RSS

RSS|

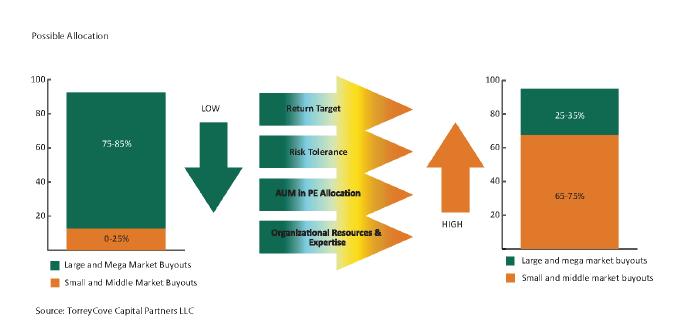

Mega funds are no longer the only place for LBOs, the middle market is packing a significant punch for investors. By: Bailey McCann Few vehicles in private equity carry with them as much folklore as leveraged buyout (LBO) funds. Popularized during Wall Street's go-go years in the 1980s, the leveraged buyout calls to mind visions of Gordon Gekko like bankers and East End Avenue addresses. Before the crash, some LBO funds amassed significant assets and deal track records, effectively becoming 'mega' funds, leading to some of the biggest deals in the industry. However, these funds started to decline even before 2008, as issues with leverage, paying too much and going after trophy deals regardless of quality dampened reputations and investor interest. In the small and mid-market, LBO funds have plugged along more steadily, spurred on by consistent activity within that market segment and an arguably more focused approach to deals. That said, like the markets they serve, small to mid-market funds have also seen more failures and a more challenging asset raising environment. For investors looking over these realities, and coming off tough crisis years, they may be left to wonder if the LBO arena is more trouble than it's worth. Research out this month shows that current market conditions may be more favorable for LBOs than they have been for some time. According to credit strategists Hans Mikkelson and Yuriy Shchuchinov at Bank of America Merrill Lynch, market conditions have become "unusually conductive for leveraging transactions for this stage in the typical cycle." This could spell the return of LBO funds, especially in the small to mid-market, according to data in the report. For investors trying to decide how to allocate to an LBO fund, there are a variety of factors to consider - especially given the dramatic changes in both the economic and regulatory environments post 2008. The Mega Fund Isn't Dead Yet As with other industries, size comes with a variety of benefits: name recognition; access to capital and talent to manage it; a track record with deals people know about; and reliability. Taken together, these factors tend to equate to an overall lower risk profile and investor trust resulting from the institutional grade infrastructure these firms offer. In the Bank of America Merrill Lynch report, the authors say that the current low yield environment, coupled with recapitalized banks and liquidity in the public markets could start pushing deal size above $10bn. New regulations require banks to stay below 6x leverage in their transactions, but the continuation of QE3 is likely to start pushing banks to lend, with the only real limitation on deal size being the equity size of the equation. The club deal may be hard to come by, but not impossible. China is on pace for its biggest ever leveraged buyout with four more banks coming on to finance the leveraged buyout of China's Focus Media Holding at $3.7 bn. In the report, strategists also note last year's acquisition of Synthes by Johnson and Johnson, post-deal filings show that at that time three private equity firms came together for a $20bn offer. However, the problem for mega funds or even big club deals, is the ability to create significant value. For deals that are of suitable size, they often involve brands that are organizationally entrenched, "the hardest part about buying a big brand is that the industry is often more mature, the management team has already taken care of the low hanging fruit, and the way the business works is well established. It can be very difficult to make real improvements," explains David Fann, President & CEO of TorreyCove Capital Partners in an interview with Opalesque. TorreyCove Capital Partners, a global alternative investments specialist, currently overseeing approximately $19.5 billion of private equity assets, recently released their own take on the LBO landscape. Fann and his firm advise a variety of public pension plans, and large institutions on private equity investing. Multiples Abound in the Middle Market For investors seeking LBOs that offer a higher multiple, the middle market may be the sweet spot right now. Always competitive, the middle market LBOs typically come with greater returns but also greater risk. The funds are smaller, and according to TorreyCove, working with them requires as much due diligence as the deal itself.

For investors seeking greater deal activity, and the opportunity to make real capital improvements, the high-touch relationships that come with these firms are likely to make them more appealing. Middle market firms also tend to have more strategic discipline than their larger counterparts. Many of the mega firms operate under public scrutiny and take more diversified approaches in order to bring in assets on a more consistent basis even if those assets are not directly aligned with all investment interests. "There is always going to be a greater blowup risk with these funds and smaller funds, by definition," Fann notes. "But, there are benefits too - people are hungrier, they work harder. Investors simply have to do their research and keep their eyes open." The relative newness of a given investor's interest in LBOs may also come into play, writing in the article, authors for TorreyCove note that, "the higher dispersion of returns within the small and middle market buyout spaces, combined with the much larger number of managers operating in those spaces, means that institutions desiring substantial exposure in the lower end of the market must possess strong organizational resources and expertise. If these factors are in place, it follows that such organizations would be better served by a substantial bias toward the middle/small portion of the buyout sector." However, if a program is relatively new, it may be better served with a larger, more established fund, trading away some of that multiple for organizational consistency. Fann explains that weighing these issues is especially important for large public institutions given today's return starved environment. "If you look at the next five years, or even if you look retrospectively, private equity has been an outperforming asset class for large institutions, especially pension funds. The only way pension funds can meet that 8% return requirement is to do more investing in alternatives. Private equity is one area where those returns can be achieved and sustained." | |

|

This article was published in Opalesque's Private Equity Strategies our monthly research update on the global private equity landscape including all sectors and market caps.

|

Private Equity Strategies

The Revival of the Leveraged Buyout Fund, Strategic and Tactical Implications For Portfolios |

|

{kind=link}