RSS

RSS|

S&P Dow Jones Indices have been a leader by being the first to attempt to replicate "managed futures performance" through a general investable index. The first version of the index was the S&P DTI. This index, based on a one dimensional seven month moving average cross trend trading method, was based on the trend following method developed by the legendary Victor Sperandeo, also known as "Trader Vic." This index had come under criticism from some in the managed futures industry who claimed it did not represent managed futures performance in the aggregate. This index was used as the basis for the early managed futures mutual funds and ETFs, then Rydex (now Guggenheim) and Wisdom Tree. As algorithms developed in sophistication, so to did the development of algorithms at S&P as elsewhere in managed futures. Mathematical pioneers such as David Harding of Winton Capital and Ray Diallo of Bridgewater have said to have developed methods of using computer algorithms to determine market environments and then select the appropriate trading algo. This type of maturing of the mathematical formulas used to manage investments has occurred throughout the industry including S&P Dow Jones Indices. After launching the S&P DTI index, they, too, branched out into index strategies to better reflect the space..The first evolutionary step was DFI (Dynamic Futures Index), an index similar to DTI, though each constituent can independently go long or short and there is a different roll. Further, under Ms Gunzberg's guidance, S&P Dow Jones Indexes launched the S&P SGMI (Systematic Global Macro Index), a much more advanced index that hasan interesting look back feature designed to adjust for market conditions. Click here for a previous review of the index Click here for a previous review of the index. Also for more information on Strategic Futures from S&P Dow Jones Indices please : click here In summer of 2011 S&P (Ratings) made a historic downgrade of the US debt market, shocking some in the industry for speaking out on the then mostly unmentionable topic. Some, including myself, viewed it as a brave Paul Revere move. (S&P Ratings is a wholly separate firm from S&P Dow Jones Indices). Today, as a debt clock graces the Republican Convention and Vice Presidential candidate Paul Ryan has brought the unmentionable topic into the public realm, the S&P managed futures indices face the future. It is from this point we pick up our previous conversation with Ms Gunzberg INTERVIEW : JODIE GUNZBERGOpalesque Futures Intelligence (Mark Melin): Let's discuss the economic rationale for managed futures. On a going forward basis, why does managed futures make sense right now? Jodie Gunzberg: Investors have recently shown interest in managed futures, particularly since 2008, when they were the only asset class to perform well through the financial crisis. Further, they have held up during other past crashes and tend to provide strong downside protection with relatively low drawdowns. This protection, combined with the positive performance during bull markets, is called convexity and is very attractive to investors. It currently drives strong demand for futures, especially as there's low correlations to traditional asset classes like stocks and bonds. So now is an ideal time for the managed futures indices that capture positive and negative price trends through global futures. OFI: Tell me about your background and how you became involved with managed futures? I have been in the industry for 17 years and spent the first half of my career on the buy-side,as an analyst and risk manager, and the second half in investment consulting, until I joined S&P Indices - which merged which Dow Jones Indices in July this year and is now known as S&P Dow Jones Indices. The potential return and data availability of equities was appealing, though I also liked the mathematics of bonds and the tangible quality of real estate. Commodity futures seemed to have the perfect combination of the three, which is what I learned while publishing research during my time at Ibbotson Associates. In the educational process to teach clients about commodities, there comes a time where managers need to be given recommendations, and this is when I realized that most managers of institutional quality are trading financial futures alongside commodity futures, in order to diversify the risk in their own portfolios. Looking atthe difficulty involved with picking an active Commodity Trading Advisor (CTA)that will consistently outperform the market, in conjunction with correctly timing entry and exit points; I became a believer in passive investing. JG: Strategic futures indices, like the S&P SGMI and S&P DFI, allow investors to access managed futures as an asset class directly, which has been traditionally difficult because of the relatively high prices, high minimums and low liquidity of many individual active CTAs. By enabling investors to invest in futures directly via an index product rather than through a fund of funds, S&P Dow Jones Indiceis "betatizing" an asset class which has been generally considered alpha. As quantitative models have become more sophisticated, the managed futures indices have evolved to detect the most current, stable historical price trends to determine whether each constituent is long or short. The most advanced versions can employ different time-frames for each constituent's trend each month, where positive trends signal long positions and negative trends signal short positions. Also, the newer indices may use leverage in conjunction with risk capital allocation weighting, in order to achieve market risk levels. OFI: Does the use of leverage fluctuate based on market environment or volatility? In a direct managed futures account the investor can see the daily leverage usage. The benchmark for trend following averages around 16% depending on what data you are looking at. Is it appropriate for the investor to understand how leverage is used? JG: The use of leverage varies depending on the index in question; however, the most recent indices representing managed futures, the S&P SGMI and sub-indices, apply leverage that fluctuates based on volatility. If the volatility of the constituents and correlations between them is relatively low, then more leverage is used in order to take enough risk to achieve a characteristic market level. However, there is a 300% gross exposure or 3x leverage constraint at every monthly rebalance to enable investable products to easily track the index. Not only is it appropriate for investors to understand how leverage is used but it is an important part of understanding the risk to take in order to earn a return. A common misconception for users that are first learning about managed futures is that they think money is actually being borrowed in order to get the leverage. They need to learn that most of the required minimum margins allow for far greater leverage than what is permitted in the standard indices and that the leverage is controlled by the number of contracts bought and sold. What are you seeing as primary developments with managed futures as it relates to distribution through equity channels? Any trends emerging? JG: There have been more advanced indexing strategies launched and offered through exchange traded products like ETFs, which allow retail investors to access managed futures for the first time without the challenges that might typically come with investing through active CTAs. OFI: In terms of managed futures, I want to address another topic that is likely to come up as the asset class grows in popularity. Detractors of the managed futures industry are comparing managed futures "performance" based on the small handful of managed futures mutual funds. They make the accurate claim that if you look at performance dating back before 2008 - when managed futures industry turned in heroic uncorrelated investing performance - that managed futures has not been profitable based on the two managed futures mutual funds in existence. Is it appropriate to benchmark managed futures performance based on all but a handful of managed futures programs? JG: S&P Dow Jones Indices' strategic futures indices are designed to represent the globalmacro and managed futures/CTA universe. The indices use quantitative methodologies to track the price trends of globally diversified portfolios of commodity, foreign exchange and financial futures contracts. By using futures contracts directly rather than select CTAs to create a fund of funds, the benchmark is an aggregate market representation rather than a biased sample of programs, which we feel is the most appropriate market proxy. OFI: Thank you for your responses, Jodie. Interesting insight.

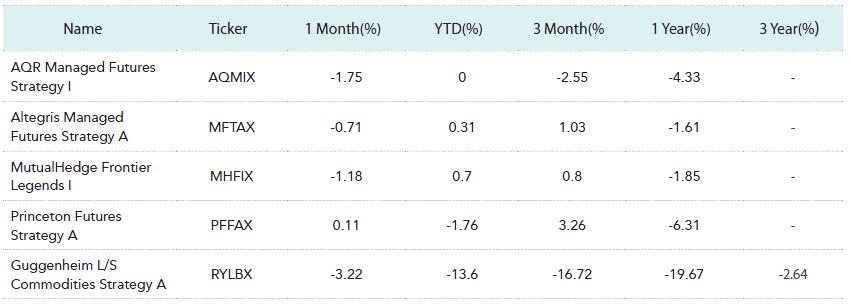

About Jodie Gunzberg: In addition, Jodie writes index methodologies, educational material and market commentary. Prior to joining S&P Indices, Jodie held various roles within the consulting and the investment management business. She managed portfolios in various asset classes including real estate, fixed income, equities, and hedge funds. Most recently, Jodie was the chief investment strategist for an investment consulting firm overseeing over 350 plans ranging in size from US$ 10 million to US$ 13 billion, totaling more than US$ 85 billion in assets. Jodie has published many industry pieces on hedge funds and commodity investing, and is a frequent panel speaker and moderator. Jodie is a CFA charter holder, member of the CFA Institute and NYSSA, and is a former director on the Board of Directors for CFA Chicago. She received her M.B.A. from the University of Chicago, Booth School of Business, and earned a B.S. in Mathematics from Emory University. Managed Futures Mutual Fund Performance Sampling

Coming in the next issue: Performance comparison across account types. Source: Morningstar Past performance is not indicative of future results. There is risk of loss when investing in futures and options. |

|

This article was published in Opalesque Futures Intelligence.

|

{kind=link}