RSS

RSS|

IS THE TREND YOUR FRIEND?

Lara Magnusen is Vice President and

Director of Investment Products at

Altegris and has a background in

research as well as seeding managers

The historical benefits of managed futures investing have been well documented. As an investment strategy that has delivered positive absolute returns over time with very low correlation to traditional long-only strategies, coupled with a seemingly remarkable ability to perform best during periods of upheaval and financial crisis, managed futures have become increasingly popular as a core long-term diversifier for investors' portfolios. After many years in which managed futures were restricted to ultra-high-net-worth individuals and institutions, the advent of lower-minimum hedge fund access and now mutual funds and ETFs have increased the availability of the strategy for the financial advisor community and the mass affluent market. As is often the case in the investment world, an expansion of popularity and market reach has unfortunately coincided with a sustained period of disappointing performance for managed futures investors. Not only are many industry observers now questioning the efficacy of the strategy, but investors are re-examining their allocations to managed futures and the asset class' place in their portfolios. This is especially troublesome for investors who may be underweight equity markets, and are watching as equity indices successfully scale new heights on the wall of worry. In this white paper we examine the characteristics of managed futures, and examine the specific market dynamics that we believe have created a difficult environment for the strategy post-Global Financial Crisis. Importantly, we look forward and ask whether it is time for those dynamics to begin shifting back in favor of managed futures investing. Our core conclusions are:

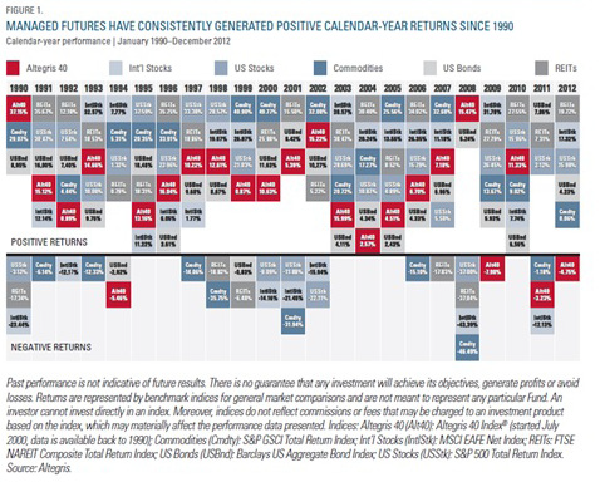

Recent Performance Within a Long-term PerspectiveTo say that managed futures have struggled over the past few years might seem patently obvious-the strategy has, after all, suffered negative calendar-year performance in three of the past four years, and delivered its first back-to back losing years since 1990. However, examining market behavior over the past 20-plus years may help put the recent performance of managed futures into perspective, and provide investors with some comfort that current returns are not somehow a proverbial new normal.

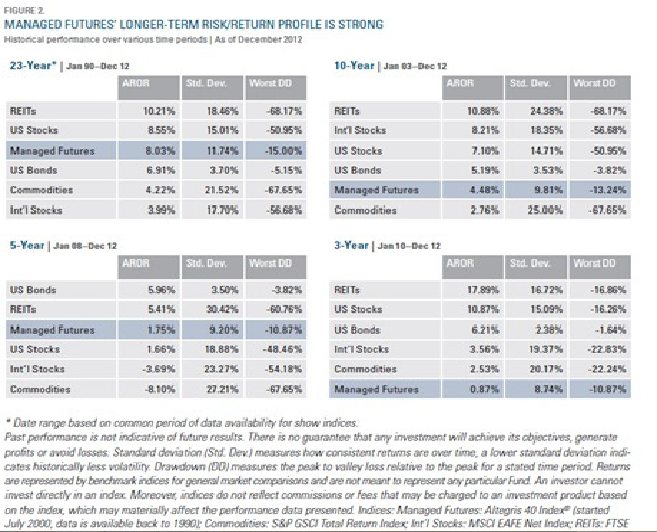

Asset classes are, by their very definition, cyclical to varying degrees. So it is with managed futures-with the caveat that historical underperformance for the strategy has been: 1) infrequent and 2) relatively lower when compared to traditional long-only asset classes. In fact, while past performance is no guarantee of future results, a key aspect of managed futures' long-term profile is its track record of generating profits through a wide array of market cycles. To that end, managed futures have experienced positive returns in 19 out of the last 23 years. Delving further into these numbers, we see in Figure 2 a illustration of the extent to which managed futures have lagged the other major market indices over the last three calendar years on an annual return basis. However, over a longer timeframe, managed futures' performance ranks much higher-slightly trailing US stocks, and beating out US bonds, commodities and international stocks since January 1990. In addition, the table below shows that, even during the last three years, managed futures generated the second-lowest standard deviation and worst drawdown, respectively, compared to the other major asset classes-which is consistent with managed futures' compelling risk profile over longer timeframes as well. We believe that the unique risk/return characteristics of managed futures investing are revealed in this broader historical context, and that the key long-term role that the strategy can play in a diversified portfolio is reaffirmed.

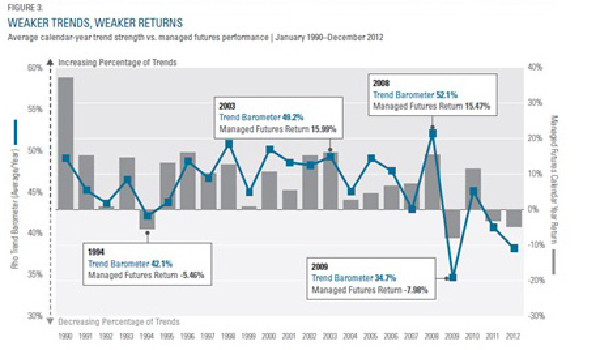

A Leading Role For Trend FollowingWe view managed futures through the lens of the Altegris 40 Index��, which monitors the performance of the 40 leading managed futures programs based on month-end equity as tracked by Altegris (net of the manager's fees, typically both management andincentive fees).1 Trend followers typically comprise 75% of the Index, while specialized managers make up the remainder. As this breakdown implies, managed futures have historically been dominated by trend following managers, whose performance- as their name suggests-is largely driven by capitalizing on trends as they develop. David Harding, Founder and President of Winton Capital Management, has been successfully pursuing a trend following strategy for 25 years. He describes the efficacy of the approach by explaining that "when a market is going up, for example, it's slightly more likely to carry on going up, rather than reverse and go down. And if you correctly invest in those trends over a long enough period of time, across enough markets, you can make money." This has certainly been true for Winton, as well as for many of its trend following peers. Choppy markets and a lack of price trends, however, generally make it difficult for the majority of trend following managed futures managers to deliver strong risk-adjusted returns. And it just so happens that three of the past four years (2009, 2011 and 2012) have featured the three lowest trend-strength readings for a calendar year in history, according to the Rho Trend Barometer. Developed by Rho Asset Management, the Rho Trend Barometer measures the percentage of markets with medium to strong trends.2 Just as a thermometer reading of 32 degrees Fahrenheit equates to freezing, when the Trend Barometer reads a value that is less than 43.3%, market trendiness begins to get "colder" or weaken. Likewise, when the Trend Barometer gets "hotter"-that is, moves above 43.3%-the more markets are trending. Trend following is a core managed futures strategy that generally seeks to profit from the continuation of medium to long-term directional price moves in a market. Specialized trading programs generally seek to capitalize on short-term market fluctuations, often using trend or counter-trend strategies with a shorter time horizon. For example, being positioned long after market prices have moved higher for a period of time or positioned short after prices have moved lower for a period of time. As a result of this analysis, illustrated in Figure 3 found that four of the five calendar years with a Trend Barometer value of less than 43.3% also- not surprisingly-saw negative performance for managed futures. 1 ) Altegris calculates the dollar-weighted average performance of those 40 managed futures programs for the monthly Altegris 40 Index performance. 2 )Please see www.rhoam.ch for more information about Rho Asset Management.

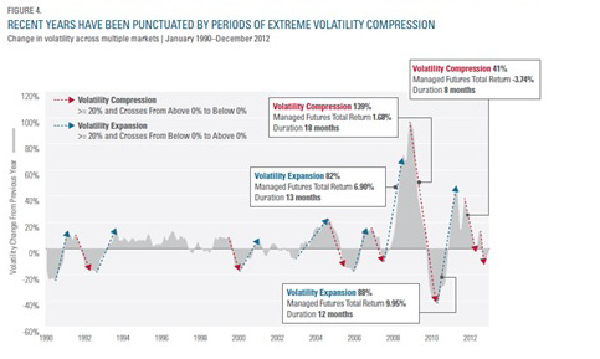

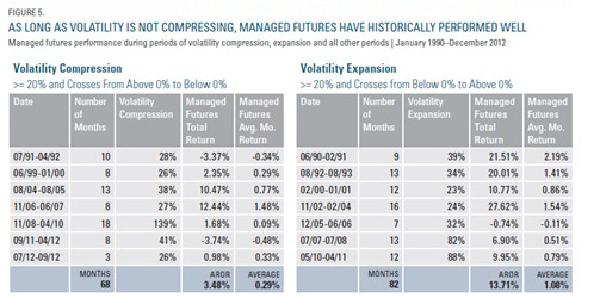

Digging deeper into the numbers, we found that 2009, 2011 and 2012 all witnessed unprecedented levels of non-trending months. Each year featured nine months in which the Trend Barometer value was less than 43.3%. In contrast, 2008 and 2003 had just six months apiece in which the Trend Barometer value was less 43.3%-not to mention, four months in each year in which the Trend Barometer value was above 60%, with corresponding returns for managed futures of 15.47% and 15.99% for the two years, respectively. However, it's also important to note that not every market needs to trend for trend followers to be successful. Indeed, the chart shows us that the best-performing years for managed futures have historically been when the Trend Barometer value is around 50%-meaning that just half of the markets had medium to strong trends on average during those years. The emergence of just a few sustainable trending markets, then, allows managers to build greater positions as trends further strengthen. Looking Forward: When Will the Trend Again Be our Friend?Certainly, the recent performance of trend following managers must be judged in the context of conditions ranking among the most unfriendly in history for these strategies. To say the markets have lacked enduring trends would be an understatement-they have been, according to Winton in a recent letter to investors, "mean / reverting more than at any point in the past 20 years."The good news is that all prior periods of exceptionally trendless markets have been short-lived. Many were followed by conditions punctuated by more durable trends-and the latter period of 2012 brought signs that such a transition might be in store. Accordingly, we believe that trends could very well move off their historic lows as measured by the Trend Barometer and begin to strengthen. Consequently, medium-and longer-term trend followers should be able to take advantage of more sustainable trends that could emerge. This scenario becomes particularly important if markets start to trend downward, as trend followers (and managed futures managers in general) can profit from falling markets just as easily as rising markets. At the same time, not all managed futures managers are trend followers-a significant subset are specialized managers, pursuing a wide variety of trading approaches, including discretionary macro, short-term systematic, countertrend and other strategies. Interestingly, six of the 10 short-term systematic managers in the Altegris 40 generated positive returns in 2012. In marked contrast, only two trend following managers were up on the year. In fact, the only managers in 2012 that returned double-digit positive returns for the calendar year were two specialized managers-thus highlighting the importance of exposure to a diverse blend of elite managers as part of an investor's total allocation to managed futures at all times, particularly during trendless or choppy markets. The Mixed Blessing of Low VolatilityUnlike traditional long-only investments, managed futures typically perform well in environments in which volatility is expanding. In fact, high volatility can be quite friendly to managed futures managers.Svante Bergstr��m, Founding Partner and Portfolio Manager at Lynx Asset Management, describes the ideal conditions for trend following managers: "When you have high volatility and stocks are falling, that tends to create trends not only in stocks, but also in fixed income and currencies and commodities at the same time. So that's normally when you see us perform best." Such was the case in 2008, a positive environment for managed futures in which the strategy returned 15.47%, while US stocks were down -37%. Conversely, as volatility across markets starts to diminish or compress, managed futures managers usually find a more challenging environment-as they have in recent years. While current levels of volatility are not out of the ordinary compared to other periods over the past 20-plus years, the range and length of time in which volatility has compressed over the past two years is only comparable to that seen in 2009, when managed futures delivered negative returns of nearly -8%. "Periods of compressing volatility have proven to be the only times in which managed futures have consistently underperformed."Looking at stretches of time with neither volatility expansion nor compression, however, reveals an interesting discovery: intervals of essentially flat volatility have generally been positive for managed futures as well. In fact, periods of compressing volatility have proven to be the only times in which managed futures have consistently underperformed. Figure 4 depicts historical volatility3 change from the previous year, as represented by the gray shaded area. An increase (volatility expansion) or decrease (volatility compression) simply means that volatility for a particular time period is greater or less than an earlier time period. Extreme periods of volatility compression (indicated by the red arrows) are when the volatility changes are greater than or equal to 20% and move from above zero (positive) to below (negative). Likewise, extreme periods of volatility expansion (the blue arrows) are when the volatility changes are greater than or equal to 20% and move from below zero (negative) to above (positive). 3) Defined by the aggregate standard deviation of 38 markets. Standard deviation is a statistical measure of how a consistent set of data are over time; a lower standard deviation indicates historically less volatility.

Clearly, there have been far more pronounced periods of volatility compression in recent years. As detailed in Figure 5, the level of volatility dropped a whopping 139% over 18 months beginning in November 2008, while the eight-month period beginning in September 2011 saw a drop of 41%. The significance: During times when volatility is compressing, managed futures have historically not performed well. For example, during these two recent periods of extreme compression, managed futures delivered total returns of 1.68% and -3.74%, respectively.

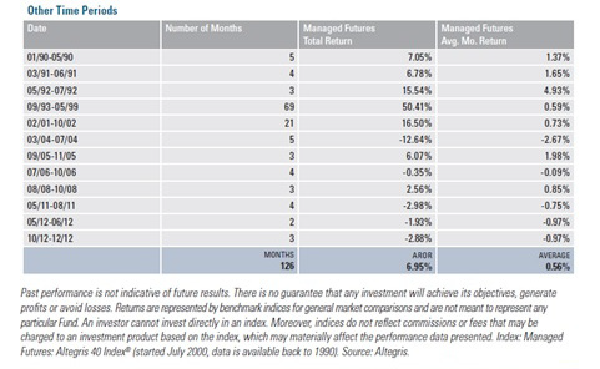

At the same time, the chart highlights managed futures' equally prominent track record of positive performance during periods of rapidly expanding volatility. For instance, managed futures delivered total returns of 6.90% and 9.95% during the two largest volatility expansion periods of the last 23 years-more than offsetting the underperformance during the most extreme compressions. In fact, as Figure 5 reveals: Managed futures during all periods of extreme volatility expansion delivered an annualized return of 13.71%, compared to 3.48% for periods of extreme compression. Further, we see that even during periods of flat volatility since 1990, managed futures still did quite well, generating an annualized return of almost 7%. Indeed, performance for the strategy was solid to spectacular across short, medium and extended periods of flat volatility-15.5% during a three-month period in 1992, or example; 16.5% for the 21 months from February 2001 to October 2002; and 50.4% for the 69 months from September 1993 to May 1999. In short: While managed futures historically under-performed during periods of extreme compression, they generally performed well amid flat volatility or really well during heightened volatility expansion. Looking Forward: When Will Volatility Compression end?Volatility expansion or compression over the past few years has been �€œamplified" compared to the previous 20-plus years. While markets could continue to experience diminishing volatility, we believe it is more likely that they will start to see an expansion, given the recent historically low volatility levels. Such a shift would, of course, augur well for managed futures managers, particularly those pursuing trend following strategies. But a shift to volatility expansion would not be the only possible catalyst for improved managed futures performance. As long as volatility simply stops compressing, the environment should be more favorable for managed futures. This is a partial excerpt of the white paper. To view the entire report follow this link |

|

This article was published in Opalesque Futures Intelligence.

|

{kind=link}