RSS

RSS|

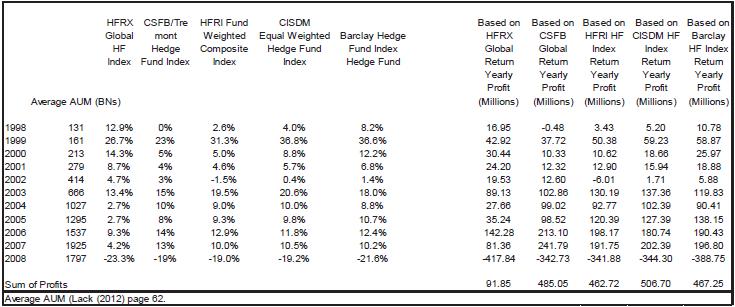

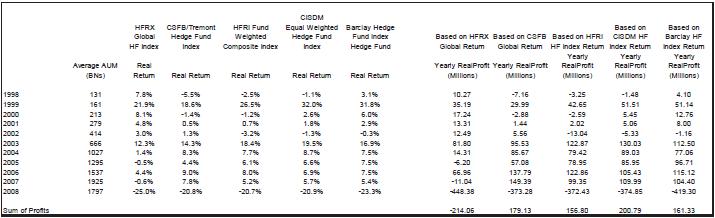

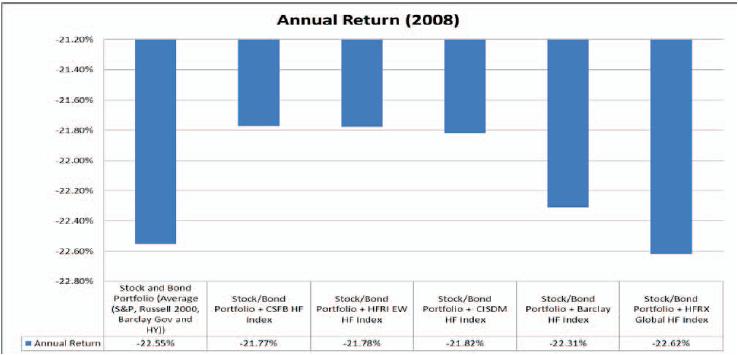

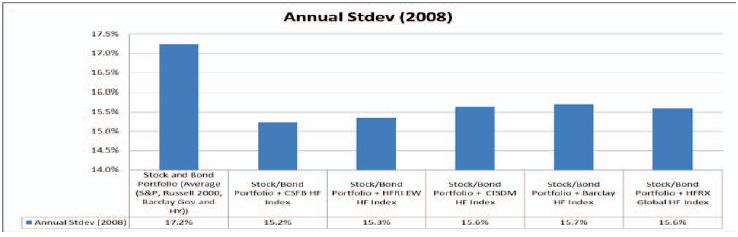

2008 As a Special Year Lack spends considerable time focusing on 2008 as an example of the hedge fund market negatively impacting investor returns even to the extentof asserting that "In fact, in 2008 the hedge fund industry lost more money than all the profits it had generated during the prior 10 years. (italics his) Although it is not possible to calculate precisely, it is likely that hedge funds in 2008 lost all the profits every made. By the end of 2008, the cumulative results of all the hedge fund investing that had gone before were negative. By the end of 2008, the accumulative results of all the hedge fund investing that had gone before were negative(page 12)." A wonderful story if true, but the story is not true. In fact, for all the traditional hedge fund indices (when considering AUM) the losses in 2008 did not dominate the past profitable years.As shown in Exhibit 5a, if one merely compares investor profits over the period 1998-2007 with the large loss in 2008, the investors' net profit still would have been positive for all the reported indices. The results in Exhibit 5a are reported in nominal terms. In Exhibit 5b, the results are also positive (with the exception of HFRX Global) in real terms (after adjusting for the risk free rate as done by Lack).11 Even for 2008 as a stand-alone year, as shown in Exhibit 6a, for every hedge fund index with the exception of the HFRX Global Index, the addition of hedge funds to the equal weight stock and bond portfolio would have increased return and as shown in Exhibit 6b, for every hedge fund index including the HFRX Global Index the addition of hedge funds to the equal weight stock and bond portfolio would have reduced risk. While it is possible to find an asset portfolio dominated by risk free government bonds for which the addition of hedge funds in 2008 would have resulted in ex post increased risk and decreased return. This is an ex post fact. The addition of many risky assets to a risk free portfolio in 2008 would have increased risk and reduced return including equities, real estate, commodities, and risky debt. As mentioned earlier investment portfolios should be considered ex ante and the relative weights of various assets based on the expected risk environment. In fact, given the relatively low correlation of hedge funds to other risky assets and low volatility of hedge funds if one believed 2008 to be a potentially risk environment, an investor who has a portfolio with a reasonable level of risk exposure could have benefited (as shown in Exhibits6a and 6b) from the inclusion of hedge funds. Exhibit 5a: Profits from Hedge Fund Investment

Exhibit 5b: Profits from Hedge Fund Investment

Exhibit 6a: 2008Annual Return and Std Dev. of Stock/Bond/ HF and Stock/Bond Portfolios

Exhibit 6b: 2008 Annualized Std Dev. of Stock/Bond/ HF and Stock/Bond Portfolios

Indices as Representative of Investor Return As discussed previously, the use of any hedge fund index in any analysis must be done with care. Lack mentions that poorly performing managers may not report and thus an equal weighted index may overestimate returns (of course he fails to mention that over performing managers that are closed may also not report so in fact the net final results are unknown). Lack also mentions (Page 60) that there is plenty of academic research on the excess return impact of certain hedge fund indices due to their use of backfill bias (e.g. many databases fill in the old returns of managers when they are start reporting to databases and drop from their databases managers who no longer report. To the degree that the newly reporting managers' historic returns are better than the managers historic returns who are leaving, the historical returns of the new database will be above that of the prior database). He then mentions prior research to support that "actual returns experienced by investors are probably lower than the reported (3 to 5 percent) by this amount" Lack goes on to state that "none of the indices referred to in this book have been modified to reflect survivor bias or backfill bias so overstatement of returns in those indices remains" (page 60). It is critical to note that the primary hedge fund indices (HFR, Barclay, CSFB, CISDM) simply report the returns of reporting managers (some with restrictions). This does NOT apply to HFRX, which is created after a number of filters or restrictions are applied to select a small group of managers. The hedge fund indices (HFR, Barclay, CSFB, CISDM) may have some selection bias (not all managers report to all databases) but no - I repeat no backfill bias and no survivor bias. When managers leave the database or are added to the database no adjustments are made to the historic returns of the hedge fund indices. There may be backfill or survivor bias in the current database but not in the historically reported hedge fund index returns. Similar to the S&P 500, as new firms come and go to the database from which the S&P 500 firms are selected the historical return of the index does not change. Once a firm's return is included in the S&P 500 it's return never leaves that index - if a firm is dropped from the S&P 500 due to poor performance, its old returns are not dropped from the historic S&P 500 and the S&P 500 index is not revised. Only for a new database for which a historical index is newly created from that database does an index have backfill bias. Lack may wish to adjust the HFRX for backfill bias (although as noted in footnote 11 since the HFRX index is not based on all reporting managers to a hedge fund database the reason for this adjustment not clear), for the reported returns for the other indices (HFR, CISDM, Barclay, CSFB) used in this analysis there is no basis for a backfill or survivor bias adjustment. Simply up, since there is no basis for backfill or survivor bias adjustment for the major hedge fund indices, there is no overstatement of returns in those hedge fund indices due to backfill or survivor bias. Manager Fees and Fund Performance Lack attempts to place one of the major concerns as to his assertion of poor average investor performance to the fees of hedge fund managers. As discussed earlier, one should be reminded that one should not compare hedge fund managers' gross profits with investor net profits. Simply put, manager gross profits do not reflect managers' net profits. One should not have to be reminded that the gross fees paid to managers does not equal net profits to them. Hedge fund managers have to pay salaries, operational costs, service costs, travel.... out of gross profits. That is one of the reasons why small hedge fund managers (e.g. $100,000,000) can hardly exist on the current 1% and 20% unless they receive incentive fees (many small hedge funds cannot be run on gross profits from fees on assets alone). In brief, a more extensive analysis and not one based on hedge fund gross profit is required to determine if hedge fund net profit can be regarded as exorbitant relative to the net return to the investor.12 Future of Hedge Funds Any analysis of past hedge fund data requires an assumption as to the relationship between past and current factors impacting the risk and return characteristics of the investment strategy. Today's hedge fund index return does not have the return and risk characteristics of the returns of a hedge fund index of 5 or 10 years ago. Over time, old strategies will change and new ones will evolve that offer new opportunities. The use of any one strategy lies not in examining years of past data. It tells one little if anything as to the future of that strategy, unless the underlying characteristics of that strategy remain constant. The future expected returns and risk of a strategy depends on the structure of the strategy and the assets it is expected to hold under current and future expected economic conditions. That having been said, the analysis of past data provides enough evidence of the historical benefit of certain hedge fund strategies as well as periods in which certain hedge fund strategies may offer benefit to certain investors. The bottom line is that in most historical periods, hedge funds have offered historical evidence of the benefits of hedge funds for the average investor. As to the future, the simple fact is that hedge fund industry asset strategies, which are not constrained to match an existing long only defined investment benchmarks, at least offer the possibility of returns in market conditions which are not favorable to that long only investment benchmark. That should be enough for investors. Selected References Acar, E. and S. Satchell. Advanced Trading Rules. Oxford: Butterworth-Heinemann, (1998). Agarwal, V. and N. Y. Naik."Risks and Portfolio Decisions Involving Hedge Funds." Review of Financial Studies, 17(1), (2004), pp. 63-98. Agarwal, V. and N.Y. Naik."Generalized Style Analysis of Hedge Funds."Journal of Asset Management, Vol 1. No. 1 (2000), pp. 93-109. Aggarwal, Rajesh K. and Philippe Jorion."The Performance of Emerging Hedge Fundsand Managers."Journal of Financial Economics, 96: 2010a, pp. 238-256. Aggarwal Rajesh K. and Philippe Jorion."Hidden Survivorship Bias in Hedge Fund Returns." Financial Analysts Journal (March/April, 2010), pp. 69-74. Aggarwal, Rajesh K., J. Buchan, and P. Saint-Laurent."Three Myths about Hedge Fund Governance." (JAI, Forthcoming, 2012). Amenc, N. and D. Schroder."The Pros and Cons of Passive Hedge Fund Replication." EDHEC Risk and Asset Management Research Center, (October 2008). Aragon, George and Spencer Martin. "A Unique View of Hedge Fund Derivatives Usage: Safeguard or Speculation?"Working Paper.Carnegie Mellon University, (2009). Bodi, Z., A. Kane, and A. Marcus.Investments, (McGraw-Hill, 2010). Brown, S. J., W. N. Goetzmann and R. G. Ibottson. "Offshore Hedge Funds: Survival and Performance, 1989-95." Journal of Business, 72 (1) (1999), pp. 91-117. Brown, S. J., and W. N. Goetzmann."Hedge Funds with Style." The Journal of Portfolio Management, (Winter 2003), Vol. 29, No. 2: pp. 101-112. Capocci, D. and G. Huber."Analysis of Hedge Fund Performance." Journal of Empirical Finance, 11 (2002), pp. 55-59. Crowder, G., H. Kazemi, and T. Schneeweis. "Asset Class and Strategy Based Tracking Approaches." Journal of Alternative Investments (Winter 2011). Dichev, I. D. and G.Yu. "Higher risk, lower returns: What hedge funds investors really earn." The Journal of Financial Economics, 100 (2011), pp. 248-263. Dietiker, Oliver. "On the Consistency of Hedge Fund Indices Across Providers." (August, 2009) ssrn.com/abstract=1458013. Dor, A., R. Jagannathan, and I. Meier."Understanding Mutual Fund and Hedge Fund Styles Using Return-Based Style Analysis."JOIMVol 1.no. 1 (2003), pp. 94-134. Fama, E. and K.R. French."Common Risk Factors in the Returns on Stocks and Bonds." Journal of Financial Economics, 33 (1993), pp. 3-56. Ferson, Wayne and Kenneth Khang. "Conditional Performance Measurement Using Portfolio Weights: Evidence for Pension Funds." NBER Working Papers 8790, (2002). Ferson, W. E. and C. R. Harvey."Conditioning Variables and the Cross Section of Stock Returns." Journal of Finance, 54 (1999), pp. 325-1360. French, K. Momentum Factors. Web Page, (2010). Fung, W. and D. A. Hsieh. "Empirical Characteristics of Dynamic Trading Strategies: The Case of Hedge Funds." Review of Financial Studies, 10, (1997), pp. 275-302. Fung, W. and D. A. Hsieh."Asset-Based Style Factors for Hedge Funds."Financial Analyst Journal (September/October, 2002), pp.16-27. Fung, W. and D. A. Hsieh. "Hedge Funds: An Industry in Its Adolescence." Federal Reserve Bank of Atlanta Review, (4th Quarter, 2006). Fung, W. and D. A. Hsieh. "Measurement Biases in Hedge Fund Performance Data: An Update." Financial Analyst Journal, Vol 65. No. 3, (2009), pp. 36-38. Fung, W., D. Hsieh, N. Naik, and T. Ramadorai. "Hedge Funds: Performance, Risk and Capital Formation." Journal of Finance, 63, (2008), pp.1777-1803. Fung, W. D.and D.A. Hsieh. "The Risk in Hedge Fund Strategies: Theory and Evidence from Trend Followers." Review of Financial Studies 14 (2001), pp. 313-341. Griffin, J. and J. Xu. "How smart are the smart guys? A unique view from hedge fund stock holdings." The Review of Financial Studies, 22, (2009), pp. 2531-2570. Gupta, B., E. Szado and W. Spurgin."Performance Characteristics of Hedge Fund Replication Programs." The Journal of Alternative Investments, (Fall 2008), pp. 61-68. Hasanhodzic, J. and A. Lo. "Can Hedge-Fund Returns Be Replicated?: The Linear Case." Journal of Investment Management, Vol. 5, No. 2, (Second Quarter 2007). Jaeger, L. and C. Wagner. "Factor Modeling and Benchmarking of Hedge Funds: Can Passive Investments in Hedge Fund Strategies Deliver?" The Journal of Alternative Investments, (Winter 2005), pp. 9-36. Jagannathan, Ravi, and Zhenyu Wang."The conditional CAPM and the cross-section ofexpected returns." Journal of Finance, 51, (1996), pp. 3-53. Jegadeesh, Narasimhan and Sheridan Titman. "Profitability of momentum strategies: an evaluation of alternative explanations." Journal of Finance, 56, (2001), pp. 699-720. Karavas, V., H. Kazemi and T. Schneeweis. "Eurex Deriva��tive Products in Alternative Investments: The Case for Hedge Funds." European Exchange (EUREX), (2003). Kat, H. and J. Palaro."Who Needs Hedge Funds?A Copula-Based Approach to Hedge Fund Return Replication."Alternative Investment Research Centre.Case Business School, Working Paper #27. (November 2005). Kat, H. and J. Palaro. "Tell Me What You Want, What You Really, Really Want! An Exercise in Tailor-Made Synthetic Fund Creation."Alternative Investment Research Centre.Case Business School, Working Paper #36.(November 2006a). Kat, H. and J. Palaro."Hedge Fund Indexation the Fund Creator Way."Alternative Investment Research Centre.Case Business School, Working Paper #38.(November 2006b). Kazemi, H., Y. Li and T. Schneeweis."Conditional Performance of Hedge Funds."CISDM Working Paper, (2008). Kazemi, H., E. Szado and T. Schneeweis. "The Use of IRR in Hedge Fund Analysis: Buyer Beware," INGARM, (2012). Kazemi H. and T. Schneeweis."Conditional Performance of Hedge Funds."CISDM Working Paper, (2004). Kazemi, H. and T. Schneeweis. "The Use of ETFs in Hedge Fund Replication: Case Examples." INGARM Working Paper, (2010). Lack, S. Hedge Fund Mirage (John Wiley, 2012). Lo., Andrew. "The Dynamics of the Hedge Fund Industry."The Research Foundation of the CFA, (2005). Malkiel, Burton and A. Saha. "Hedge Funds: Risk and Return." (Working Paper, 2004). Malkiel, Burton and A. Saha. "Hedge Funds: Risk and Return." Financial Analyst Journal (November/December, 2005), pp. 80-88. Naik, N., T. Ramadorai and M. Stromqvist."Capacity Constraints and Hedge Fund Strategy Returns." European Financial Management, 13 (2007), pp. 239-256. Schneeweis, T., "Dealing with the Myths of Hedge Fund Investment." The Journal of Alternative Investments Winter 1998, Vol. 1, No. 3: pp. 11-15. Schneeweis, T., "Dealing with the Myths of Managed Futures." The Journal of Alternative Investments Summer 1998, Vol. 1, No. 1: pp. 9-17. Schneeweis, T. "Where Academics/Practitioners Get It Wrong: An Open Letter," INGARM, 2012. Schneeweis, T. The Myths of Hedge Funds. INGARM, (2010). Schneeweis, T. The Benefits of Hedge Funds. INGARM, (2010). Schneeweis, T. and H. Kazemi. "Factor Versus Trading Style Based Return Estimates." CISDM Working Paper (2006). Schneeweis, T. and R. Spurgin."Benchmark Determination for Managed Futures."CISDM Working Paper (1997). Schneeweis, T. and R. Spurgin."A Comparison of Return Patterns in Traditional and Alternative Investments." in SohailJaffer ed. Alternative Investment Strategies (Euromoney, 1998), pp.157-188. Schneeweis, T. and R. Spurgin."Multi-Factor Analysis of Managed Futures, Hedge Funds, and Mutual Funds.Return and Risk Characteristics."The Journal of Alternative Investments (Fall 1998), pp.1-24. Schneeweis, T., H. Kazemi and G. Martin. "Understanding Hedge Fund Performance: Research Issues Revisited - Part I." The Journal of Alternative Investments, 5, (2002), pp. 6-22. Schneeweis, T., H. Kazemi and G. Martin. "Understanding Hedge Fund Performance: Research Issues Revisited - Part II." The Journal of Alternative Investments, 7, (Spring 2003), pp. 8-30. Schneeweis, T., R. Spurgin and H. Kazemi. "Eurex Derivative Products inAlternative Investments: The Case for Managed Futures." CISDM Research Report, (2003). Schneeweis, T., H. Kazemi and G. Martin," The Impact of Size on Hedge Fund Performance," INGARM, 2003. Schneeweis, T., R. Spurgin, and V. Karavas, "Eurex Derivative Products in Alternative Investments: The Case for Hedge Funds." CISDM Working Paper, (2003). Schneeweis, T., G. Crowder, and H. Kazemi.The New Science of Asset Allocation.(John Wiley, 2010). Schneeweis, T. and E. Szado. "Madoff: A Return Based Analysis." The Journal of Alternative Investments, (Spring 2010), Vol. 12, No. 4: pp. 7-19. Schneeweis, T., H. Kazemi and E. Szado. "Hedge Fund Database "Deconstruction": Are Hedge Fund Databases Half Full or Half Empty?" The Journal of Alternative Investments, (Fall 2011), Vol. 14, No. 2: pp. 65-88. Schneeweis, T., E. Szado and H. Kazemi. "Hedge Fund Return-Based Style Estimation Models: A Review on Comparison Hedge Fund Indices." The Journal of Alternative Investments (Fall 2012), Vol. 15.No. 2, pp. 24-53. This is the final installment of a two part article. To receive the full white paper on the topic, e-mail melin@opalesque.com Thomas Schneeweis Ph.D. is the Michael and Cheryl Philipp Professor of Finance and Director of the Center for International Securities and Derivatives Markets at the Isenberg School of Management, University of Massachusetts-Amherst. He is the Founding and current EditorofThe Journal of Alternative Investment. He is also the co-founder of the Chartered Alternative Investment Analyst Association (www.caia.org), the Chartered Alternative Investment Analyst Foundation (foundation.caia.org) and the Institute for Global Asset and Risk Management (www.ingarm.org). He has published more than 100 articles in the area of investment and asset management with his current research focusing on risk based asset management and investment strategy replication. He has presented at major conferences globally, has been quoted in major financial press, and spoken on many financial news programs. He has been credited in part for the creation of asset allocation breakthroughs such as portable alpha and the development of hedge fund replication concepts. He received his Ph.D. from the University of Iowa, M.A. from University of Wisconsin, and a B.A. from St. John's University. His most recent co-authored book publications include The New Science of Asset Allocation (John Wiley and Sons, 2010) and Postmodern Investment (John Wiley and Sons, fall 2012). Professionally, he has more than thirty years experience in investment management. He was associated with the creation and development of the Zurich and Dow Jones Investible Hedge fund Indices, the LMEX and Bache Commodity Indices and acted as Director of Research at Ursa Capital (one of the first managed account based hedge fund platforms). He is currently serves as an out-side trustee on the boards of several large mutual fund families. He helped found Alternative Investment Analytics (a commodity investment firm) and White Bear Partners (a hedge fund/managed futures trading firm). He is currently principal at S Capital Management, LLC (www.scapitalmgmt.com) an investment management firm specializing in asset allocation, risk management and investment strategy replication programs. HosseinKazemi, Ph.D., CFA, is responsible for hedge fund performance analytics and strategy replication. He is a Professor of Finance at the University of Massachusetts and is the Associate Director of the Center for International Securities and Derivatives Markets at the School of Management. He is also a Chartered Financial Analyst and has served as a consultant in the areas of asset allocation and risk management. |

|

This article was published in Opalesque Futures Intelligence.

|

{kind=link}