Small Managers - BIG ALPHA Episode 20

Tuesday April 21st 11 am ET (4pm GMT, 5pm CET, 6pm Riyadh, 7pm Dubai, 8:30pm Delhi)

Identifying uncorrelated, alpha-generating strategies in today's market is no small feat: Niche, alpha-focused strategies with institutional backing are rare. This investor workshop connects you with proven managers:

This investor workshop features quality managers:

Ironshield’s Market-Neutral Credit fund generated positive returns both during the Iran war* and across strong market in the previous quarters.

With HY credit dispersion at a 13-year high, the days of "a rising tide lifting all boats" are over. For credit specialists who can distinguish winners from losers, this is a perfect environment.

Firm Background, Fund Structure & Returns

Ironshield Capital Management LLP is a London-based credit specialist founded in 2007, managing long/short high yield credit portfolios across market cycles.

Fund: Ironshield High Yield Alpha Fund UCITs

Portfolio Manager: Frits Lieuw-Kie-Song

Launch date: August 2022

Aim: Target 6-7% net a year in Euro over the cycle while maintaining Market Neutral exposure

Structure: Daily liquidity, Irish domiciled UCITs

Approach of the fund is straightforward in concept but demanding in execution. The fund is structured as follows:

- Long exposure consists of: individual bonds which are fundamentally mispriced.

- Short exposure consists of: individual bonds which are fundamentally mispriced

- High Yield indices

- Equity indices (including put spreads)

The fund hedges out all foreign exchange risk and has minimal duration exposure. Although the fund can invest globally, most of its exposure is in Western Europe and the USA.

The return is +13.33% net since inception with an annualised volatility of 1.88%, less than half the volatility of the Bloomberg Pan-European and US High Yield indices. Beta to EU HY of 0.21 and US HY of 0.13, and a Sortino ratio of 3.73 since inception.

Since Frits’ appointment during the summer of 2025, performance has annualized at 6.41% (net in euro) with continued low volatility. Frits brings decades of experience of managing similar strategies, navigating credit through multiple market dislocations, including the LTCM crisis, the Global Financial Crisis, and post-9/11 markets to name but a few. This experience underpins a disciplined, repeatable and scalable investment process designed to exploit mispricing across cycles particularly when dispersion is elevated.

The fund has been recognised for this approach, winning the HedgeWeek European Emerging Performance of the Year Award 2025.

Current market opportunity:

The investment thesis for 2026 is arguably more compelling than at any point since launch. Stressed sectors such as chemicals, autos, and software are generating short opportunities, while also throwing out mispriced longs in the panic. The different speed of adoption of AI among companies will create winners and losers within sectors. The explosive growth of AI-related high yield issuance (from zero in 2024 and expected to reach $60-80bn in 2026) is creating a new frontier of structurally mispriced bonds on both sides of the book.

Frits’ experience in managing similar portfolios through numerous crises is invaluable and enables the team to rely on a proven, battle-tested investment process.

Strategy Highlights

- Market-neutral: Target 6-7% net a year in euro over the cycle while maintaining market neutral exposure. Beta to EU HY of 0.21 and US HY of 0.13 since inception

- Expected return breakdown: ~70-75% from carry. 25-30% from capital gains.

- Sophisticated hedging toolkit: CDS indices, Equity indices, Equity index options (tail hedge), Bund/BOBL/SX5E futures - hedging contributed positively during 2022 and the April 2024 stress

- Diversified, liquid portfolio: 50–60-line items; bonds, CDS, TRS, and interest rate derivatives; daily liquidity, no gates or lock-ups; modified duration of just 1.2

- UCITS-compliant, institutional infrastructure: Irish domicile; administrator and custodian Northern Trust; auditor KPMG; managed on the MontLake UCITS Platform ICAV; FCA-authorised investment manager; scalable to €1bn+

- Award-winning track record: HedgeWeek European awards - Emerging Performance of the Year: UCITS - Credit Year 2025 winner

Investment Team

- David Nazar - Founder & CIO: 30 years in credit markets; prior to founding Ironshield in 2007, managed proprietary credit portfolios at Deutsche Bank and Bank of America; career spans Goldman Sachs, Salomon Brothers, BAML and Deutsche Bank; specialist in stressed and distressed European credit

- Frits Lieuw-Kie-Song - Portfolio Manager: 30 years in global credit; spent 11 years at Allianz as Portfolio Manager across Global High Yield and multi-asset funds; previously managed very similar strategies at various hedge funds for ~15 years.

- Sunny Chhabra - Senior Analyst & Partner: 17 years in stressed and distressed European credit; 11 years prior experience at Nomura

- Ishar Sawhney - Senior Analyst: 15 years as US credit specialist; prior roles at Goldman Sachs, Citadel, and Neuberger Berman; CLO experience

- Bledion Sasa - Senior Analyst: 11 years in stressed and distressed European credit; previously at Taconic Capital Advisors, Barclays, and Jefferies

- Average team experience exceeds 20 years; 7 nationalities represented across the business; leadership team average 25+ years

*as of publication date of 20th March 2026

AFC Asia Frontier Fund: The Alpha in the Blind Spot - +143% Since Inception While the Benchmark Returned +28%

Pakistan at 7.6x earnings. Bangladesh at 9.1x. Uzbekistan banks paying 13% dividend yields. These are not distressed assets - they are the fastest-growing economies on earth, systematically ignored by global capital. Asia Frontier Capital has been quietly compounding in this blind spot for 14 years.

Asia Frontier Capital (AFC) is a Hong Kong-based specialist investment manager focused exclusively on Asian frontier equity markets, established in 2013 through a management buyout from Leopard Capital. The firm manages four funds spanning the breadth of the Asian frontier universe, with a team of 10 investment professionals based on the ground across Hong Kong, Vietnam, Uzbekistan, Thailand, and Iraq. The flagship AFC Asia Frontier Fund , launched 30 March 2012, has returned +142.9% since inception against +27.5% for the MSCI Frontier Markets Asia Net Total Return USD Index over the same period - a gap of more than 115 percentage points accumulated with an annualised volatility of 10.3%, lower than the MSCI World, MSCI Frontier Markets, and MSCI Emerging Markets indices. The five-year annualised return stands at +11.6% with a Sharpe ratio of 0.83 and Sortino of 1.16. The fund returned +19.75% in 2025 and is up +6.1% YTD through February 2026. Current AUM is USD 26.4 million.

The investment universe spans 18 countries - Bangladesh, Cambodia, Georgia, Iraq, Jordan, Kazakhstan, Kyrgyzstan, Laos, Maldives, Mongolia, Myanmar, Oman, Pakistan, Papua New Guinea, Sri Lanka, Timor-Leste, Uzbekistan, and Vietnam - a combined GDP of USD 2.5 trillion and a population of 757 million, comparable in scale to India, yet virtually absent from institutional portfolios. These economies are growing at an IMF-projected average of 4.1% annually through 2030, faster than every major developed market region. Bangladesh is now the world's second-largest garment exporter. Vietnam's exports to the US have grown from USD 42bn to USD 120bn since 2017. Central Asia is emerging as a critical geoeconomic corridor. And the fund currently trades at a weighted average trailing P/E of just 6.98x - near its all-time low - with a portfolio dividend yield of 4.04% and a P/B of 1.32x, at a fraction of the multiples commanded by comparable emerging market names.

Strategy Highlights

- 14-year live track record, 515% outperformance vs benchmark: +142.9% since inception (USD-A, net of fees) vs +27.5% for MSCI Frontier Markets Asia; five-year annualised return +11.6%; +19.75% in 2025

- Low volatility, genuinely uncorrelated: 10.3% annualised volatility since inception - lower than MSCI World (13.7%), MSCI Frontier Markets (13.8%), and MSCI Emerging Markets (16.3%); correlation of 0.49 with MSCI World

- Historically cheap entry point: portfolio P/E at all-time low of 6.98x; P/B of 1.32x; dividend yield 4.04%; Pakistan trades at 7.6x vs India at 22.4x

- 62 holdings across 15+ markets: bottom-up stock selection from a universe of 3,000+ listings, screened to a focus list of 200; position sizing disciplined at max 5% at cost, top-sliced above 10%; annual turnover below 20% since inception

- On-the-ground research: 200+ company meetings annually; analysts resident in Vietnam, Uzbekistan, Iraq, Thailand, and Hong Kong; top-down country allocation drives currency and macro risk management

- Supply chain and geopolitical tailwinds: Vietnam, Bangladesh, Cambodia, and Pakistan among the primary beneficiaries of manufacturing diversification away from China; Central Asia gaining geoeconomic importance via the Trans-Caspian corridor

Investment Team

- Thomas Hugger - CEO and Fund Manager: 27 years in private banking; investing in Asian and African frontier markets since 1993; former Managing Partner, CFO and COO of Leopard Capital; former MD and Head of Portfolio Management at LGT Bank Hong Kong; founding shareholder of one of Bangladesh's largest brokerage firms; CFIA, Investment Adviser (Switzerland), EFFAS Financial Analyst

- Ruchir Desai, CFA - Co-Fund Manager: with AFC since inception; covers Bangladesh, Georgia, Jordan, Kazakhstan, Oman, Pakistan, Sri Lanka, and Vietnam; prior experience at HandsOn Ventures (Mumbai); MBA from CUHK Business School (exchange at Fuqua/Duke); CFA charterholder since 2015

- Roland Jossi, CFA - Deputy CEO: 40+ years in private banking, fund management, and insurance; senior management roles at leading Swiss banks in Japan, Hong Kong, and Singapore; CFA charterholder since 2001

- Ahmed Tabaqchali, Chief Strategist AFC Iraq Fund: 25+ years experiences in capital markets in US and MENA markets, currently covering the Iraqi market based in Iraq and London. Former Executive Director at NBK Capital. He has an M. Sc. in Mathematics from Oxford University

- Scott Osheroff - CIO, AFC Uzbekistan Fund: on-the-ground specialist in Central Asian frontier markets; resident in Tashkent and the region; with extensive experience in frontier markets in Asia in listed and private equity across Asian frontier markets

- Peter de Vries - Marketing Director: 25+ years in Hong Kong finance; former Director at Leopard Capital; prior roles at ViewTrade Securities and Merrill Lynch; MBA from Calstate Hayward; fluent in Dutch, English, and German

- Fund domicile: Cayman Islands | Custodian: DBS Hong Kong | Auditor: EY Hong Kong | Administrator: Trident Fund Services

Amfileon: Market-Neutral Statistical Arbitrage with Elite Quant Pedigree

When markets panic, most strategies struggle to stay flat. Amfileon accelerates.

Amfileon AG is a Munich-based quantitative investment manager founded in 2021 as a family office spin-off, with a mission to develop and operate cutting-edge market-neutral systematic investment strategies across global equity markets (US, Europe, Japan). The firm is built around a team of eight STEM PhDs and quantitative scientists with over 100 years of combined relevant experience - veterans of Millennium, Oxford Asset Management, Aspect Capital, Virtu Financial, Citigroup, Nomura, and Google DeepMind.

Since going live in October 2023, Amfileon has delivered 7.7% annualized returns with 4.9% volatility and a Sharpe ratio of 1.6 - results that stand out even more under the hood: with a beta of -0.03 and annualized alpha of 9%, the strategy is genuinely market-neutral. The maximum drawdown is just 4.9%, and the Sortino ratio of 2.7 reflects the asymmetric downside protection built into the design.

Perhaps most compelling is how the strategy performs when markets break: in high-volatility regimes (VIX above 21), the fund has delivered 23.6% annualized returns with a Sharpe ratio of 2.8 - the kind of crisis-alpha that transforms portfolio construction for serious allocators.

Strategy Highlights

- Genuine market neutrality: Beta of -0.03 to the S&P 500; zero directional equity exposure by design

- Crisis-alpha profile: Annualized return of 23.6% and Sharpe of 2.8 during high-VIX regimes (vs. 1.0% / 0.3 in low-volatility periods)

- Diversified and systematic: Eight active sub-strategies; 500-2,000 portfolio positions in liquid stocks; holding periods from one hour to five days

- Disciplined risk management: Max drawdown of 4.9% since inception; 4.9% annualized volatility

- Institutional-grade infrastructure: Live performance is reported net of all trading costs and before management fees; assets administered through Universal-Investment-Gesellschaft mbH

Investment Team

- Sebastian Helmensdorfer, PhD, CFA - Founder & Co-CEO; previously Partner at Europe's largest short volatility fund and CIO at Quants Vermoegensmanagement AG (family office); PhD in Mathematics, University of Warwick

- Thomas Trenner, PhD - Head of Research; previously Senior Quantitative Researcher at Oxford Asset Management, Citigroup and Nomura; PhD in Mathematics, University of Cambridge

- Markus Sauter, PhD - Head of Portfolio Management; previously Quantitative Researcher at Virtu Financial and Portfolio Manager at Principal Global Investors; PhD in Physics, University of Greenwich

- Andreas Denner, PhD - Head of Data; previously Quantitative Researcher at Aspect Capital; PhD in Mathematics, TU Munich

- Scientific Board includes Georg Ostrovski, PhD (Google DeepMind Reinforcement Learning Engineering Lead) and Prof. Joerg Osterrieder (University of Twente / Bern Business School; formerly Goldman Sachs, Merrill Lynch, AHL)

Althera42: Royalty Investing Comes to European Tech - Uncorrelated Income Streams from the IP Economy, Before the Window Closes

Royalty Pharma built a multi-billion dollar business buying pharmaceutical revenue streams. The same model is now being applied to Europe's EUR 1 trillion tech IP economy - and Althera42 is the first mover.

Althera42 is a London-based alternative investment platform with a mission to do for technology and software IP what Royalty Pharma did for healthcare: transform predictable recurring revenue streams into institutional-grade royalty assets. Founded in 2025 by Dr. Christian Czernich as a spin-off from Round2 Capital - the firm he built into Europe's leading revenue-based finance provider - Althera42 is raising its debut EUR 300m Royalty Tech Fund targeting EUR 1bn AUM within three to five years, with an indicative target net return above 15% and quarterly cash distributions to investors.

The strategy sits at a genuinely novel intersection: it is neither private equity (no reliance on exits or valuation multiples) nor traditional private credit (no fixed amortization schedules, no cash-flow mismatch). Instead, Althera42 purchases 5-10% of an IP-based technology company's recurring revenues via a true sale, receiving uncapped monthly royalty payments for periods of up to 25 years - while the existing business owners and equity investors retain full control, carry no additional balance-sheet debt, and can fully preserve their ownership stake without dilution. Returns have a very low market correlation, do not depend on timing an exit nor on entry or exit valuations and are naturally protected from inflation; the investment is self-liquidating by design, with multiple additional early optionality paths including securitization and secondary transactions at the fund level.

The opportunity is time-sensitive. Royalty investing is well-established in pharmaceuticals, metals and mining, and music with a yearly royalty investment volume of EUR 10 – 20bn in these sectors - but has not yet been deployed at scale in European IP-based tech despite over EUR 1 trillion in size and growing at 12-15% per year. Three structural barriers keep competition low: banks cannot use royalties within their regulatory frameworks; most credit funds lack the specialized underwriting skills required (revenue cohort analysis, billing system diligence, true-sale structuring); and business owners in tech are simply unfamiliar with the instrument. Althera42's founding team has spent the last decade in sourcing, structuring and executing 40 royalty deals across Europe with 13 exits and an average realized exit IRR >20%.

Strategy Highlights

- A genuinely new asset class: Contractual participation rights in future revenues - uncapped upside, IP-backed downside protection, no equity valuation risk, no exit dependency, natural hedge against inflation and isolation from interest rate fluctuations; indicative target net returns above 15%, 1.75 – 2x MOIC with quarterly cash distributions

- Structural protection superior to traditional credit: True-sale royalty purchases do not appear as debt on the borrower's balance sheet; royalty claims typically senior to creditor claims in insolvency; payments scale with revenues, eliminating the cash-flow mismatch that triggers most loan defaults

- EUR 500-600bn investable pool, minimal competition: Over EUR 1 trillion in IP-based tech recurring revenues; systemic inertia, capability gaps, and borrower unfamiliarity keep institutional competitors out - for now

- Clearly defined target market: Cash-profitable European and US mid-market B2B technology companies with defendable IP, EUR 10-100m revenues, gross margins above 50%, churn below 10%, and consistent growth above 10%; tickets of EUR 5-25m per company

- Six target sectors in digital infrastructure and tech-enabled services: Cloud and compute, connectivity and networks, platforms and applications, data infrastructure, cybersecurity and defense, and payments and digital transactions

- AI-native operations: Fund operations powered by proprietary data-driven tooling and industry partnerships; origination via pan-European networks built over a decade of royalty deal-making

- Comprehensive legal protection: Collateral package on a case-by-case basis with the following building blocks: Receivables pledges, IP and all-asset pledges, covenants with step-in and step-up rights, 90-180 day rolling royalty reserves, board and observer seats, monthly revenue reporting tied directly to billing systems.

You will be able to tune in to this webinar from any computer, tablet, or smartphone. The webinar will be recorded - in case you are not able to join, all registered participants will be provided a link to replay the webinar.

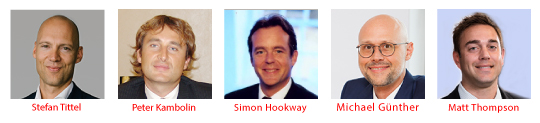

Frits Lieuw-Kie-Song

Ruchir Desai, CFA,

Dr. Sebastian Helmensdorfer, CFA,

Dr. Christian Czernich

PAST WEBINARS

Small Managers - BIG ALPHA Episode 19

"Superb panel with great presentations, excellent job from all managers. Thank you very much!" (MT)

"Thank you -- thought provoking." (DH)

"Thank you. Was excellent!" (GC)

"Very well done!" (RB)

"Great session!" (MP)

"Nicely done" (CC)

"Well done, thank you!" (AS)

Thursday February 12th 2025

Identifying uncorrelated, alpha-generating strategies in today's market is no small feat: Niche, alpha-focused strategies with institutional backing are rare. This investor workshop connects you with proven managers:

This investor workshop features quality managers:

Katch Investment Group: European Value-Add Real Estate Equity

Katch Investment Group, founded in 2017, is a global alternative asset manager investing across Europe and select international markets with approximately $1.5bn AUM.

Katch’s European value-add real estate private equity strategy focuses on sourcing and executing high-conviction investments where returns are primarily driven by business plan delivery rather than market appreciation. Since inception, the strategy has executed projects totalling €317m of gross development value (GDV), with realised outcomes demonstrating 20%+ IRRs. Investment performance is supported by conservative leverage, tight governance, and multiple exit routes (HNW sales, forward funding, and institutional disposals), providing flexibility and liquidity through market cycles.

Strategy Highlights

- Proven Execution Track Record: Executed €317m GDV across France, Spain and the UK, with realised investments demonstrating 20%+ IRRs through disciplined business plan delivery

- Institutional Deal Focus: Targeting resilient, supply-constrained markets with deep liquidity and institutional exit optionality where demand fundamentals and structural barriers to new supply support pricing power

- Scaled Proprietary Origination: €610m+ pipeline sourced through off-market channels and repeat relationships, enabling disciplined entry pricing and strong structuring

- Equity-Led, Control-Oriented Structuring: Majority or co-GP equity investments, with governance rights, alignment, and flexibility across the capital stack

- Active Asset Management & Governance: Investment committee process, asset-level oversight, and hands-on execution from acquisition through delivery and exit

- Institutional infrastructure: AIFM Luxembourg: Funds Avenue (Trustmoore Group), Fund administrator: Bolder services, Audit & NAV Fund services administration: Mazars Forvis.

Tabor Asset Management: Low net, market-neutral equity long/short

Tabor Asset Management, founded in New York in 2018, executes an equity long/short strategy focusing on concentrated high-conviction opportunities in Consumer, Media, Internet, and Technology sectors. The firm specializes in low net, market-neutral investing with rigorous fundamental research and strict risk management, delivering alpha generation through deep industry expertise with a core focus on uncorrelated returns and capital preservation.

Tabor's disciplined investment strategy has delivered 81.5% net returns since inception (February 2019), maintaining disciplined position sizing with 3:1 reward/risk requirements for longs and generating most alpha from a diversified short book of 70+ positions.

Strategy Highlights

- Uncorrelated Returns, Consistent Performance: 0.26 correlation to S&P 500 with 7.8% beta-adjusted net exposure; 1.1 Net Sharpe Ratio; 81.5% cumulative returns since inception; 12.92% in 2024, 12.68% in 2023

- Concentrated, High-Conviction Portfolio: Approximately 30-40 longs and 60-70 shorts across 18 sub-sectors; 90%+ single-name short positions; strict 3:1 reward/risk requirement for long entry; top 5 longs represent 28% of exposure

- Alpha-Generating Short Book: Most ITD alpha generated from shorts through combination of alpha shorts (fundamental decline) and hedge shorts (relative underperformance); 90% in single names vs. 6-8% factor basket hedge

- Robust Three-Prong Risk Management: Individual position limits combined with sub-sector drawdown controls and portfolio-level gross reduction protocols

- Deep Sector Expertise: Specialized focus on Consumer/Leisure (57.2% ITD attribution), Internet (13.9% ITD), and Media sectors; team averages 18 years Wall Street experience; integrated buy-side and sell-side backgrounds

- Experienced Leadership: Jonathan Jacoby (CIO) with portfolio management experience at Millennium and UBS O'Connor

- Institutional Infrastructure: PwC audit; NAV Fund Services administration; IQ-EQ compliance; Prime Brokers: UBS, Jefferies; Legal Counsel: Kleinberg Kaplan (US), Mourant Ozannes (Offshore); Boosted.ai risk platform

Coromandel Capital: Asset-backed credit facilities to Specialty Finance and FinTech

Coromandel Capital LLC is a Los Angeles-based private credit manager founded in 2019, offering investors access to a diversified portfolio of performing assets in niche credit opportunities. The firm specializes in asset-backed credit facilities to Specialty Finance and FinTech companies, delivering consistent cash flows through conservative structuring with a core focus on principal protection.

Coromandel delivered 100% positive return quarters since inception, focusing on equity contribution by borrowers and excess spread of underlying assets, while achieving low volatility and correlation to other asset classes with floating rate pricing.

Strategy Highlights

- Uncorrelated Returns, Consistent Performance: -0.85 correlation to S&P 500 with 1.40% annualized volatility;100% positive return quarters; 13-16% net annual returns since 2020

- Diversified portfolio: Across consumer services, embedded financing, specialized finance, education/training services, and PropTech/logistics. Borrowing bases governed by strict eligibility criteria and restrictive covenants

- Proprietary deal flow: Driven by strategic relationships

- Principal Protection: Conservative structuring with borrower equity cushions and excess spread

- Quarterly Income: Regular cash flow distributions available to investors with average quarterly net yield distribution: 4.01%

- Experienced Team: Complementary skillsets from Credit Suisse, Morgan Stanley, Prosper, Moody's

- Institutional Backing: $125M anchor commitment; partnership with Origami Capital Partners

- Institutional Infrastructure: KPMG audit; Alter Domus administration; Compliance: Pine Advisor Solutions; Legal Counsel: McGuire Woods, Thompson Coburn; Banking: Security National Bank of Omaha

Please review this disclaimer for full information: https://coromandelcapital.com/disclaimer

S.R. Ocellus (Sloane Robinson): Global ex-U.S. long/short equities with an opportunistic macro focus

S.R. Ocellus is a global (ex-U.S. and Japan) long/short equity strategy managed at Sloane Robinson, a London-based investment firm founded in 1993 with a long heritage in global and macro-oriented investing. The strategy is led by Edward Lam, CIO and Portfolio Manager, who brings over 20 years of experience in emerging and international equities, including a decade as lead PM and Head of Research at Somerset Capital Management.

The Ocellus strategy applies a differentiated framework to global equities outside the U.S., with banks and financials often forming the core of portfolio positioning. The approach combines bottom-up fundamental analysis with top-down macro and capital-flow insights, seeking to exploit recurring banking and crisis-recovery cycles across geographies. Net exposure is actively managed and can vary significantly depending on opportunity set and risk conditions.

Since launch in January 2024, the fund has delivered strong performance. For full-year 2025, the strategy closed up 57.7% net in USD terms (unaudited), driven primarily by positions in global banks and financials rather than mega-cap U.S. technology stocks. The fund is primarily seeded by the principals, ensuring strong alignment, and benefits from Sloane Robinson’s institutional infrastructure, governance, and risk management framework.

Strategy highlights

- Conviction-driven, unconstrained mandate: Global ex-U.S. long/short equities with flexibility to pursue opportunities across regions and sectors

- Banks as a core alpha engine: Proprietary framework focused on banking cycles, capital flows, and crisis-recovery dynamics

- Strong recent performance: +57.7% net in 2025, achieved largely outside crowded AI and mega-cap tech trades

- Experienced leadership: Edward Lam with 20+ years in EM and global equities; supported by Hugh Sloane and George Robinson

- Aligned structure: Principals seeded the fund; institutional-grade operations, risk management, and governance

Canadian Farmland: The Original Inflation Hedge Delivering Double Digit Returns

"This is a brilliant webinar. Super theme and excellent manager. Thanks for showcasing Omnigence and its farmland thematic." (RH)

"Congratulation for another most interesting webinar." (CP)

"This is an incredible session with Will. Thank you so much!" (CW)

"Many thanks you Matthias and Will for a robust presentation." (BM)

"Will, great presentation!" (PH)

"Congratulations to a great product, great sector and great performance track record!" (WG)

Wednesday, January 28th 2026

An $800 billion real asset class hiding in plain sight - Canadian farmland secures the world’s food supply while delivering high, uncorrelated returns.

Webinar Description

In a world of persistent inflation, volatile markets, and fragile global supply chains, Canadian farmland stands out as a beacon of resilience. This real asset offers genuine inflation protection, high returns and low correlation to traditional markets - rooted in essential food production.

Join Omnigence Asset Management for an exclusive deep dive into Canadian farmland investing.

This webinar reveals how Omnigence Farmland’s TerraFIRST platform and quantitative framework capture productivity-adjusted pricing inefficiencies across 140,000 acres of Canadian farmland, enabling consistent alpha generation for nearly two decades.

Participants will learn:

- Market Structure: Overview of a ~$800B asset class with ~2% institutional ownership and $30B in annual liquidity.

- Macro Tailwinds: Population growth, dietary shifts, and climate impacts driving long-term agricultural demand.

- Valuation Gap: Why Canadian farmland trades 40–60% below major markets on a productivity-adjusted basis.

- Data-Driven Strategy: How Omnigence’s quantitative approach identifies pricing inefficiencies traditional buyers miss.

- AgTech Development: Use of satellite monitoring, proprietary AI and predictive analytics to enhance portfolio management.

- Track Record: Review of 18 years of consistent, inflation-beating returns through multiple cycles.

- Portfolio Allocation: How institutions deploy farmland to strengthen diversification and resilience.

Featured Speaker

Jonathan Planté – Head of Capital Formation, Omnigence Asset Management. Jonathan leads investor initiatives at Omnigence, a Canadian alternative investment firm with over C$1 billion in assets across real assets and private equity. He is a seasoned industry professional with 18+ years of experience designing investment solutions for institutional investors across alternative strategies.

Who Should Attend

- Institutional investors and asset allocators seeking inflation-hedged real assets

- Global family offices exploring agricultural investments

- RIAs and wealth managers serving ultra-high-net-worth (UHNW) clients

- Investment consultants evaluating alternative asset strategies

- Pension fund and endowment managers seeking ESG-aligned real asset investments

Mastering Manager Selection in Blockchain Venture

"Thank you for this amazing webinar, Matthias!" (CIO, single family office)

"Thank you -- thought provoking." (DH)

"Thank you. Was excellent!" (GC)

"Very well done!" (RB)

"Great session!" (MP)

"Nicely done" (CC)

"Well done, thank you!" (AS)

Wednesday, December 10th 2025

Applying Institutional Discipline to the Frontier of Blockchain Venture: Lessons from Europe's Largest Blockchain Venture Allocator

Duration: 60 minutes including Q&A

Overview

Hype is easy. Real success is rare. In blockchain venture, the gap between top-quartile and bottom-quartile managers isn't just wide—it's existential. With 200+ funds competing for capital and only a handful delivering sustainable returns, manager selection isn't just important. It's everything.

After six years and dozens of allocations, Theta Capital has learned what separates the fleeting from the enduring. This isn't about chasing narratives. It's about process, governance, rigorous research and institutional discipline applied to the frontier of innovation.

Blockchain venture has evolved from a niche opportunity to a structurally growing segment of global venture capital. As Europe’s largest blockchain venture allocator, Theta Capital Management has developed a research-driven, repeatable process to identify and build exposure to the most capable managers globally. Since 2018, through its Theta Blockchain Ventures strategy, Theta has constructed one of the broadest institutional portfolios in the sector, combining qualitative insight, quantitative analysis, and disciplined portfolio design to translate innovation into investable exposure.

This Opalesque Investor Workshop opens up that process: exploring how Theta sources, evaluates, and monitors managers in an emerging market where traditional frameworks often fall short.

Discussion Topics

- From Universe to Portfolio: As institutional capital enters digital assets, the challenge isn't finding managers. It's finding the right ones. How Theta tracks and filters more than 200 blockchain venture managers globally.

- Qualitative Assessment: The common characteristics of resilient and enduring venture managers.

- Institutional Oversight: Theory is cheap. Track records tell the truth. How governance, risk, and operational standards are applied in a frontier asset class.

- Portfolio Construction: Balancing diversification and conviction across strategies, stages, and ecosystems.

- Evolution of the Landscape: What six years of allocations reveal about how blockchain venture is maturing.

Why It Matters

Blockchain is entering an institutional phase, yet disciplined allocation remains the exception rather than the norm.

This session provides investors with a clear view of the decision-making, structure, and governance that underpin Theta’s long-term approach to the asset class. It illustrates how process, rather than prediction, has been central to building durable exposure to innovation at scale.

Speakers

Ruud Smets

Partner & Chief Investment Officer, Theta Capital Management B.V.

Will discuss Theta’s investment philosophy and how structural shifts in blockchain technology inform portfolio design.

Leopoldo Ochoa

Investment Associate, Theta Capital Management B.V.

Will discuss Theta’s manager research and due diligence process.

What You'll Walk Away With:

- A repeatable framework for evaluating blockchain venture managers

- The top 5 red flags Theta has learned to spot

- How to apply institutional governance without stifling innovation

- Portfolio construction principles for an emerging, high-dispersion asset class

Perfect For:

- Family offices exploring digital asset allocations

- Institutional investors building blockchain exposure

- Fund-of-funds managers evaluating the space

- Investment committees seeking due diligence frameworks

No Fluff Promise: This isn't a blockchain hype session. It's a practical workshop on manager selection discipline in a high-stakes, rapidly evolving market.

For professional investors only

Uncommon Ideas For Commoditized Markets: Alpha from Builders, not Prices

"Great webinar. Can you arrange a 1:1 call with Will?" (LC)

[more feedback]

"Congratulation for another most interesting webinar." (CP)

"This is an incredible session with Will. Thank you so much!" (CW)

"Many thanks you Matthias and Will for a robust presentation." (BM)

"Will, great presentation!" (PH)

"Congratulations to a great product, great sector and great performance track record!" (WG)

Thursday, November 20th 2025

While Silicon Valley captures headlines, a $1.5 trillion institutional underweight in real assets tells a different story with smart money quietly building positions where others fear to tread.

The world runs on electricity, is built from steel, and moves through railroads, airports, and shipping lanes. Yet most investors get burned trying to time commodity cycles, missing the real source of returns: the operators and builders who create value regardless of where oil or copper trades.

Join William Thomson, Founder and Managing Partner of Massif Capital, for an exclusive Opalesque Investor Workshop that reveals why the next decade's best returns won't come from predicting commodity prices—they'll come from identifying superior execution in energy, materials, infrastructure, and industrial equities.

What You'll Learn:

- The Three Macro Shifts: Creating a Generational Opportunity Discover how volatile inflation, regionalization, and structural scarcity are permanently reshaping cost curves and competitive dynamics across real asset sectors

- Why Conventional Wisdom Fails in Cyclical Industries: See the data proving that commodity prices explain less than 50% of equity returns in these sectors—and what actually drives the other 50%

- The Massif Capital Framework for Evaluating Management: Get Will's proprietary system for assessing capital allocation, operational excellence, and execution in commodity businesses—the same framework we use to generate uncorrelated returns

- How to Balance Environmental and Economic Concerns: Learn practical strategies for building portfolios that capture the energy transition opportunity while maintaining discipline on returns

Who Should Attend:

Institutional allocators, family offices, and sophisticated investors seeking differentiated alpha in an increasingly correlated market. This session is especially valuable for those who recognize the strategic importance of real assets but may have been burned by commodity volatility in the past.

About the Speaker:

William Thomson leads Massif Capital, a specialist investment firm focused on Basic Materials, Energy, and Industrial businesses. By decomposing equity return drivers and focusing on operational excellence over price speculation, Massif has built a unique track record of uncorrelated, long-term capital appreciation in sectors most investors avoid.

Key Takeaway:

Alpha in commodity producer equities doesn't come from calling the tape—it accrues to investors with a superior process for underwriting execution and management. This workshop provides that process.

How to Panic: The Science of Building Unbreakable Portfolio Protection

"Excellent presentation from Dan" (AF)

[more feedback]

"Thank you -- thought provoking." (DH)

"Thank you. Was excellent!" (GC)

"Very well done!" (RB)

"Great session!" (MP)

"Nicely done" (CC)

"Well done, thank you!" (AS)

Thursday, October 23rd 2025

A Live Webinar for Sophisticated Investors

What Makes a Protective Strategy Actually Work When Markets Break?

That's the Million-Dollar question every investor should ask.

When markets crashed on "Liberation Day" 2025, most "protective" strategies failed spectacularly. Why?

Because they weren't built to handle what actually happens when markets panic—they were built for textbook scenarios that never occur.

Join us for an eye-opening webinar that challenges everything you think you know about portfolio protection and reveals why most defensive strategies fail precisely when you need them most.

What You'll Discover

- The Physics of Market Panic

- Market shocks are inevitable. The real question isn't *if* they will happen, but how your portfolio will react

- Watch a fascinating demonstration of how markets transform from self-stabilizing systems into chaos machines—and learn to recognize the warning signs before others even notice the shift.

Why Your Current Protection Is Probably Useless

Most "protective" strategies are merely trend-following in disguise. Discover why they catastrophically failed during the 2025 Liberation Day crash and the 2023 fixed-income reversal—and what actually worked.

The Three Non-Negotiable Elements of Real Protection

Learn the counterintuitive framework that separates strategies that actually protect from those that merely promise to:

- Liquidity When Others Have None: The graveyard of portable alpha strategies teaches us: If it takes 3 months to access your protection, it's not protection—it's decoration.

- The Power of Negative Correlation: While everyone chases uncorrelated assets, discover why negative correlation is the portfolio allocator's secret weapon—and how even modest returns can outperform high-Sharpe strategies when properly deployed.

- Volatility as Your Friend (Yes, Really): High volatility in protection isn't a bug—it's a feature. Learn how to harness volatility as "negative risk" that actually strengthens your portfolio when properly structured.

Who should attend? This investor workshop is designed for:

- Family offices managing concentrated wealth

- Institutional investors seeking robust risk management

- Portfolio managers tired of protection that fails when needed

- Sophisticated private investors with significant allocations to illiquid assets

Note: This session assumes advanced knowledge of portfolio construction and risk management.

Your Speaker: Dan Gelernter recently presented "How to Panic" to a standing-room-only audience in Chicago, demonstrating how markets transition from mean-reverting to trending regimes—and why most protective strategies can't handle the switch.

Drawing from his white paper on negative correlation dynamics and real-world experience managing through multiple market crises, Dan will share insights that challenge conventional wisdom about portfolio protection.

What Makes This Different

This isn't another webinar about diversification or stop-losses. Using live demonstrations and real crisis data, you'll see:

- Video demonstration: How shifting weight transforms stability into chaos (and what this means for your portfolio)

- Case studies: Detailed analysis of protection failures during Liberation Day 2025 and the 2023 bond reversal

- Mathematical proof: Why negative correlation beats high Sharpe ratios for portfolio protection

- Action framework: How to audit your current protection and identify fatal flaws

Key Takeaways

- A clear framework for evaluating any protective strategy

- Understanding of why private equity/credit heavy portfolios face unique liquidity crises

- The ability to distinguish real protection from expensive insurance theater

- Specific metrics for measuring protection effectiveness before you need it

The Bottom Line

In a world where a single tweet can trigger a market meltdown and "safe" bonds can crash 20% in weeks, yesterday's protection strategies are today's portfolio land mines.

This webinar reveals what actually works when markets break—not in theory, but in practice.

Register Now Here

Date: October 23rd Time: 11 am ET (4pm GMT, 5pm CET, 6pm Riyadh, 7pm Dubai, 8:30pm Delhi)

Duration: 60 minutes incl. Q&A

Format: Live interactive webinar with replay available to registrants

Investment: Complimentary for qualified investors

Space limited to ensure interactive discussion. Priority given to institutional allocators.

Can't attend live? Register anyway to receive:

- Full recording of the session

- Downloadable framework for evaluating protective strategies

- Executive summary of key insights

- Invitation to follow-up discussion

Final Thought

"The time to repair the roof is when the sun is shining." – John F. Kennedy

Markets feel invincible today. They won't tomorrow. The question isn't whether you'll face another crisis—it's whether your protection will work when you do.

Don't wait for the next panic to discover your protection is an illusion.

This webinar contains advanced concepts and is intended for sophisticated investors only. Past performance of any strategy discussed does not guarantee future results.

Small Managers - BIG ALPHA: How Life Settlements Turn Illiquidity into Alpha

"Thanks for this session packed with practical strategies and tactics, super useful!" (AJ)

"Great webinar Matthias" (JT)

"Very informative...many thanks." (DW)

"Spot on! A good deck literally helped us to increase AUM by ca. 60% since Jan!" (AS)

Thursday, October 9th 2025

Making money when others can't: How and Why Life Settlements found their way into institutional portfolios

When "alternatives" start moving with everything else, they aren't really alternatives anymore. If your "alternatives" depend on the same drivers as equities and credit, you may be paying alternative fees for mainstream risk.

Life Settlements can offer an attractive mix of risk, return and non-correlation. Following a conservative approach, the Laureola Investment Feeder Fund delivered annual compounded return of 10.19% and a Sharpe ratio of 1.62 over the past 12 years. The strategy also displays strong ESG characteristics along with the potential for asset/liability matching.

The best feature of the asset class is the genuine non-correlation with stocks, bonds, real estate, or hedge funds. Life Settlement investors will make money when others can't, and in this new Opalesque DEEP DIVE webinar format we examine how:

Life Settlements is an asset class with great promise: the genuinely non-correlated returns and attractive risk return profile are a rare combination. But in order to deliver the alpha and the diversification that investors seek, the successful manager must be prepared to do extensive research on every single investment; there can be several hundred investments in a portfolio. The most important assumption in the investment decision is the assumed life expectancy of the insured; managing the longevity risk in each investment is the primary responsibility of the asset manager and it is this responsibility that requires the “Deep Dive”. It should not be outsourced, as the life expectancy estimates provided by the life settlement under writers have proven to be unreliable.

Tony Bremness is the Founding Partner and CIO of Laureola Advisors, a specialist Investment Advisory Firm dedicated to managing Life Settlement assets exclusively. Tony has over 35 years' experience in investment management, with over 15 years in Life Settlements. Tony founded Laureola in 2012; the firm has been managing Life Settlement portfolios since 2013. The Laureola team has grown to 11 professionals with over 200 years of relevant experience.

Tony will discuss:

- Why Institutions should consider Closed End Funds only for this asset class

- Using macro trends to help manage risk and generate Alpha

- Turning the opaque and illiquid nature of the asset class to investors’ advantage

- Why internal underwriting is essential

Tony has a Master of Business Administration degree from McGill University in Canada and has been awarded the CFA designation

Khadija Benlhassan, PhD is a biotechnology executive and entrepreneur with 20 years' experience in preclinical and clinical research and development. Currently Expert for European Community, founding director of Voynich Biosciences Inc, Chief scientific officer of Wellness Group Intl SA and part of scientific advisory board of Laureola Advisors Inc. Dr Benlhassan worked in the past for ImmunoClin Corporation (IMCL) and for Biopharm Centre of Excellence in Drug Discovery at GlaxoSmithKline R&D, UK. She holds a PhD in Immunology from Paris Descartes University and has extensive R&D experience in drug development for international biotech and pharmaceutical companies.

Khadija will discuss:

- Trends in Cancer Research – where have the improvements been concentrated?

- Future Developments

- A recent example of her work at Laureola

Why Most Hedge Funds Fail at Shorting — And Steamboat Doesn’t

"Thank you Parsa - interesting and good for LPs to hear and understand. Thank you Matthias as well!" (MB)

[more feedback]

"Thank you. This was excellent." (JL)

"Cool call today - please share their material." (HM)

"Great job Parsa and Matthias!" (SS)

"Thank you very much - well done and organized." (SP)

"Very Insightful - liked the webinar !¤æŹ" (AK)

"Thank you - this was well done." (BS)

Tuesday, September 9th 2025

Most hedge funds lose money on short selling—diluting returns, increasing volatility, or failing to capitalize on overvalued stocks. Yet Steamboat Capital Partners has consistently generated alpha from its short book, turning a typically losing strategy into a key driver of outperformance and proving that well-researched short positions can still deliver alpha.

Unlike most hedge funds that use shorts merely as portfolio hedges, Steamboat treats short-selling as a distinct alpha-generation strategy—with a 12+ year track record to prove it works.

In this exclusive Investor Workshop, Parsa Kiai (Founder & CIO) and Farhad Dalvi (Director of Research) will sharing key insights:

- Why shorting is typically a losing game — and how Steamboat turns it into a profitable one

- A look back at Steamboat’s March 2025 short list — where 3 of 4 highlighted names fell by 27%, 50%, and 90% - and where Steamboat sees current opportunities

- Steamboat’s rigorous short selection process, including real-world case studies

- How Steamboat’s approach complements long alpha while limiting downside volatility

- Risk management techniques that allow for conviction without excessive exposure

- Why 2025 presents unique short opportunities amid stretched valuations and macroeconomic uncertainty.

Why Attend?

- Learn from a fund that has profited from shorts while peers struggle

- Discover actionable insights on spotting overvalued stocks and flawed business models

- See how Steamboat’s event-driven, catalyst-based approach differs from generic short-selling

Who Should Attend?

- Investors, Consultants, Analysts evaluating hedge fund allocations

- Portfolio managers interested in short-selling strategies

- Anyone skeptical about short selling’s role in a winning hedge fund strategy

Multi-Manager Investing 2.0: How Lucidity Capital reinvented the model

"Very impressive!" (RV)

[more feedback]

"You always bring great guests!" (AM)

"Thank you for hosting! Learned so much." (GG)

"Very informative" (JM)

"Thanks for your time, Tom." (JL)

"Please connect with us." (RA)

"Please visit us in Geneva." (AM)

Tuesday, July 08th 2025

In a market distinguished by uncertainty, where volatility lurks behind every geopolitical directive or incident, it is important to know what you have in your portfolio, to know that you have the facility to move out of the way, and to be confident that you control your own destiny.

Join Thomas Zucosky, Founder & CIO of Lucidity Capital Partners, for a deep dive into the next evolution of multi-manager investing—where transparency, liquidity, and real-time control replace the inefficiencies of traditional hedge fund structures.

The traditional multi-manager hedge fund model is broken. Investors face opaque commingled vehicles, lock-ups, and limited oversight—while paying excessive fees for middling results.

Lucidity Capital Partners has upgraded the approach by re-engineering the best elements of multi-manager investing with cutting-edge technology and a disciplined risk framework.

In this webinar, Lucidity’s Founder & CIO Thomas Zucosky will reveal:

- Why Multi-Manager 2.0 Outperforms the Old Model

- Transparency: Every position is visible real time—no black boxes

- Liquidity: Monthly redemptions, no gates, and 95% of positions liquid within a day

- Control: Dynamic risk management at the portfolio level, with the ability to adjust exposures in real time

- Investing with "Pod Leaders": Tom’s team recruits veteran PMs with deep sector expertise and integrates them into a diversified, low-net portfolio

- The Flaws of Traditional Multi-Manager Funds

- Commingled vehicles hide underlying risks

- Capital is trapped due to gates, side pockets, and quarterly redemptions

- Investors pay Pass Through fees for bloated overhead and opaque strategies

- Lucidity’s Edge: The SMA Advantage

- Direct ownership: Assets can be held in the investor’s name, eliminating counterparty risk. Unlike commingled funds, SMAs let investors see and control every position.

- Cost efficiency: Attractive pricing with traders through SMAs – no management fees

- Flexibility: Customized allocations (min. $10M) or use the core "ORCA" portfolio

- Results That Speak for Themselves

- Attractive risk adjusted statistics – 2.6 Sharpe ratio/ 6.6 Sortino ratio (Model Portfolio since 2020) (*)

- Low correlation to markets due to inventive portfolio construction around niche strategies (i.e. AI quant, crypto long/short, sector strategies)

Multi-Manager 2.0 =means no compromises for investors.

While investors trapped in traditional multi manager set ups pay pass through fees, accept illiquidity, and hope for the best, Lucidity offers daily transparency, total liquidity, and dynamic risk controls.

Who Should Attend?

- Institutions and family offices tired of traditional hedge funds’ lack of transparency

- Allocators seeking true liquidity and control over their hedge fund exposure

- Investors interested in uncorrelated niche strategies—without the lock-ups

Register now to learn how Lucidity is rewriting the rules of multi-manager investing.

(*)Disclaimer: Past performance is not indicative of future results. For qualified, eligible investors only. See Lucidity’s tear sheet for full disclosures.*

Small Managers - BIG ALPHA Episode 17

"Fantastic, very insightful and organized. Appreciate the work to create this for us." (SK)

[more feedback]

"Brilliant webinar!" (AK)

"Great session!!!" (LC)

"A big thanks to everyone!" (AO)

"Merci!" (GM)

Tuesday June 10th 2025

Finding differentiated, high-conviction strategies is increasingly difficult. This investor workshop offers a rare opportunity to discover quality managers:

1. Kris Sidial from The Ambrus Group: Carry-neutral tail risk strategy to protect portfolios without the bleed

Unlike traditional approaches that bleed investor capital during normal market conditions, Ambrus has developed an innovative, carry-neutral model that aims to provide robust protection against market crashes without depleting capital in the interim.

2. Jerome Callut from DCM Systematic: Scientific methods and AI power outperforming "Non-Trend" CTA strategy

Unlike conventional CTAs that may cluster around similar trend-following signals, DCM has developed a multi-strategy architecture that captures alpha through behavioral, relative value, and macro approaches, providing genuine diversification for institutional portfolios.

3. Elias Nechachby, CFA from MoSAIQ: A New Paradigm in Quant Investing

Developed by aerospace engineer-turned-quant Elias Nechachby, MoSAIQ is a groundbreaking investment framework that combines machine learning, genetic algorithms, and behavioral finance to deliver asymmetric returns with disciplined risk control.

4. Evgeny Gokhberg from Re7 Capital: Market-neutral, double-digit Web3 strategy

Re7 is a research-driven digital asset investment firm and has excelled as an operator, builder and a strategic allocator across multiple blockchain ecosystems, strategies and instruments. Starting in 2016, Re7 Capital's founders have operated in the digital assets space through three full cycles. Such multi-cycle experience creates deep understanding of market mechanics and ability to distinguish signal from noise.

Digital Health: How to invest early in a trillion dollar opportunity

"Great event, thanks so much. Dave is a superstar!" (JB)

[more feedback]

"Very impressed! Makes sense." (AK)

"EXCELLENT!!!" (JP)

"Well done Dave. Thank you!" (EP)

Thursday, May 15th 2025

An Investor Workshop with Dave Vreeland, Senior Managing Partner, Caduceus Capital Partners and veteran investor Adi Divgi.

The $5 trillion / year U.S. healthcare system is on the brink of collapse, but a new, tech-driven model is emerging.

Join us as we’ll reveal how the inevitable transformation of America's largest industry will create exceptional wealth-building opportunities through early-stage digital health investments, even amid broader economic volatility.

Boosted by advanced technologies such as: artificial intelligence, wireless electricity and robotics, a better, stronger, more consumer-oriented and less hospital-dependent system is already on the horizon. And you can participate already now.

What You'll Learn:

- The Unsustainable Status Quo: Why the hospital-dependent U.S. healthcare system is mathematically certain to transform in the coming decade

- Macro-Economic & Demographic Catalysts: Aging populations, cost pressures, and consumer demands are accelerating healthcare's digital revolution

- Technology Transformation Vectors: The key roles artificial intelligence, wireless technologies, and robotics in healthcare's reinvention

- Investment Opportunity Mapping: Which segments of digital health offer the highest growth potential and how to evaluate them

- Early-Stage Investment Strategies: Practical approaches for family offices to access high-potential digital health opportunities with managed risk

- Portfolio Construction Principles: How to balance digital health investments within your broader investment strategy

- Real-World Success Cases: Examining breakthrough companies that illustrate the transformational potential and investment returns in this space

- Due Diligence Framework: Essential questions to ask when evaluating digital health investment opportunities

Small Managers - BIG ALPHA Episode 16

It was excellent and thank you! (MR)

Thank you very much, great presentation! (AO)

Thanks a lot! Very interesting. :-) (JS)

Thursday April 3rd 2025

Energy Investing: Tall Trees Capital Management

Having generated over $500 million in P&L managing $1.2 billion in energy investments at Discovery Capital and now as Founder and CIO of Tall Trees Capital Management, veteran investor Lisa Audet is one of the leading experts globally on energy transition – one of today’s most significant investment opportunities.

Drawing from her remarkable 15+ year track record in energy investing and unique experience building businesses in emerging markets, Lisa will reveal:

- Why common approaches to energy transition investing may be missing the biggest opportunities

- Four exciting investment themes that are reshaping the energy landscape: Electrification, Nuclear, Copper, and Data Center Infrastructure

- How her team at Tall Trees Capital identifies “non-obvious opportunities” in this $25 trillion market

- Why certain popular clean energy sectors might actually present better short opportunities

- Strategic insights on portfolio construction and risk management that have driven her market-beating performance.

Zenith Alpha Management: A New Standard in Multi-Manager Investing

Zenith Alpha Management Ltd (ZAM) is redefining the multi-manager investment landscape with a cost-efficient, high-conviction approach to fund selection. Structured as a low-cost, open-ended multi-manager strategy, ZAM offers investors access to a curated selection of 6-8 elite fund managers, each with a proven track record in global equity markets.

Unlike traditional fund-of-funds models, ZAM eliminates the double-layer of fees (and all management fees at the fund and manager level), aligning investor and manager interests through a single performance fee structure—only payable when returns exceed an ambitious 11% hurdle rate. With a directional equity focus complemented by targeted hedging, ZAM provides diversified, actively managed exposure to top-tier strategies while mitigating risk and maintaining a cost-effective and performance-driven framework.

Backed by industry veterans and advised by UK based Sorengo Partners, ZAM prioritizes manager selection, transparency and alignment to deliver consistent, long-term returns above global equity benchmarks. Designed for sophisticated investors, ZAM is structured for tax efficiency and optimized capital deployment.

Oraclum Capital: Harnessing the Wisdom of Crowds to Predict Market Moves

With a proven track record of predicting major geopolitical events like Brexit, the 2016 U.S. election, and the 2020 Biden victory—all within 1% accuracy—Oraclum Capital has emerged as a leader in leveraging the wisdom of crowds and advanced network analysis to predict financial markets. Oraclum Capital applies this groundbreaking methodology in an uncorrelated, benchmark-beating options strategy.

Led by Vuk Vuković, PhD, a seasoned expert in political economy and network theory, Oraclum Capital has developed a proprietary Bayesian Adjusted Social Network (BASON®) Survey that combines crowd-sourced predictions with sophisticated network analysis to eliminate echo chamber biases and identify high-probability market moves. This scientific innovation has been successfully applied to predict weekly S&P 500 movements, achieving an impressive 64% accuracy rate over the past three years.

Hear Vuk Vuković speak about:

- The science behind crowd wisdom and network analysis, and how it predicts the market direction with remarkable precision

- Insights of integrating this strategy - with -0.02 Correlation to the S&P 500 and a Sharpe Ratio of 2.07 - into any portfolio seeking diversification and consistent alpha generation

- Key risk management practices that ensure disciplined exposure and safeguard against market volatility.

TradeFlow Capital Management: Transforming Trade Finance into an Investable Asset Class

TradeFlow Capital Management is a pioneering firm revolutionizing global trade finance by transforming SME import/export commodity risks into investment-grade products for banks and investors. Over the past seven years, TradeFlow has successfully invested in over US$3.5 billion of physical commodity trade across 18+ countries and 35+ commodities, executing more than 3,500 transactions – with zero (0) defaults.

Unlike traditional lenders, TradeFlow takes a non-credit, non-lending approach, directly owning commodities during shipment or storage to bridge the global trade finance gap. This asset-backed, over-collateralized strategy mitigates risk while ensuring short-dated liquidity.

Investors can access TradeFlow’s unique model through both Traditional Finance (TradFi) and Decentralized Finance (DeFi) products, including equity investments, Euroclear-listed notes, and innovative stablecoin-denominated debt instruments. Offering attractive, low-correlation returns with an investment-grade rating, TradeFlow provides a compelling alternative to traditional fixed-income investments.

The End of Siloed Investing: AI-Powered Selection for Hedge Funds, Liquid Alts & QIS

"I wanted to thank you for a very interesting webinar... it was a completely different use of AI than I had imagined it would be... So, very interesting! This purpose is not at all subject to the scourge of the common use of AI: overfitting!" (EZ)

[more feedback]

"Insightful! Thank you very much indeed!" (NF)

"Thanks for the presentation!" (SE)

"Thanks guys! Very useful!" (BH)

Tuesday, March 18th 2024

One platform, three universes—reshaping the future of investment selection. Resonanz Capital has pioneered the only AI-powered platform designed for Hedge Funds, Liquid Alts, and Quantitative Investment Strategies, moving beyond outdated methodologies to a new era of precision-driven investing.

Say goodbye to incomplete data, selection biases, and unsystematic decision-making. Powered by cutting-edge AI that transforms traditional selection methods from analog to digital, from guesswork to precision, this platform represents what investment selection will look like in 2030 - available to forward-thinking allocators today.

Experience a quantum leap in investment technology where siloed thinking becomes a relic of the past. Learn how you can empower yourself and your team to see through noise and randomness, delivering structured, data-driven clarity that can transform how you and other top allocators select, invest in, and monitor liquid alternative investments.

Join us for a cutting-edge deep dive into the next generation of AI-powered investing! In this interactive INVESTOR WORKSHOP, Resonanz Capital co-founder Vincent Weber will:

- Explore the hidden synergies and missed opportunities that arise when traditional silos are broken down

- Demonstrate how advanced analytics supercharge selection and risk assessment

- Examine when AI becomes a trusted co-pilot rather than just another tool

- Show how to evolve current practices into a resilient, future-proof framework

Creditor-on-Creditor Violence: New Dynamics in Distressed Debt

"Highly insightful, practical, detailed information. The decades of experience and extraordinary expertise of the presenters shone through, glad I participated!" (RB)

[more feedback]

It was excellent and thank you! (MR)

Thank you very much, great presentation! (AO)

Thanks a lot! Very interesting. :-) (JS)

Wednesday, Jan 15th 2025

In an era of rising interest rates, legal uncertainties, and evolving restructuring tactics, professional investors face unprecedented challenges—and opportunities—in credit markets. From uptiering strategies to cross-class cramdowns, this upcoming INVESTOR WORKSHOP will equip you with exceptionally valuable and actionable insights.

Join us for an in-depth discussion of the emerging trends reshaping credit markets, focusing on the rise of aggressive liability management exercises (LMEs) and their implications for institutional investors:

- Emerging Risks and Opportunities: Understand the implications of aggressive restructuring tactics like liability management exercises (LMEs). Why European markets may soon experience similar volatility to US credit markets.

- The Impact of Regulatory Changes: Explore the evolving legal landscape across Europe and the U.S. and its impact on investor protections. How changes in cross-class cramdown rules are affecting creditor dynamics.

- Strategies for Proactive Investors: Learn how to identify and capitalize on distressed credit opportunities while navigating the risks. Opportunities from market dislocations and restructuring scenarios, and how to protect creditor positions in an increasingly aggressive environment.

Who Should Attend:

- Institutional investors

- Sovereign wealth fund managers

- Family office investment professionals

- Pension fund managers and advisors

- Distressed debt specialists and credit fund managers

The Trump Portfolio Challenge: How to Balance Profit and Protection

Quite impressive to hear Roy speak again, particularly after literally all predictions he made at the previous Opalesque webinar "Debt Ceiling Deja Vu?" were spot on. Let's see how this webinar's predictions crystalize, particularly on inflation (and Bitcoin). (MKF)

[more feedback]

"Time well spent. Roy is one of the more thoughtful commentators and investment managers. Very interesting to hear his analysis of the upcoming Trump administration and implications for investors, the future of the dollar, and his take on investing." (RU)

"Excellent and in-depth presentation, thank you also for answering so many questions!" (SM))

"Thank you all!" (EG)

"Was great, thanks a lot!" (DL)

"Roy's insights are truly invaluable." (DG)

Thursday, Dec. 12th 2024

With the new US administration set to take over, the investment landscape is polarized and volatile. Investors face critical questions as geopolitics, monetary and fiscal policy, portfolio construction and investor psychology collide.

How do you position your portfolio for maximum upside capture should markets continue their rally? And how much downside protection is necessary should things turn down?

What kind of solutions are available for equity portfolios that fulfill the goal of maintaining or enhancing upside returns while providing substantial protection?

For portfolio construction, what about private vs. public? Are alternatives still a good solution? What styles belong in a portfolio?

What kind of volatility should portfolios be prepared for? And what type of emotional/psychological decision-making challenges will investors face should it occur?

What are the Fiscal and Monetary risk factors that could drive market direction in 2025 and beyond? How will the forces of inflation vs. recession play out? Are there hidden, off-the-beaten-track opportunities for diversified portfolios in digital assets, commodities, and beyond?

We’ve scheduled this Critical Investment Briefing to tackle these pressing issues head-on. Join us on December 12, 2024 at 11 AM EST as we dissect the Trump Portfolio Challenge and explore strategies to safeguard your portfolio without sacrificing upside potential. The patterns are familiar but not identical. Just as with past pivotal moments, this challenge requires foresight, a thoughtful strategy, and optimal tactics, along with a keen understanding of history.

Beyond Blockchain & Bitcoin: How Re7 Capital Finds Real Value in Web3

"Excellent webinar, very well presented." (SN)

[more feedback]

Very informative. Thanks! (PC)

Excellent (EG)

Great webinar! (LC)

Wednesday, Nov. 27th 2024

Re7 is a research-driven digital asset investment firm and has excelled as an operator, builder and a strategic allocator across multiple blockchain ecosystems, strategies and instruments. Starting in 2016, Re7 Capital’s founders have operated in the digital assets space through three full cycles. Such multi-cycle experience creates deep understanding of market mechanics and ability to distinguish signal from noise.

A New Paradigm

At the moment, the Web3 economy is in a manifest boom across a wide number of KPIs (e.g. users); blockchain business are generating sizable and growing cash flow. Ethereum surpassed $10bn revenue in 7 years, outpacing top software companies by nearly half the time.

Web3 businesses monetise their users at margins vastly superior to their Web2 counterparts as they coordinate commerce without middlemen. Interestingly, it will actually be Web2 businesses which will act as key catalyst for driving the next wave of adoption.

This is supported by three far-reaching structural changes:

- Sovereign crypto adoption via nation states, global corporations

- Financial system inclusion with mobile, cross-border payment rails, and points card partnerships

- New Product market fits, e.g. through stablecoins, staking infrastructure, NFT marketplace adoption

Opportunity Set

Re7 opportunistically invests in proven crypto projects that fall into a structural gap: liquid tokens in the post-venture stage of growth. Its operating system enables enhanced asymmetric information and deal flow via unique network and proprietary intelligence tooling.

Join us for an exclusive Investor Workshop featuring Evgeny Gokhberg, Managing Partner and CIO of Re7 Capital. With over 14 years of experience in investment management and blockchain technology, Evgeny's expertise uniquely positions him to guide investors through the rapidly evolving Web3 landscape.

In this webinar, Evgeny will discuss:

- Understanding Re7 Capital’s Web3 Tech Cycle Framework: The current state of the crypto market and why we're entering a "golden age" for Web3 investments

- Re7's approach to identifying high-potential projects in the post-venture stage of growth and insights into investment strategies that set Re7 apart in the market

- Case studies of successful investments, including Across and Neutron

- How Re7 proprietary risk rating system and real time position monitoring allows for smart contracts analysis and over 500 protocols monitored real time

- How Re7 five layers of risk assessment and mitigation safeguard investor capital in a volatile market

Don't miss this chance to learn from one of the industry's most experienced teams and learn how to navigate and benefit from the next wave of Web3 adoption. Whether you're a seasoned crypto investor or looking to enter the space, this webinar will provide valuable insights into the future of decentralized technology and its investment potential.

{kind=link}