RSS

RSS|

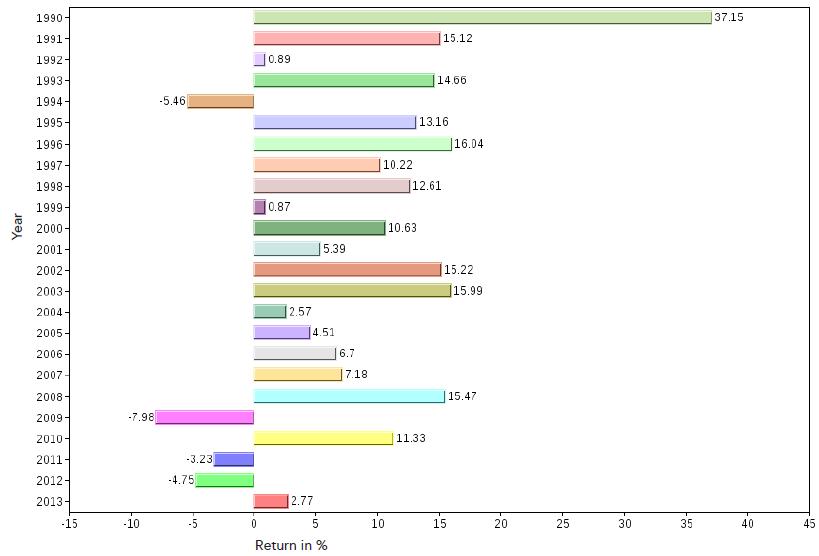

By Mark Melin From 2009 to 2012 managed futures and its primary strategy, trend following, had its most challenging performance in history. As a benchmark, the trend following heavy Altegris 40 index, which only had 4 negative years of performance in its 22 year history, encountered three of those years since 2009. This has led many to ask "Is the managed futures trend following strategy broken," with some investors quickly withdrawing support for the investment. However, is exiting on the investment category's drawdown a prudent choice? Does the generally statistically driven investment category have a history of mean reversion from its drawdown points? Altegris 40 Index Annual Performance 01/90 - 03/13

Is Managed Futures Broken? When looking at previous performance and wondering if the "strategy is broken" is asking the wrong question. If the managed futures performance beta is based on price trends in a market then isn't the real question: are price trends broken? If the strategy is based on price volatility, then isn't the real question: is market volatility broken? This discussion centers on the beta factors that drive performance in managed futures. While it would seem unlikely that price trends and market volatility would disappear from the landscape, the interesting question becomes how has the strategy performed throughout time? Have price trends always existed in markets? Has even the most basic trend following strategy been effective been effective over time? While most studies of managed futures performance tend to date back near 30 years, the birth of the regulated investment category, a recent AQR study of price trends considers market behavior dating back to 1903. The Variable Nature of Price Trends Perhaps most interesting in the AQR study, A Century of Evidence on Trend-Following Investing, is noting how, which price trends are unpredictable, they have always been present at some point in the market environment. Trend following strategies and their related viability were found to deliver positive performance during all study periods. While positive returns were interesting, other statistical measures warrant consideration. For instance, the rate of return on AQR's model portfolio did vary significantly. From a high return of 40.3% during runaway inflation of the 1970s to the low of 9.7% during the depression era, the spread from high to low was wide, but surprisingly not the volatility. Realized volatility in the study ranged from 11.7% during World War Two to a low of 8.4% during the 1990's era of deficit expansion. Further tightening was evidenced in the correlation to the S&P 500, which ranged from 0.21 to -0.30. During the great depression, it should be noted, the correlation of AQR's trend following model to the S&P 500 was 0.00, according to the study. While managed futures performance only officially dates back to 1985, researchers Brian Hurst, Yao Hua Ooi and Lasse H. Pedersen in the AQR research department studied trend following strategies dating back to 1903. Looking behind the numbers, the research most importantly demonstrates that trends have always been a present market environment. Because study data previous to 1985 is sparse, researchers were required to measure trend following in general using a basic trend following time / series momentum strategy. What's interesting is that by basing the study on a trend following strategy rather than judging manager performance, researchers can extract the "beta" of the investment. This, in turn, helps validate the core concept that trends are always present in the market environment at some point. The Cyclical Nature of Trends Trend following professionals note that what is statistically interesting is in 2012 markets didn't find meaningful trends across any time horizon. Price persistence, or "trendiness" in market prices, is both expansionary and carries mean reversion traits as well. Price trends are expansionary in that, during powerful market trends, once one market begins to exhibit strong price persistence other markets may follow suit. This could be due to a number of reasons, including fundamental economic factors driving supply and demand across a variety of markets. But trend followers don't consider the fundamentals as much as the meaning behind the price movement in markets. The market environment for consistent price persistence, or trendiness, was above mean in 2008. As a result, managed futures generally experienced its best performance in history. With 20 / 20 hindsight one might think it clear to exit managed futures while the investment category was on the outside of its statistical mean just as one might expect investors to enter the program when it was on its statistical bottom of the range of returns. Market Environment Cyclicality Which was a very above mean type environment for trend following and thus the strategy exhibited above mean performance relative to other asset classes. Once a trend ends, regardless of the time frame, the tendency is for markets to compress or absorb volatility, thereby setting up the next wave of directional movement. "We tend to see trends come in 3 to 5 year rolling waves, or cycles, in the longer duration timeframe," said Cole Wilcox, who operates three funds at Longboard Asset Management. "With an ultra long term trend follower, for instance, we may have 3 to 5 years of above mean performance environments and 3 to 5 years of average to below mean performance environments, with some of those years substantially below average." To be a successful trend following investor is to understand cyclicality of the performance drivers. "Just like farming, when crop yields are low, it isn't appropriate to consider that 'farming is broken.' Trend following isn't broken because price trends, at a basic level, are a feature of the market environment." Performance Sources: |

|

This article was published in Opalesque Futures Intelligence.

|

{kind=link}