RSS

RSS|

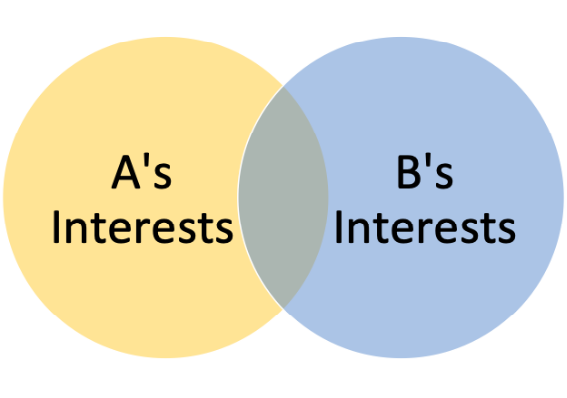

David is a second generation family member who went from software developer to technology entrepreneur to family advisor, writer and speaker. He wrote the bestselling book Transition on intergenerational wealth, has a science degree, a masters in entrepreneurship, and is an Adjunct Professor at Swinburne University (family governance and entrepreneurship). Conflict Resolution in Wealthy Families When it comes to conflict resolution, families and especially wealthy families pose additional challenges. In this article, I will present a framework for conflict resolution, and then see how it can be used to understand family conflicts and their resolution, and derive some learnings about what techniques are and are not helpful in that context. In this model, there are essentially three methods to eliminate conflict: power, rights, and interests. This is derived from the Harvard University Getting to Yes theory of negotiation. 1. Power is a very effective way to resolve a conflict. For example, if a young child says I want to do X, and their parents do not want them to, they can simply say no, and the conflict is quickly and simply resolved. In this case, there is a power imbalance between parents and (young) children and they have sufficient authority that a no is adhered to. It is crude, but it works. A more salient example might be when an adult family member wishes to gain access to the family wealth, and the assets are held in a trust where control of that wealth rests entirely with the older generation. In that case too, there is a power imbalance in respect of the assets, and a simple no will quickly resolve any conflict over deployment of the assets. While this method works remarkably well, it doesnt truly end the conflict. Because one partys power has been invoked, the other party is by definition disempowered through the process. Being on the other end of the exercise of power can lead to resentment and hurt feelings which can fester and blow up at a future date. When using power to resolve a conflict, one may win the battle but lose the war. This is both because of the very side effect of using power, and also because its very difficult to hold on to power forever. That means the use of power can have a time limit. 2. Resolving a conflict using rights is the next step up in sophistication. In that scenario, each party to the conflict submits to some external and independent standard and uses that to resolve their differences. The standard could be a contract between the parties, the law, an arbitrator or mediator, or a court of law (as far as the parties choose to take it). Because this method relies on a standard, it can result in a fairer outcome than the use of power. One party may not be happy with the outcome, but having agreed to the standard, it is reasonable that they must abide by the ruling that flows from that standard. Returning to our family wealth example, a family member seeks access to the wealth, and there is a family agreement in place that sets down the distribution policy. The family agreement is the standard for resolving the conflict the set of rules that all family members accept and adhere to. If that standard is unacceptable, it may be challenged by using another standard, such as through litigation. Even in that case, the same method of rights is being used to resolve the conflict. Results using this method do not have a time limit, as when someone uses power but that power is eventually gone. Depending on the standard chosen, the process can take much longer. If matters end up in court, they can drag on for years, chew up huge legal costs, and cause significant collateral damage to relationships (although those relationships may already have been broken well before the decision to litigate is taken). Significantly, while the process is fairer than the use of power, it will result in one party being deemed right, and another party being wrong, which may leave the losing party aggrieved by the process. That again means the conflict may not truly go away, especially when the parties remain connected by family bonds. 3. That brings us to the optimal method of dispute resolution, using interests. In the previous two methods, we never delved deeper than the face of the conflict: one party wants X, and the other party wants Y (or doesnt want X). When we seek to resolve the dispute using interests, we start asking a very important question: what do you really want This is especially relevant in family disputes because the manifestation of conflict is often just that a manifestation of deeper, family-related issues that just happen to be expressed in financial terms. For example, when a younger family member asks to be appointed CEO of the family business, they may really want to correct perceived favouritism, for their talents to be suitably recognised, or to be in a position of power where they can exact revenge on other family members. The current CEO an older family member who says no may actually be desperate to cling to their position because their personal identity is bound up in their role within the family business, or because they have reserved the CEO position for another, more favoured, member of the family. To resolve the conflict using interests, the parties come together and discuss their interests what they really want to achieve and what sits behind the position they expressed. This is best done with the assistance of an independent mediator or facilitator who can help the parties draw out and discuss their true interests. They may be more comfortable discussing their interests first with the facilitator, and getting assistance in presenting them when the other party is present. Simplistically, we can express the interests of each party using a Venn diagram, as below.

The interests-based methodology identifies the interests of each party, and then finds where those interests overlap (if they do). That area of overlap represents the universe of possible resolutions that can meet both As and Bs interests. This can lead to an optimal win-win resolution that can leave both parties satisfied with the outcome. Lets consider a case study, based on an earlier example and a typical combination of real life factors I often come across when working with families. The family in question has more than half of its wealth in an operating business, and the balance is a mix of real estate and passive investments managed through private banking. The wealth originator has passed away, and the second generation son Alan, 62 years of age, is CEO of the operating business, in which several family members of second and third generation are employed. The operating business has a board, and the family has an investment advisory board (chaired by Alan) which is responsible for asset allocation and instruction to the private banker. A third-generation family member, Brad, son of the CEOs youngest sister and aged 25, has an idea for a business venture and wants the family to invest in it. Alan has never had a good relationship with Brads mother, and there are ten years between them. Brads idea is not met with any enthusiasm whatsoever. Using our framework, what are the ways this conflict can be resolved 1. Power. Alan says no, and uses his influence on the investment advisory board to ensure they back his position. This leaves Brad is upset and frustrated. His mother does not have sufficient capital to fund the venture on her own, nor influence at board level to change the decision. 2. Rights. Alan is still not in favour, but wants to give Brad a chance, so allows him to present to the investment advisory board. If they approve the venture, they will invest half provided Brad can raise the other half externally. Seeking external validation of the venture is always a prudent approach, and while Brad is successful raising half the money, the board is concerned about the stark departure from the familys risk profile, and votes against investing. Brad gave it his best shot, but is disappointed the family doesnt share his view of the importance of diversifying. 3. Interests. Alan and Brad first meet separately with Charles, a family advisor and facilitator, to discuss their interests. Alan has a strong attachment to the family operating business that his late father started, and thinks that should remain the primary vehicle of future wealth creation for the family. He doesnt think much of Brad, who has completed a university degree and worked elsewhere for several years, but was only 15 when his grandfather died, never worked in the family business, and doesnt share Alans view of the primacy of the business to the family legacy. Alan feels investment in a single startup does not fit with the overall risk profile of the company, although he notes that the investment advisory board has been considering an allocation to some VC funds with good track records. Understandably, Brad has a very different view of the world. He talks to his first cousins (there are 13 in his generation) about innovation, startups and venture capital, and some of them share his enthusiasm, others dont at all, and a third group have no interest. He has attended the annual family briefing and has a fair understanding of the family asset base and how it is allocated. He views the possible investment in his venture as throw away money and doesnt understand why the family wont give him a chance to prove himself in his way (as opposed to several of his cousins, who are working in the family business). He would like to see the family eventually diversify into entrepreneurial risk as another significant source of wealth creation. While hes not interested in joining the family business, he does want guidance and mentorship in his journey, and not to carry the burden of doing it all alone. Charles coaches Alan and Brad separately toward a conversation where they share their interests and map them out on a whiteboard. The conversation is focussed initially on identifying the overlap in their interests, and using that as a base to consider options. It turns out they agree in principle that the family should seek further diversification, and that a single investment in one startup operated by a family member carries too much risk. They discuss how that risk might be mitigated, and together with Charles, develop a structure by which to achieve this. Together, they write a proposal to the investment advisory board to establish an entrepreneurial risk investment subcommittee comprising two second generation family members of the main board, two from the third generation, plus an independent specialist in VC investment. Their proposed mandate is to develop an investment plan for diversification (to be ratified by the main board), and then to recommend a series of investments. Brad agrees to park his venture idea, but embarks on a number of internships at startups so he can (a) make more informed investment decisions, and (b) prepare to start his own venture, at the appropriate time. The family also identifies an external mentor for Brad, who now sees a future role for himself within the wider family asset base. Alan is happy that any diversification is measured, and has input of older and more experienced minds. The resolution of this issue took nearly two months, and its implementation will take about a year. Importantly, it has resulted in a win-win outcome for both parties, teased out some latent issues that had the potential to explode down the track if not dealt with, and built some bridges between the generations within the family. Contrasting the three methods, it is evident from this case study that while interests-based resolution takes much longer, it leads to superior outcomes particularly in families where the issues are often multi-layered and therefore benefit from deeper discussion around interests. More broadly, the power-rights-interests construct is useful even without the (overt) presence of conflict. In particular, family members from the in power generation should be very wary of using their power with other adults in any context, and also be aware of the potential fallout from using rights to rule on issues. At the very least, a preliminary examination of interests (even as simple as asking five whys) can uncover the core issues that are at the heart of a matter.

| ||||

|

Horizons: Family Office & Investor Magazine

David Werdiger: Conflict Resolution in Wealthy Families |

|

{kind=link}