RSS

RSS|

Keith Campbell has guided his firm - and

the managed futures industry - through significant growth. Will Andrews took the helm in the Fall of 2012 as CEO having spent the last 16 years in research and research operations, most recently Co-Director of Research before his current role.� Newly promoted to President, Mike Harris was most recently Director of Trading and is in his 13th year at Campbell.� Will and Mike are supported by an Executive Team with a tenure at Campbell ranging from 6-20 years at the firm.�� Keith Campbell commented, "Will and Mike have 29 years of collective Campbell experience.� Their ability to guide our corporate culture and adapt with vision and foresight are without question.� Campbell has never been managed by one key person which is why we have been successful for over 40 years.� Our systematic discipline allows us to function and collaborate across many people who bring unique skills to our process."

With a background in research, Will

Andrews was promoted to CEO. What is interesting about this statement is the reference to the systematic nature of the trading strategy being passed on.� Unlike a discretionary strategy, which is dependent on the individual alpha of the trading manager, a systematic strategy is typically developed and managed by a team of people.� The strategy is mathematically based and a systematic approach to trade management is more easily transferred from one generation to the next than is a discretionary strategy. The History of a Maturing Algorithm Campbell & Company began trading a momentum / trend strategy in 1972, making it among the most seasoned Commodity Trading Advisors still operating.� Many early managed futures programs were known as "Turtles," following a specific discipline of trend following that utilized a basic moving average cross method to determine when to enter and exit a trade.� Although Campbell was founded in 1972 and began as a classic trend follower, don't confuse it with any of the famous "Turtles" who are considered trend following founders.� The Campbell quantitative strategy has matured through a research department of nearly 30 pure researchers generating alpha using hypothesis-driven, scientific research.� This team is supported by additional employees in research operations and trading, all touching the investment process of Campbell's multi-model, multi-time horizon, multi-asset class approach.�� It is out of this research department that the new leader for the firm has emerged.

Mike Harris, former Director of Trading,

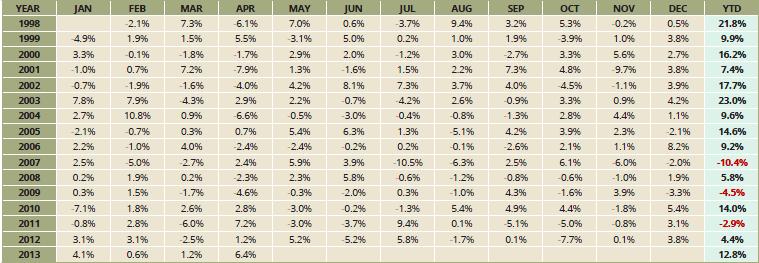

is Campbell's President. Speaking of the new leadership taking over his namesake firm, Mr. Campbell stressed the importance of understanding the quantitative models.� "Will Andrews grew up in the research department at Campbell starting as an assistant to the Director of Research in 1997," he said.� "Will understands the model development process from start to finish, including the technology, data, and control environment necessary to have a sustainable process.� I cannot think of anyone better suited to guide Campbell in all aspects of our business going forward.� We are first and foremost, committed to competing at the highest level in risk adjusted returns.� We have been in business a long time, but we have a young spirit at the firm." In addition to the core trend following strategies, Campbell was one of the first managers to develop systematic strategies in currency carry and other forms of non trend following strategies, starting in the late 90s.� Since then, Campbell has used its sector specific expertise to develop strategies that exploit the term structure in commodities and fixed income, as well as strategies that use cross-sector information from other markets such equities and derivatives of futures price information.� Most recently, Campbell has focused on developing strategies that fall in the shorter time horizon (less than one week).� These strategies, according to Campbell, are very complementary to the overall portfolio. Campbell by the Numbers Campbell's risk management policies have evolved with the inclusion of more and more models that have low correlation to each other.� Overtime, they have adopted a risk targeting approach that delivers a realized annual standard deviation of 13-15% and a margin to equity ranging from 10-15% on average, according to the firm. Outlook Going Forward Campbell believes they are in a sweet spot of assets under management from $3 billion to $10 billion.� At $3 billion they have an institutional quality infrastructure and the capacity to develop strategies that allow them to keep a footprint in many commodity markets and maintain a reasonable allocation to shorter time horizon strategies.� Campbell continues to adapt and innovate by committing to research talent combining disciplines from finance and economics with mathematicians and scientists from prestigious universities around the world.� "We are committed to competing at the highest level in risk adjusted return, to maintaining a strong control environment in all aspects of our business including compliance with regulatory changes," Mr. Andrews said. Opinion/Analysis of Campbell PerformancePERFORMANCE AS OF APRIL 30, 2013

Risk Disclosure: Past performance is not indicative of future results. Performance Sources: Campbell & Company. Information sources believed reliable but no warrantee is being made relative to same. By Mark Melin Trend followers have several interesting statistical points to consider.� Among them is win percentage.� This isn't because win percentage is necessarily a good measure of trend following performance - it's not. Win percentage might be best used as a caution flag.� In win percentage I look for a range from 52% to 57%.� Anything north of 60% starts to raise suspicion.� In part this is because the historical numbers lead me to believe the number of ideal beta market environments of price persistence might not lend itself to the strategy having a high win percentage.� Contrast this with win percentage in a short volatility (my target is north of 70%) or discretionary strategy (my target is north of 60%).� These strategies might be expected to display a very different profile than a trend strategy (where my real target is 54% with cause for further investigation rising with questions regarding story plausibility.)� �Campbell is at the target regarding win percentage, but perhaps most important to consider in trend following is the downside risk management. In trend following perhaps the more significant issue is found in size of win relative to loss.� A related key metric to consider is the extent of upside deviation to downside deviation. �Here's why these two statistics are key to consider in trend following. While early algorithms were nothing more than a simple moving average cross trend following method, many trend following formulas adjust risk differently based on upside deviation / profit relative to downside deviation / loss.� Once a winning trade is established certain systems, it is said, loosen risk controls for the upside and tighten risk on the downside.� The trader's concept of "letting the winners run but cutting the losers." The variation between win and loss size speaks to risk controls while upside vs downside deviation is related but speaks more to volatility control.� With Campbell, they have an average loss size close to 1% lower than my benchmark, but their differential between upside and downside deviation is much tighter than the spread their win size / loss size.� These might provide a window to benchmark a robust risk management regime.� You can use this in the conversation with the CTA.� If one were to see high upside deviation but lower downside deviation, an interesting next question might be "Do you use portfolio position scaling to exit positions or is it an all in / all out method?" Anecdotally one might expect the portfolio position scaling to have a wider spread between upside and downside deviation numbers if they recognize the difference in risk between upside and downside deviation.

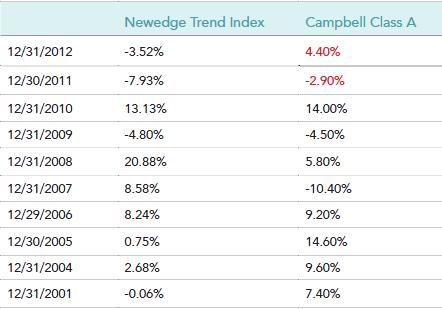

Risk Disclosure: Past performance is not indicative of future results. Performance Sources: Campbell & Company. Newedge Trend Index performance source Information sources believed reliable but no warrantee is being made relative to same. Personal Note / Observations / Opinions: I had coffee with Will and two of his associates about a month ago in New York. He was questioned about the algorithmic changes, something that had been rumored to have been actively underway 2 years ago when performance began to correlate less and less with the Newedge Trend Index.� In particular the question at the top of my mind: did they add a relative value strategy or volatility strategy to the trend following staple?� Or did they stay true to their trend following roots? He was coy about the relative value question, but said they were using "term structure" in trades, which typically is verbiage used to indicate relative value of some sort was at play.� I would suspect Will might have an eye on new developments in research and development going forward. While the numbers behind Campbell are interesting - and we only investigated a few of many considerations in this article - perhaps most significant is their operational due diligence considerations, including a significant back office, research and risk management team in place. When you understand Campbell's business emergence, it is a classic tale of the business of a trading program growing through the emerging, evolving and maturing stages of CTA development. (RPM Asset Management has conducted extensive studies in this regard.)� From a business infrastructure standpoint, there are many interesting business challenges that all CTAs encounter resulting from rapid growth.� The managed futures industry spiked in growth leading up to 2008 and then dramatically accelerated to become the top hedge fund sub category.�� 2008 was a time of assets under management growth for Campbell.� But what is really interesting is the lack of correlation one could see after 2010.� My speculation is that is the point significant changes were made to the algorithm, just judging on performance. (Campbell neither confirmed nor denied this speculation.)� Could this point to the rejuvenation phase of the CTA's development?� Can Campbell's trend following algorithms catch the price persistence of future volatility?� This is an "unknowable?" �From a performance standpoint, the question is what happens if price persistence enters the market place on a short and mid-term level?� How will it perform relative to the benchmark Newedge Trend Index?� When the beta market environment of price persistence is in place one might expect this to be an optimal environment for this CTA to operate in, which is among several issues to consider in managing this investment on a going forward basis. |

From June 2009 through present, the assets in the Fund were considered to be proprietary as fifty percent or more of the beneficial interest was owned or controlled by the Trading Advisor and its affiliates.

From June 2009 through present, the assets in the Fund were considered to be proprietary as fifty percent or more of the beneficial interest was owned or controlled by the Trading Advisor and its affiliates.

|

This article was published in Opalesque Futures Intelligence.

|

{kind=link}