RSS

RSS|

Andre Steyn (andre@steyncapitalmanagement.com) is the CEO and Portfolio Manager of South-Africa based Steyn Capital Management, which he founded in 2008. From 2004 to 2008, Andre? was the CEO of Temujin Fund Management UK, the UK arm of a billion dollar New York based hedge fund. At Temujin, Andre was responsible for all non-US investments comprising a long/short portfolio of approximately USD2 billion. From 2002 to 2004, Andre was an investment associate at Ziff Brothers Investments, a multi- billion dollar hedge fund. At Ziff Brothers, he performed fundamental research for the purpose of recommending new investments for the firm's capital, and generated significant alpha by shorting companies with poor earnings quality. Andre began his career at Andersen in 1998, completing his Chartered Accountant articles in Cape Town before transferring to the New York Mergers & Acquisitions practice where he advised companies and private equity funds on acquisitions. Andre? is a Chartered Accountant and a Chartered Financial Analyst. Steyn Capital has been investing in African markets since 2009, and manages over $700 million in South African long/short, and pan- African and global frontier long only funds. All of these mandates are managed with the same value orientated intensive research focus, and all have outperformed their respective markets since inception, with little to no overlap between each other. The company has a team of 16 with 10 on the investment side and 6 on the operational side.

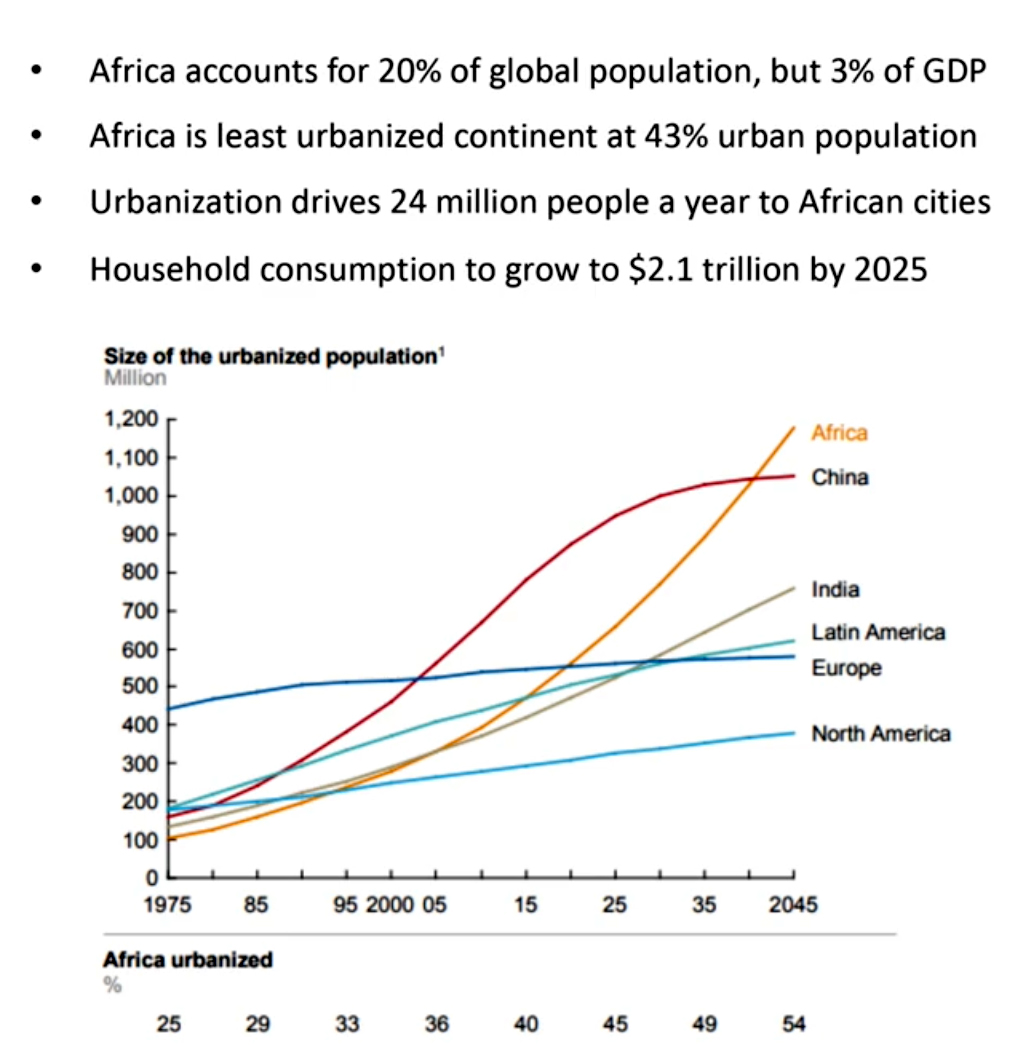

Africa is the fastest-growing continent on the planet. From 2000, half of the world's fastest- growing economies have been in Africa. By 2030, more than 40% of Africans will belong to the middle or upper classes, increasing demand for goods and services. Household consumption is expected to reach $2.5tln, more than double that of 2015 at $1.1tln. Private wealth held in Africa amounts to approximately USD 2.0 trillion as at December 2020, with South Africa, Egypt, Nigeria, Morocco and Kenya forming the "Big 5" wealth markets, accounting for over 50% of the continents total private wealth. Steyn Capital Management is an established African and frontier markets focussed equities investor located in the Winelands surrounding Cape Town, South Africa. The firm has been investing in African markets since 2009 and manages more than US$700m in a South African long/short fund and pan-African and global frontier markets long-only funds. Were speaking with founder Andre Steyn who has also been featured in an Opalesque VIRTUAL MANAGER VISIT at his Cape Town office recently.

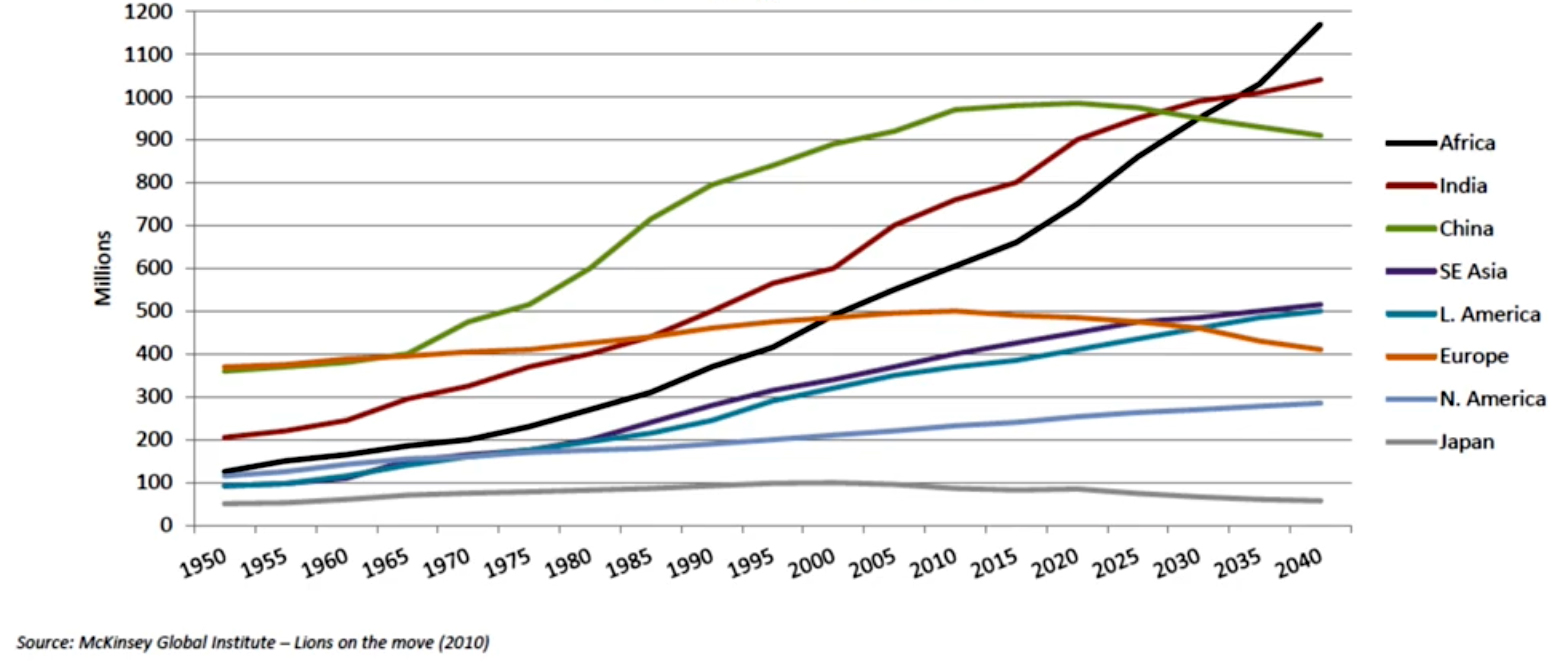

Matthias Knab: Andre, you have a different starting point in the investment industry, please tell us about that, and highlight the benefit of that background to your current strategies? Andre Steyn:I started my investment career as a dedicated short selling analyst at Ziff Brothers Investments, where I applied forensic accounting analysis to ferret out short selling opportunities. This is almost certainly different to any other African or Frontier markets investor. This early experience has led to our excellent fundamental short selling record at our long/short fund in South Africa, where we have added over 400% of cumulative alpha on the short side over 12 years. Being a good short seller is also an advantage on the long side, since you can avoid buying potential short sales. Very early on in our investment process, we invert and run all of our potential longs through our normal short selling process. This is also a great method to increase our return on time, since we organize our research process into a 15 step process, and we stop work and move onto the next idea immediately when there is something that is a deal-killer. Steyn Capital is all about applying developed market research techniques learned during my time at Ziff Brothers Investments and Temujin to identify and take advantage of market inefficiencies. This is why we gravitate towards African and other frontier markets, where is it still possible for intensive research to generate a fundamental edge in a variety of unknown and unloved equities. Matthias Knab: What opportunities are you seeing across African markets, and can you give me some examples of the market inefficiencies you are seeing? Andre Steyn: We are currently targeting investments in franchise consumer businesses, including several of the dominant brewers across African markets, which sports market shares of over 80% and has volumes growing at multiples of developed market beer producers. We also have investments in mobile telecoms with strong FinTech businesses, some of them with de-facto monopoly positions. Lastly, we invest in owners of irreplaceable assets like container ports with excellent pricing power and the ability to collect royalties on African growth over long periods of time. Having spent a decade investing in Africa, we've been able to cultivate a network of relationships and brokers across the continent who send us the flow. One benefit of the investor apathy I'll be happy to talk more about is that it has really provided us the opportunity to take advantage and build meaningful positions in these dominant, high quality businesses. One recent example of this extreme market inefficiency was when we acquired 7.5% of Heineken's business in Rwanda from a fund that was liquidating. While the stock was trading at RFW100, we bid RWF50 for the entire block. Subsequent to our purchase, the company reported earnings up almost 100%, in-line with our expectations, more than doubling the stock price again. While we think that the market inefficiencies will persist, we don't think the investor apathy here will be permanent. The opportunity set is compelling and anecdotally, we have run into several large sovereign wealth funds who are becoming increasingly interested in investing in the continent. Matthias Knab: Looking at the macro picture, why should investors have an allocation to Africa? Andre Steyn: Africa has excellent demographics, with the number of working age adults expected to increase from 700 million today to well over a billion by 2035. This is in sharp contrast with the majority of the rest of the world, which is seeing declines in working age populations going forward. Large and rising working population =

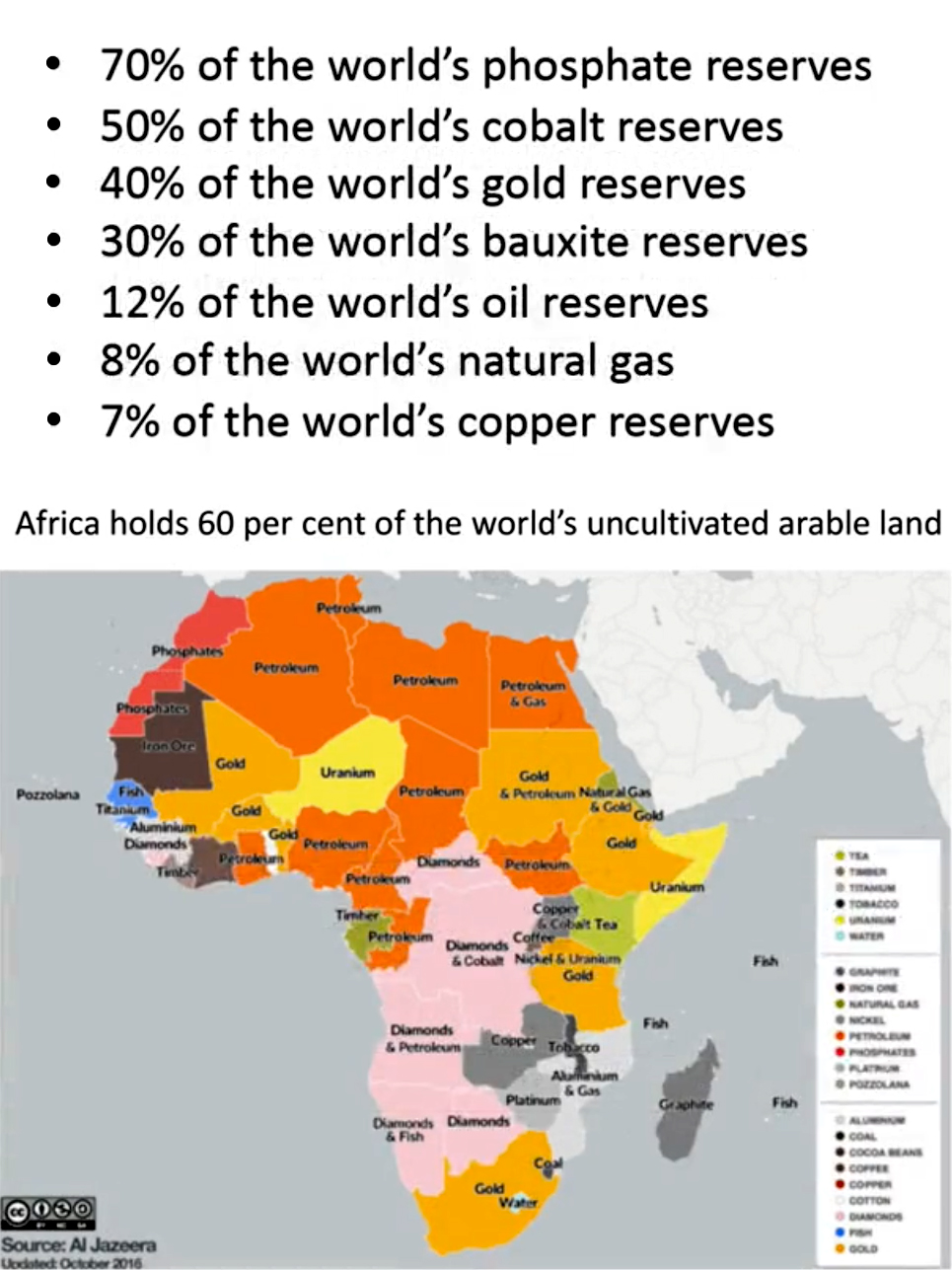

The implications for future demand for infrastructure and consumer goods is clear. Africa is also seeing rapid urbanization with 25 million people a year moving to cities, which is a further driver of built-in demand. Africa is also home to 30% of the world' natural resources, much of this unexploited and only now coming into focus for international investors.

Given this highly positive demographic backdrop, you would be surprised to learn that African investment markets are extraordinarily undervalued, as a result of investor apathy. Our Africa fund is now trading at approximately 6x EV/EBIT, which is close to the lowest valuation over the decade that our fund has been investing. The key difference this time around is that our concentrated portfolio of 17 high conviction names is the highest quality that it's ever been. The portfolio generated a ROIC of 55%, and has a weighted average market share of almost 70%, illustrating the market dominance of these businesses. The multinationals we speak to about their African businesses see this as a multi-decade growth opportunity, and we are very excited to be a part of this. Matthias Knab: What is your investment process when you invest in Africa? Andre Steyn: I believe that we benefit from four competitive advantages. Firstly, we have created a proprietary investment screen where we have a team of three idea generation analysts who comb through source financial statements, cleaning up the extraneous earnings items and adjusting for hidden assets and liabilities to give us a great starting point for further research. Our team has over the last decade created a proprietary universe by eliminating all lower quality businesses, including most extractive industries, and ending with a screen comprised of only 500 super high quality African business, all of which is updated by one of our idea generation analysts for new earnings announcements. Secondly, we focus on high quality companies that are not recognized or priced as such. Frontier markets investors tend to focus on the bigger index constituent names, whereas we have been generalists for 20 years looking at hundreds of different business models. We believe that we have an uncommonly good understanding of what makes a superior business, and we have been consistently paid by owning these. Thirdly, we apply the forensic accounting and value added research skills learned at Ziff in order to avoid pitfalls and generate a true edge into our holdings. There are many ways for public companies to massage reported earnings numbers in order to hide fundamental weakness or strength, and it is one of our key skillsets to identify this and convert reported results into economic reality. Companies that hide fundamental weakness with accounting tricks tend to miss reported earnings with great regularity, and so it is important to avoid these on the long side. Value-added research means not just talking with the management team, but conversing with customers, competitors and suppliers to gain a true edge into the business. Lastly, we size our funds appropriately in order to be nimble investors in these smaller markets. We have a demonstrated track record of closing our funds to new investment in order to preserve the opportunity set for existing investors. Notwithstanding, our funds have sufficient size in order to afford top notch research and operational talent and investment. Given the exceptional opportunity set in Africa, our funds are currently open to investment, with remaining capacity of approximately $400 million. | ||||

|

Horizons: Family Office & Investor Magazine

Andre Steyn: Global investor apathy leaves Africa's multi- decade growth opportunity to few on the ground managers |

|

{kind=link}