RSS

RSS|

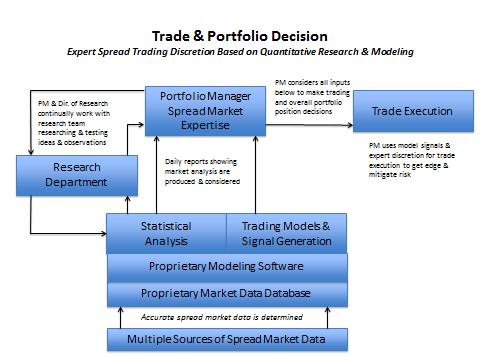

Note: This profile is written for professional money managers and QEP investors only. It includes frank discussions of investment volatility and how market environments can influence strategy drivers. The article may express significant opinions and may not have considered all risk factors. It is not a recommendation to invest but rather a look at risk management through the lens of how a strategy operates. Past performance is not indicative of future results. Trading futures and options is not suitable for all persons and can involve substantial risk of loss. Spread arbitrage trader Emil Van Essen is a study in how a managed futures program might adapt a research and trading approach that adjusts with shifting market environments. While professional investors may be most familiar with the managed futures trend following strategy, the most popular strategy, Van Essen is known for a spread arbitrage strategy. Understanding different strategies in managed futures can be beneficial, because they point to how a portfolio might be built with uncorrelated strategy components. In spread trading, for instance, such strategies are generally known to operate based on price relationships between related products. As an example, a spread arb strategy may sell July corn and purchase December corn with the objective that the price of the July contract may fall relative to the price of the December contract. This strategy can be influenced by the market environment of price dislocation with convergence back to the mean, a topic addressed in the book Spread Trading, by Keith Schap.1 Contrast this to trend following, where a primary strategy driver is considered to be a market environment of price persistence, and professional investors might understand some of the high level risk management considerations.2 With this knowledge risk management relative to market environment may be better understood by the investor. See related article Understanding Spread Arbitrage strategy drivers. The Genesis of a Spread Trading Model “We have always made it a priority to learn from our market experiences and to find trading opportunities by watching markets closely,” said Emil Van Essen, whose 25 years in the markets has included trading and modeling. “We constantly conduct research to improve our understanding of the current market environment and how it affects our investment strategy.” It’s interesting to witness managed futures programs as their trading algorithms expand. This happened in trend trading, as many of the original “turtle strategies” with single algorithmic formulas eventually gave way to today’s trend trader, some of whom are known to use significant numbers of mathematical formulas for trade execution, and some formulas that are said to attempt to determine the market environment and then select the appropriate trade algorithm.2 Just as trend following has generally evolved so, too, has spread arbitrage. The van Essen program offers interesting insight into how a firm can learn from history and develop solutions for an uncorrelated investing world. While spread trading is interesting, understand that as in all strategies, risk exists. Past performance is not always indicative of future results, which is why a program’s risk management is important. While the performance of the van Essen program strategy might stand out, a professional investor’s attention should really be on the subtleties of risk management. In this article we discuss the primary structure of the van Essen program, and then in the password protected version provides more information about risk management and the use of leverage. Spread / Arb Roots in ETF Roll The van Essen program was originally launched as a roll arbitrage strategy that was developed upon the advent of long-only commodity funds and the expansion of electronic spread trading, according to Dennis Callahan, Director of Trading, who has been with van Essen program since its inception. In the past, commodity ETFs have been said to enter and exit markets in a somewhat predictable strategy, and the related bulk order entry has, in the past, created what is known as a temporary supply and demand imbalance the futures markets. It is important to note that all markets have practical limits. When a rush of orders occurs in one direction, price dislocation can tend to occur, regardless of what “efficient” market theory may dictate.3 “The effective modeling of the impact of index funds and other market forces on spread prices allowed us to attempt to profit from spread price movements near the roll date,” van Essen explained. Seeking to take advantage of his research and modeling capabilities and to mitigate risk, van Essen added other spread trading strategies to his initial roll arb strategy. He also adjusted leverage and added a hedge risk overlay. My interview with van Essen follows below. Opalesque Futures Intelligence (OFI): Will you provide details relative to the primary strategy and how you execute that strategy? van Essen (vE): The program was originally launched as a roll arbitrage strategy that was developed upon the rapid growth of long-only commodity funds and the expansion of electronic spread trading. The effective modeling of the impact of index funds on spread prices allowed us to take advantage of price movements in spreads near the roll date as long only funds rolled their commodity futures contracts. OFI: So when a long only commodity fund or ETF transfers positions from the front month of a futures contract to a back month, as an example, the relative impact on supply and demand in the market place has potential to dislocate prices to a degree. You strategy is to then rely on prices to revert back to the mean. An example of this might be a September roll, for example, where a particular commodity contract may expire in September and the fund or ETF is required to transfer positions from the September contract prior to expiration to a longer dated contract in December, for instance. This activity can potentially create a temporary supply and demand imbalance, but obviously past performance is not always indicative in an unpredictable future. The strategy performs positively and negatively. When prices dislocate and converge back to the mean, and it generally experiences enhanced risk during times when prices do not revert back to historic means, which is a general explanation of spread arbitrage programs at a basic level.1 How has the strategy matured over time as market environment has expanded? vE: Although the roll arbitrage strategy was historically successful as a stand-alone strategy, we believed that expanding into a multi-model strategy would potentially reduce risk and improve risk adjusted returns. We also wanted to take advantage of our modeling and research capabilities to look outside of the roll periods and find trading opportunities throughout the term structures. We found that we could trade spread price trends similar to the ways outright markets are traded. For example the spread may be long-term trending, mean reverting, etc. In addition, we identified dislocation and convergence opportunities across commodity term structures. We have also evolved from trading strictly term structure or intra-market trades to relative value or inter-market spreads. OFI: This is interesting. So you went from a straight roll arb spreading strategy to trading spread relationships throughout the term structure and across markets. How were you able to make this transition? vE: It’s important to note that we have always stayed true to our spread trading roots, but our research and modeling platform have allowed us to evolve and expand. This has been critical for us because the commodity markets have changed and are changing rapidly. Even our roll arb strategy has changed over time. As the commodity funds change their roll strategies and more speculators seek to profit from the rolls, our method and timing of trading the roll have changed. In general, our style is opportunistic; we are seeking to uncover spread trading opportunities across the term structure that we believe possess the best risk-reward characteristics. OFI: Explain your investment process. You have talked about technical research and modeling, how much discretion do you use. How do you identify and filter trade opportunities? vE: Our Investment Process is a hybrid of model and discretionary trading. Term structure and relative value spread trading in commodities includes a number of complexities, execution challenges and rapidly changing market dynamics that require a discretionary overlay in the investment process. We believe that maximizing alpha generation and minimizing risk requires detailed modeling and ongoing research. In short, we continually examine current and historical spread markets seeking opportunities that could provide significant alpha and a sustainable edge. The trading opportunity is then researched, tested, and the results are compiled in a database. Results are then filtered and the new model is optimized for integration into our strategy. We then employ discretion to adjust model weightings to procure trades with the best perspective risk/reward characteristics. Fundamental information is then used in an attempt to protect against unforeseen problems that may not be apparent in modeling such as hurricanes, drought and other factors. Figure 1 below provides an overview of this process:

OFI: That’s a detailed process and very beneficial for investors to understand how decisions are made and potential risk management approaches being considered. How are trades executed and over what markets?

Footnotes:

FTC RISK DISCLOSURE: PAST PERFORMANCE IS NOT INDICATIVE OF FUTURE RESULTS. THE RISK OF LOSS IN TRADING COMMODITIES CAN BE SUBSTANTIAL. YOU SHOULD THEREFORE CAREFULLY CONSIDER WHETHER SUCH TRADING IS SUITABLE FOR YOU IN LIGHT OF YOUR FINANCIAL CONDITION. THE HIGH DEGREE OF LEVERAGE THAT IS OFTEN OBTAINABLE IN COMMODITY TRADING CAN WORK AGAINST YOU AS WELL AS FOR YOU. THE USE OF LEVERAGE CAN LEAD TO LARGE LOSSES AS WELL AS GAINS. YOU COULD LOOSE ALL OF YOUR INVESTMENT OR MORE THAN YOU INITIALLY INVEST. IN SOME CASES, MANAGED COMMODITY ACCOUNTS ARE SUBJECT TO SUBSTANTIAL CHARGES FOR MANAGEMENT AND ADVISORY FEES. IT MAY BE NECESSARY FOR THOSE ACCOUNTS THAT ARE SUBJECT TO THESE CHARGES TO MAKE SUBSTANTIAL TRADING PROFITS TO AVOID DEPLETION OR EXHAUSTION OF THEIR ASSETS. THE DISCLOSURE DOCUMENT CONTAINS A COMPLETE DESCRIPTION OF THE PRINCIPAL RISK FACTORS AND EACH FEE TO BE CHARGED TO YOUR ACCOUNT BY THE COMMODITY TRADING ADVISOR ("CTA"). THE REGULATIONS OF THE COMMODITY FUTURES TRADING COMMISSION ("CFTC") REQUIRE THAT PROSPECTIVE CUSTOMERS OF A CTA RECEIVE A DISCLOSURE DOCUMENT WHEN THEY ARE SOLICITED TO ENTER INTO AN AGREEMENT WHEREBY THE CTA WILL DIRECT OR GUIDE THE CLIENT'S COMMODITY INTEREST TRADING AND THAT CERTAIN RISK FACTORS BE HIGHLIGHTED. THIS DOCUMENT IS READILY ACCESSIBLE AT THIS SITE. THIS BRIEF STATEMENT CANNOT DISCLOSE ALL OF THE RISKS AND OTHER SIGNIFICANT ASPECTS OF THE COMMODITY MARKETS. THEREFORE, YOU SHOULD PROCEED DIRECTLY TO THE DISCLOSURE DOCUMENT AND STUDY IT CAREFULLY TO DETERMINE WHETHER SUCH TRADING IS APPROPRIATE FOR YOU IN LIGHT OF YOUR FINANCIAL CONDITION. YOU ARE ENCOURAGED TO ACCESS THE DISCLOSURE DOCUMENT. YOU WILL NOT INCUR ANY ADDITIONAL CHARGES BY ACCESSING THE DISCLOSURE DOCUMENT. YOU MAY ALSO REQUEST DELIVERY OF A HARD COPY OF THE DISCLOSURE DOCUMENT, WHICH WILL ALSO BE PROVIDED TO YOU AT NO ADDITIONAL COST. THE CFTC HAS NOT PASSED UPON THE MERITS OF PARTICIPATING IN ANY OF THESE TRADING PROGRAMS NOR ON THE ADEQUACY OR ACCURACY OF ANY OF THESE DISCLOSURE DOCUMENTS. OTHER DISCLOSURE STATEMENTS ARE REQUIRED TO BE PROVIDED YOU BEFORE A COMMODITY ACCOUNT MAY BE OPENED FOR YOU. MUCH OF THE DATA CONTAINED IN THIS REPORT IS TAKEN FROM SOURCES WHICH COULD DEPEND ON THE CTA TO SELF REPORT THEIR INFORMATION AND OR PERFORMANCE. AS SUCH, WHILE THE INFORMATION IN THIS REPORT AND REGARDING ALL CTA COMMUNICATION IS BELIEVED TO BE RELIABLE AND ACCURATE, NOT WARANTEE RELATIVE TO SAME IS AVAILABLE. THE AUTHOR IS REGISTERED WITH THE NATIONAL FUTURES ASSOCIATION. |

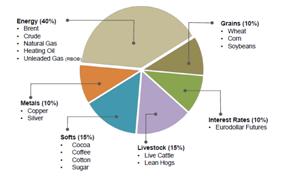

VH: Due to the complexities of spread trading, trade execution is discretionary within model defined price ranges and time lines. Trade orders are entered either electronically or via CME ClearPort where positive slippage, risk mitigation and execution edge is accomplished via the utilization of veteran traders each with over 25 years of market experience. We believe that using a manual trade order entry process as opposed to an automated algorithmic system enables us to get an edge many trades. The contracts traded in the program may include WTI and Brent Crude Oil, Heating Oil, Natural Gas, Heating Oil, Unleaded Gas, Copper, Silver, Cotton, Sugar, Coffee, Cocoa, Livestock, Wheat, Corn, Soybeans, Eurodollars, Euribor, Short Sterling and other exchange listed interest rate futures.

VH: Due to the complexities of spread trading, trade execution is discretionary within model defined price ranges and time lines. Trade orders are entered either electronically or via CME ClearPort where positive slippage, risk mitigation and execution edge is accomplished via the utilization of veteran traders each with over 25 years of market experience. We believe that using a manual trade order entry process as opposed to an automated algorithmic system enables us to get an edge many trades. The contracts traded in the program may include WTI and Brent Crude Oil, Heating Oil, Natural Gas, Heating Oil, Unleaded Gas, Copper, Silver, Cotton, Sugar, Coffee, Cocoa, Livestock, Wheat, Corn, Soybeans, Eurodollars, Euribor, Short Sterling and other exchange listed interest rate futures.|

This article was published in Opalesque Futures Intelligence.

|

{kind=link}