RSS

RSS|

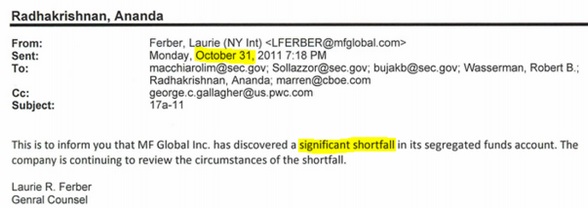

Who Knew What and When Did they Know It. Who Gave a CFTC Lawyer His Marching Orders?By Mark Melin When a regulator orders a brokerage firm not to transfer money, there are typically serious reasons as the rare event. Without direct statements from regulators it is difficult to document exact motivations. But based on publically documented actions and statements, the reason for a regulator’s motivation for engaging in a MF Global fraud investigation seems plausible – given what was known just after the 8th largest bankruptcy in the US occurred. The key point is had a fraud investigation been initiated or even mismanagement been alleged, a receiver would have been appointed and a legal process beneficial to customers would have ensued. The issues start with clear regulatory orders being violated. Who at MF Global Was Given A Direct Order Not to Transfer Money? Based on page 100 of the Trustee’s Investigation Report, October 26, 2011 was the date MF Global was ordered not to transfer customer assets. The notice was given to MF Global executives Laurie Ferber, Chief Legal Counsel; Christine Serwinski, Chief Financial Officer for North America; and Mike Bolan, MF Global (Inc) Assistant Controller. The instructions came from the Designated Self Regulatory Organization (DRSO) CMEGroup. Based on the serious nature of the situation, regulators were attempting to prevent what would become serious damage to the integrity of regulated derivative markets. Had customer assets not been transferred to cover operational expenses, MF Global would likely have been sold to a third party without incident. Note the deficit in customer segregated accounts was http://www.go2managedfutures.com/MF_Global_Giddens_Report.pdf known among CFTC regulators over the weekend, as the deal to sell the firm broke up over this issue. CFTC regulators were documented to have reviewed the segregation reports during the week leading up to the bankruptcy on a daily basis – they were on site presumably trying to protect the public, the false information contained in the report is a key issue. When a shortfall was discovered to reflect contradictory information in the segregation report, this did this triggerred flags for a fraud investigation? Even though MF Global re-submitted revised segregation reports on Sunday, this was well after the damage had been done and funds could not be easily clawed back. CFTC knowledge is further illuminated in Trustee Giddens report in a number of places, including page 118 – 119: “The CME has said that at approximately 2 p.m., a CME representative learned that the CFTC had seen a draft of the segregation statement as of October 28 that showed a deficit.” The report continues. “In the early morning hours of Monday, October 31, the deficit in the segregated funds was confirmed to the CFTC, the CME…” The Giddens report documents Edith O’Brien having discussions with the CFTC over the seg funds shortfall as well as showing active discussion taking place with the CFTC. Thus, the CFTC was aware of these issues well before November 1, 2011. Illegal Asset Transfer While it is important to consider when misleading information was provided to the court on November 1, 2011, so, too, is understanding the nature of the report falsification. As documented on page 139 of the Trustee’s report, on October 28, Mr. Corzine was faced with a decision. He was required to cover an internal margin call of $175 million in London with his only source of funding was customer assets. It is at this moment, a willful decision to transfer customer funds to cover business expenses took place, which violated the law. This was said to be one of the clear focuses of a CMEGroup investigation (see “CMEGroup Independent Investigation Halted” article below). At 40 minutes into the Congressional Testimony, CFTC Commissioner Jill Sommers notes: “Individuals could be liable if they are control persons who has violated the law. “Control persons” generally refers to management. “A willful violation of the CEA is a federal crime and can be prosecuted by a federal attorney,” Commissioner Sommers noted in testimony. In Congressional testimony of August 1, 2012 at 57 minutes, Trustee Giddens notes that while his mandate was not to determine criminal behavior “Our report makes it clear our conclusion that there was knowledge customer segregated funds were improperly moved.” At 1:20 further statements provide context: “My own view is the preponderance of evidence senior management was aware customer funds were being utilized to cover other costs of the firm.” The Falsified Report During the week leading up to the bankruptcy, it stands to reason that unless MF Global hid the illegal transfer of customer assets investigators would have entered into hard investigatory mode during that final week, potentially interrupting additional asset transfers. (Is it odd that the primary suspects involved in the MF Global theft were allowed to operate the firm after the bankruptcy, with ability to further transfer assets?) As outlined on pages 111-113 of the Trustee’s report, after the illegal transfer of customer assets, MF Global employees made a $540 million manual adjustment to the segregation report, hiding the transfer from regulators. This was boldly questioned on page 112 Trustee’s report: “Based on these discussions, an erroneous $540 million manual adjustment was made to the Segregation Statement by personnel in the Financial Regulatory Group, although they did not have backup for the adjustment. The witnesses’ descriptions regarding this matter are confusing and contradictory.” What is Documented That MF Global Regulators Know Going into Court November 1, 2011 The morning of October 31, 2011, the CFTC publically acknowledged they were aware of a significant shortfall in MF Global customer segregated accounts, as CFTC commissioner Jill Sommers documents in Congressional testimony. Segregated funds and the suspicious shortfall had been a hot topic in and around the CFTC all week, as the failure to find a buyer for MF Global was due to this issue. The agency had been in contact with the CMEGroup much of the week discussing the unusual and intricate. This is documented in Trustee Giddens report in several locations. The CFTC’s official knowledge of the MF Global missing money one day before going to court is well documented. As if icing on the cake, regulators received an e-mail from MF Global’s Chief Legal Counsel Laurie Ferber documenting knowledge of the “significant” shortfall on October 31, 2011.

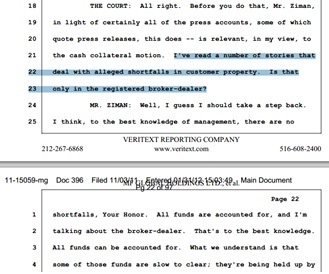

This Matters: What Instructions Were Given to MF Global’s Legal Counsel? The lawyer representing MF Global in bankruptcy court was Kenneth Ziman. It is known Mr. Ziman was in court on instructions from his client, MF Global. Mr. Ziman was hired by MF Global’s Laurie Ferber and no longer represents the client. When Mr. Ziman informed the bankruptcy court in the southern district of New York that MF Global client assets were accounted for, this statement stood in clear contrast to known facts at the time. While Mr. Ziman’s apparent carefully worded testimony included a qualifier that he was referring to the Holdings unit, MF Global is documented to have known much more at the time. The BD and FCM were essentially the same firm (see related articles below). Mr. Ziman issued a “no comment” for this report. The question is: What instructions was Mr. Ziman given? Based on her own e-mails, MF Global’s Chief Legal Counsel Laurie Ferber, said to have hired Mr. Ziman, is on record as confirming knowledge of the shortfall in customer funds the day prior to Mr. Ziman’s court appearance. How Did the CFTC React? A key issue with the CFTC until November 3, 2011 was the lack of action to defend the commodity markets. This first started by Chairman Gensler sleeping while Robert Cook, the SEC’s Division of Trading and Markets and former attorney representing banks, maneuvered to achieve a bankruptcy process that disadvantaged MF Global customers. This can be seen in many locations, such as the CFTC reaction in court. On November 1, 2011. Acting on instructions, a CFTC lawyer from Washington D.C., Martin White, appeared in court on November 1, 2011. Mr. White reports to CFTC General Counsel Dan Berkowitz, who reports directly to Chairman Gensler. When MF Global essentially represented to the court MF Global funds were accounted for, the CFTC’s Mr. White did not object despite the CFTC having in its possession contradictory information. Government lawyers were in court as observers and had rights and obligations to object. Why didn’t he object when the known truth would have benefited MF Global customers and likely protected commodity market integrity? The judge even provided an opening for a CFTC objection, but it did not come. Here is the key: if indications of “fraud, dishonesty, incompetence or gross mismanagement of the affairs of the debtor by current management,” the judge may appoint an examiner or trustee. Why didn’t this happen? Did Mr. White receive instructions from Dan Berkovitz? The information in the CFTC’s possession was of a potentially criminal nature. Mr. White, a sworn officer of the court officially representing an investigatory agency, stood down and the integrity of the segregated account went down as well. It is not known if Mr. White shared any knowledge with the CFTC lawyer from the New York office on the scene, Mr. Stephen Jay Obie. It is unknown if information about criminal behavior was shared with Department of Justice lawyers Ms. Elisabetta Gasparini or Mr. Brian Masumoto who were also in court that day as observers. Also a mystery is if information regarding the falsification of segregated account reports that hid the illegal money transfer made its way to the Securities and Exchange Commission lawyer on the scene, Ms. Patricia Schrage. When contacted, Mr. White did not comment. This Matters: What Were Mr. White’s Instructions from The CFTC? Who Provided Mr. White His Briefing? What Didn’t Gary Gensler Do? The question becomes: what were Mr. White’s instructions from the CFTC? Can we assume that Mr. White knew of the communication to the CFTC by MF Global’s legal chief who hired him? It is documented the CFTC was aware of the information well before Mr. White went to court. If Mr. White were aware of this information did he fail his obligations to the court and in his role at the CFTC? At the time of the MF Global bankruptcy filing on November 1, 2011 did Mr. White believe all customer funds were accounted for? Was Mr. White given any indication of potentially criminal behavior before this date? These same questions could be asked of Chairman Gensler, who had ultimate responsibility as Chairman of the CFTC. What Happened Inside the CFTC? “The information we were getting through official channels was significantly diluted,” said CFTC Commissioner Bart Chilton in an exclusive interview. “We knew customer segregated accounts were violated, and that alone rang alarm bells of the highest magnitude. Based on the limited information available, we were ready to mount a vigorous investigation.” Commissioner Chilton notes the investigation into MF Global is ongoing, although sources have indicated the process is more like an on again, off again affair were justice drifts with the political winds. If the CFTC knew what information was available, they had all the reason in the world to stop the Chapter 11 proceedings of MF Global holdings. They had the power to object and prevent a bankrutpcy structure that was disastrous for the futures customers and the regulated derivatives industry. They did not do it. The question is: Why? Misdirection in Court and Information Known to the CFTCOpinion: By Mark Melin MF Global is a crime scene benchmarked by “chaos” and “confusion.” Consider details of court testimony and peer into misdirection and confusion that is classically outlined in the book Ponzimonum by CFTC Commissioner Bart Chilton. (Behind the scenes, Commissioner Chilton is perhaps best known for his personal choice of hairstyle, a mullet cut. While his detractors exist, the commissioner’s various stands in support of market integrity in the MF Global incident are noteworthy.) This article references a court transcript in which an MF Global legal representative testified to the court with numerous parties watching, including the CFTC. Key Summary: In court an MF Global legal representative was asked where a customer shortfall existed. The MF Global legal representative’s answer to the where question appeared to serve the function of obfuscating known truth by portraying the situation as without criminal suspicion. Misdirected and inaccurate answers essentially communicated to the court that a customer shortfall did not exist, masking what regulators have identified as criminal behavior. CFTC regulators, in possession of contradictory and likely criminal information, did not object when known inaccurate testimony was submitted. According to the US Bankruptcy code, had the court been aware of indications of fraud, dishonesty, incompetence or gross mismanagement of the affairs of the debtor by current management, the judge would be compelled to appoint an examiner or trustee. With a fraud investigation underway MF Global customer rights would have priority and commodity industry segregated account protections would have been defended, as is the mandate of the CFTC. This is because MF Global customer’s transferred property could have been clawed back, with customers retaining their priority rights in the bankruptcy. This is the intent in the design of the Commodity Exchange Act (CEA). Court Documents Detail “The Question” and “The Answer” Information was withheld from the court at a time the transcription shows Judge Glenn was reaching out for information regarding MF Global. For instance, on page 18 in the court transcript, the judge notes the docket from a previous case has not arrived and he further notes the only information available to him at the time was press reports. At this time, shouldn’t a domain expert such as the CFTC be expected to fill in the blanks? Unfortunately for MF Global customers, the accurate information around MF Global was known at the time by the CFTC but not communicated to the court. This leads us to the big moment. On page 21, beginning on line 21, Judge Glen asks a logical question as to WHERE the customer funds shortfall could be found. “I've read a number of stories that deal with alleged shortfalls in customer property. Is that only in the registered broker-dealer?” – Judge Glenn in bankruptcy court, relying on press releases and news reports for information on an unusually complex BD/FCM bankruptcy. What the court did not know at the time is the broker dealer and the FCM were part of the same company. Further, the judge was unaware of what was known by regulators, which indicated mismanagement at best or fraud at worst. In answer to where the customer shortfall existed, the MF Global legal representative said:

Here is the key. Nothing else about the clearing or exchange matters at this point, it is obvious misdirection. The MF Global legal representative was asked where fund shortfalls existed, and they answered that in one division of the overall company there were no funds shortfall. At this point the correct and complete answer to the Judge’s question might have gone something like this: What Was Not Said in Court: To be clear, you are asking “where” the funds were transferred. But first allow me to mention the broker dealer (BD), to which you reference, and the futures commission merchant (FCM), where customer funds shortfall exists, are the same corporate entity. Your honor, this bankruptcy process is complex because it involves both a registered BD and FCM, but we can simplify the issues. Here is all we know as of November 1, 2011: To answer your question, the alleged shortfalls are in the registered FCM division of the combined BD / FCM corporate structure. As the CFTC can attest, here in court today, the FCM experienced a significant customer shortfall under suspicious circumstances with potential mismanagement. At this point we don’t know everything, but what we do know is a classic indication of fraud. The issue is the transfer of MF Global customer assets to cover a margin call on the CEO’s marked-to-the-market trading losses. The week preceding the bankruptcy, MF Global’s chief legal officer is documented to have received orders not to transfer customer assets. After this order was received, customer assets were transferred while the CFTC and CMEGroup were on site at MF Global. Regulators were unaware of this transfer because the reports they relied on from MF Global contained false information. This is the primary information what we know at this point in time, the most important points. Based on this, section 1104 of the Chapter 11 bankruptcy code says the court should be compelled to immediately appoint a Trustee or Examiner when evidence of mismanagement or fraud exists.1 This disclosure of known facts did not happen. As a result, MF Global customers lost priority rights and the core integrity of the commodity markets has been threatened. CFTC Action Required The informational point the CFTC should have contested is when Judge Glen was obviously in need of the wider picture. Why didn’t the CFTC provide input after being given numerous points in the proceeding when Judge Glenn opened up discussion to courtroom participants? In its defense, the CFTC might claim that the reference was the broker-dealer, an area out of its authority, and thus its input was not required. This is false, however, because Judge Glenn asked a question relative to the funds shortfall, which involved the CFTC. The FCM / BD were one corporate entity. This moment in court dramatically impacted the bankruptcy process for the FCM and MF Global customers. The CFTC had an obligation to protect commodity market integrity above all else and report suspected criminal behavior to the court. The CFTC lawyer in court had an obligation to report it not only from their obligations as lawyers, but also do the CFTC’s core stated mandate to protect commodity market integrity. Anyone knowledgeable of the facts and regulatory legal proceedings, such as a CFTC lawyer, should be expected to recognize the critical misdirection of a fraudster. One would assume the CFTC had read the work of CFTC Commissioner Bart Chilton and his book Ponzimonium? This book detailed tactics of a fraudster, which is misdirection and the creation of confusion. What was occurring in court was a classic case of misdirection. How could this go without notice by a skilled CFTC lawyer? Footnotes: 1) Under Section 1104 of Chapter 11 bankruptcy code, the court can (and should) be compelled to immediately appoint a Trustee or Examiner when there is evidence of mismanagement or fraud, etc. and according to the code: Sidebar: |

|

This article was published in Opalesque Futures Intelligence.

|

{kind=link}