|

Long-Term Commodity Investing

Steven Baffico, senior managing director at Guggenheim Partners, gives a broad perspective on commodity investing centered on the theme of

long-term supply constraints.

Commodity markets and concerns about supply often make headlines. Recently the Group of 20 agreed on measures to improve food supplies

(see figure below). And the US and other countries started to release 60 million barrels of emergency oil reserves to make up for Libyan

exports-a casualty to political turmoil.

In the past decade investors have increasingly bought into commodities in a variety of ways. Mr. Baffico explains the reasoning behind

various types of investments and the advantages and disadvantages.

Guggenheim Partners manages and allocates to different investment strategies. This diversified financial services firm, currently

responsible for around $100 billion in assets, originated as the Guggenheim family office.

"You may seek to efficiently express in your portfolio a secular view or to do price arbitrage to capture inefficiency in the short run."

Opalesque Futures Intelligence: What role do commodities play for investors?

Steve Baffico: At Guggenheim, we generally take a long-term investment view and that's reflected in portfolio construction and the

role commodity investing may play in an allocation. That assessment starts with the observation that with many commodities, global supply is

under pressure from fast-growing emerging economies. As people have pointed out, the dynamics of global commodities consumption are changing

dramatically while delivery conduits are strained and infrastructure is largely antiquated in many commodities markets such as oil and

natural gas. This makes it difficult to readily expand supply. Guggenheim believes that secular growth trends can be expected to put upward

pressure over time on demand levels and hence, prices of natural resources and commodities. From this long-term perspective, we believe in

adding commodity exposure to traditional portfolios both for attractive total return and diversification. The question is how you mitigate

the risk of the inherent volatility in commodity markets. If you believe in secular opportunities, what's the best way to access that trade?

OFI: Do you see particular commodities as more promising?

SB: Emerging markets growth has strong impact on certain commodities. Agriculture is an excellent example. Our chief investment

officer, Scott Minerd, expects that the developing markets growth trend will be a long-term one and bring sustainable rising

GDP per capita. We continue to witness mass migration from agrarian to urban areas in a number of developing countries, with China being

the most notable and having the greatest impact. So you have hundreds of millions of people becoming more sophisticated consumers with more

discretionary income. As that happens, their diet is becoming more sophisticated as well, with substantially greater consumption of protein.

In economic terms, it takes nearly ten times the input and cost to produce a pound of meat versus a pound of grain. So there should be no

surprise that there's been dramatic rises in agricultural prices. We think this is a longer term trend.

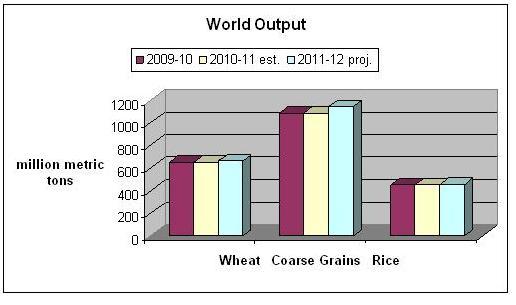

Global supply is not expanding while demand grows for certain commodities.

Coarse grains: Corn, sorghum, barley, oats, rye, millet and mixed grains.

Source: US Department of Agriculture.

OFI: What other commodities are likely to trend upward over time?

SB: Another strong impact of urbanization is through the construction of infrastructure and the building up of cities. Think of all

the new cities being built in China, which creates an enormous demand for industrial metals used in construction, in particular steel,

copper, aluminum and nickel. This has driven up the prices of these metals in both the spot and futures markets. In addition to agriculture

and industrial metals, there is a third area, namely precious metals. Inflation in emerging markets, mainly driven by rising food prices, is

showing up in the price of gold.

OFI: Is inflation a big part of the commodity story?

SB: Investors both here in the US and elsewhere seek a way to hedge their portfolio against inflation. While inflation is low here,

the growth of the money supply suggests it may be a future threat. If you expect inflation, you'll want to be in commodities because their

prices generally rise with inflation-the correlation is significant.

OFI: Does this long-term picture favor index investments?

SB: This does not necessarily point to index investments. It does not mean you should put the allocation into the portfolio and forget

about it. I've outlined some of the secular upward trends in commodities but along the way there will be periods of correction and

consolidation in these markets. At times, prices are driven by temporary factors like geopolitical events. Political unrest in the Middle

East and North Africa has led to a higher range for oil prices. On the other hand, concern that US growth is weakening pushed down prices.

Because of all these variables, opportunities for price arbitrage frequently present themselves.

OFI: How do you put the secular trend into a portfolio?

SB: You can take a direct investment route or an indirect route to get commodities exposure in a portfolio. The potential benefits of

a direct investment like a commodity index its strong correlation to movements in price. The drawback is that futures-based funds can have

significant tracking error because of the contract rolling process.

OFI: What is the indirect route?

SB: The indirect strategy is to invest in the equities of companies in the natural resource and commodities space. This has certain

advantages. Company stocks may outperform the underlying commodities because forward-looking expectations in the equity market factor in the

upward trend. Long-term trends can be efficiently expressed through indirect exposure. Clearly there are drawbacks as well. This type of

commodity play will be more correlated to the equity market than the hard assets and there is risk that a company will lag the underlying

physical asset because it is not managed well.

OFI: How do you decide which route to go?

SB: You have to think of what's more important to you as an investor and consider the pluses and minuses of different types of

investments.

OFI: Do you have examples to illustrate the choices?

SB: In the US, we have a number of funds that focus either on a specific commodity or countries that stand to benefit the most from

rising commodity markets. The Guggenheim timber ETF - its ticker is CUT, by the way - invests in companies that own and manage timber

properties. Here's a short-run, tactical way to play this. A pretty aggressive post-earthquake rebuilding effort is now going on in Japan,

where government buildings are required to use lumber of a certain grade. You can get exposure to companies in that lumber market via CUT.

The foundational approach would be to hold it long-term to gain from the secular growth of infrastructure and the demand it creates for

timber.

OFI: You mentioned a regional approach. How does that work?

SB: One way to approach the commodity boom is through the "ABC" story-Australia, Brazil and Canada. Guggenheim believes that there's

going to be more interest in ABC going forward. Whereas the BRIC countries - India and China specifically- are big emerging consumers of raw

materials and natural resources, ABC countries are the larger more developed producers of these commodities. So we've constructed a fund that

invests in companies in ABC that pay high dividends.

OFI: What's the alternative?

SB: You may seek to efficiently express in your portfolio a secular view or to do price arbitrage to capture inefficiency in the short

run. If you want to arbitrage markets, you'll want a multi-directional, long/short strategy. You can buy options on ETFs to in effect go

short. And there are various other products that give you both long and short exposure, such as the Rydex Long-Short Commodities mutual fund.

OFI: What do you see in the future?

SB: We think over the next decade, one of the bottlenecks in commodity markets will be the inability to effectively deliver supply to

meet growing demand. Oil is a good example. To extract oil from large new mega-fields like in the deep water Gulf of Mexico, we need an

enormous infrastructure to harvest it and manage these projects safely. It also takes time. The abundant natural gas fields in Qatar are a

similar story as constructing new pipelines to harvest and processing facilities to refine takes a long time and is very expensive. So given

the long term supply-demand dynamics, we expect continuing pressure on price across many commodities and natural resources. Fortunately,

whether your allocation is a long term foundational one or a short term tactical trade, there are a number of investment solutions.

|

RSS

RSS

{kind=link}