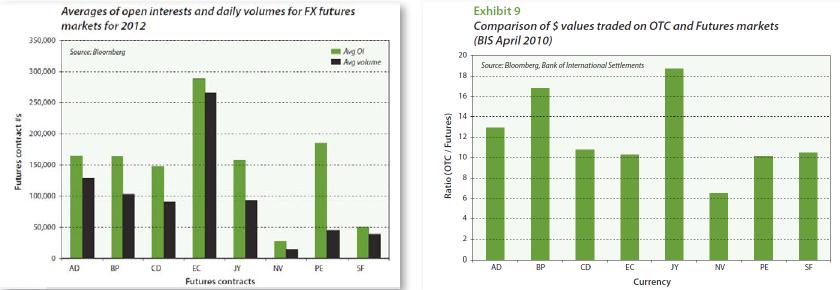

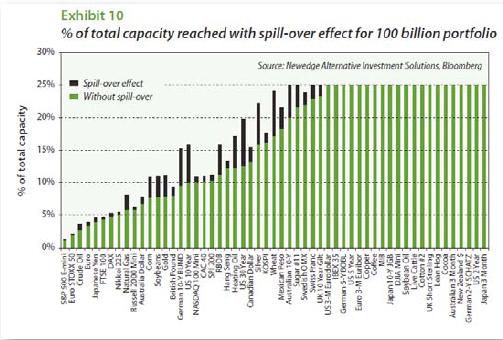

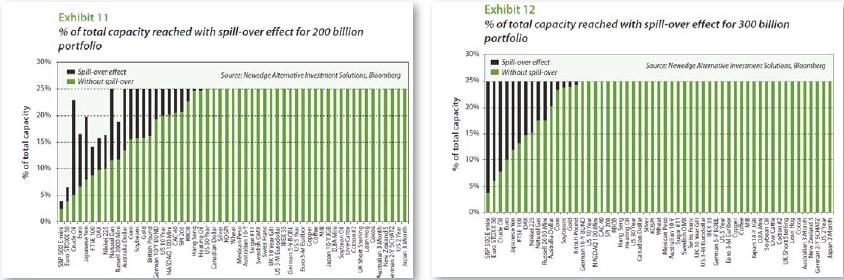

To deal with this, rather than trading the currency market as a boundless source of trading positions, we applied the following logic. First, we can compare open interest and trading in the futures market. Exhibit 8 provides average values for 2012. Second, we can compare futures trading with spot and forward trading using a survey that BIS coordinates once every three years. Exhibit 9 shows the April 2010 ratios of over-the-counter spot and forward trading to futures trading for the currency markets in our model portfolio. Then, with these two sources of data, we apply the ratio of open interest to trading volume that we observe for futures to the trading that we observe in the over-the-counter forward market. The result is a synthetic open interest value for over-the-counter currency trading that we can express in futures contract equivalents. While this is a bit of an approximation, for the purposes of this paper, it seems both reasonable and robust.  Confronting the model with open interest constraints We are now ready to consider what would happen with the trend following model if it were to confront the open interest constraints developed in the previous section. We want to be clear, though, that we are treating open interest as a constraint solely for the purposes of this exercise. Even so, we think that the lessons of this section are worth considering. First, the exercise shows which markets are more likely to be crowded than others as the industry grows. Second, the exercise traces out the sequence of effects of growth on CTAs' risk-adjusted returns and on their return volatilities. Consider the sequence of Exhibits 10, 11, and 12. In each case, we have chosen (arbitrarily) to limit the model's share of any one market to 25% of that market's open interest. Exhibit 10 corresponds to assets under management of $100 billion, Exhibit 11 to $200 billion, and Exhibit 12 to $300 billion. In these exhibits, the least constrained markets are on the left, while the most constrained markets are on the right.

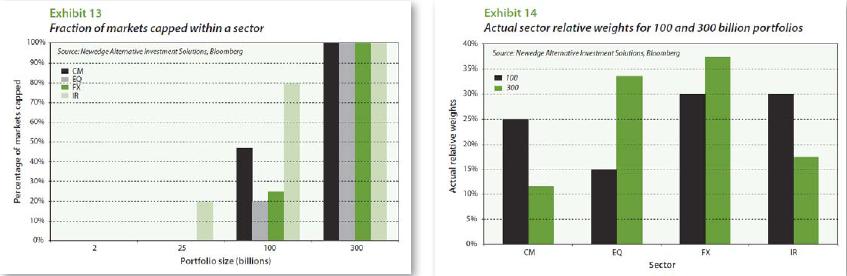

Perhaps the most interesting insight to be gained from this work is the CTA industry's likely response to crowding. It is important to know that most, if not all, CTAs strive for two things - a high risk-adjusted return and a target return volatility. Thus, if a CTA reaches what it considers to be the limit of risk it can take in any given market, its most likely response is to allocate any unmet risk to other, less crowded markets, first within the same market sector, second to other market sectors. Exhibit 10 begins with a $100 billion portfolio and shows the positions taken in each market as the sum of two decisions. The bottom portion of each vertical bar shows how much the model would want to allocate to that market up to the 25% constraint. The top portion of each bar shows much risk the model has reallocated to each market in an effort to maintain the portfolio's risk allocation across sectors and the portfolio's overall risk objective of 15% volatility. In a sense, the markets on the left are the shock absorbers, shouldering any risk that the constrained markets are not allowed to bear. Note that four of the markets are capped out because of risk that has been reallocated to them - the UK gilt contract, Swiss francs, Sugar, and the Australian 10-year note contract. Exhibit 11 moves to a $200 billion portfolio, for which a greater number of markets are constrained, both outright and because of risk overflow. Even so, there are a number of markets on the left that remain unconstrained. At $300 billion, however, as shown in Exhibit 12, the 25% limit has been reached for all 55 markets, either because the model's position exceeded the limit, or because the model has allocated more risk to the remaining markets than can be accommodated by the market.  At this point, the portfolio has nowhere to turn. Diversification is limited by the size of the market. For that matter, as the position size has grown, the portfolio has gravitated more and more to what would be called a market portfolio. The progression from relatively unconstrained to fully constrained portfolio is illustrated in slightly different ways in Exhibits 13 and 14. In Exhibit 13, you can follow the fractions of markets within each sector that are capped as the portfolio grows from $2 billion to $300 billion. At $2 billion, which would represent a reasonably large CTA, almost nothing is constrained, while at $25 billion a relatively large fraction of interest rate markets are constrained. By the time we reach $100 billion, some markets in all four sectors are capped. And, as we know from Exhibit 16, once the portfolio reached $300 billion, all markets in all four sectors are capped.  In Exhibit 14, you can see the difference between the portfolio's target weights and the market weights that would result from constraining the portfolio to hold no more than 25% of the open interest in each market. The point of this exhibit is not that the target weights are necessarily the correct ones, but rather than the market portfolio likely is different from the industry's target portfolio. This leads to the question of how the industry's returns and risk would be affected by open interest constraints. This is a partial report. To view the full report, click here. Acknowledgement: We want to thank Ewan Kirk of Cantab Capital Partners both for encouraging us to pursue this question of the industry's capacity and for his active participation in the research. It is a thorny topic with no clear solution in sight, so his confidence that a simple model could yield useful insights into the question of capacity and into the rich complexities of the markets involved inspired in us the confidence to press forward with the work and publish this note. It has been a satisfying and lively collaboration for which we are truly thankful. Footnotes: 1) A description of the Newedge Trend Indicator model can be found in Two benchmarks for momentum trading, which is Chapter 5 in Burghardt and Walls, Managed Futures for Institutional Investors (Bloomberg Press, 2011). 2) Perhaps the closest analogy one can find in securities markets is the practice of shorting stocks or bonds. These trades create the appearance of a larger quantity of the security. It is not possible, however, to reduce the apparent supply of a security. |

|

This article was published in Opalesque Futures Intelligence.

|

{kind=link}