RSS

RSS|

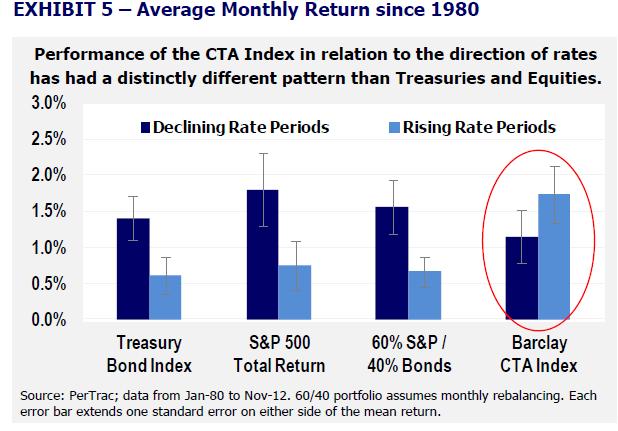

By Mark Melin Campbell & Company, a specialist in systematic trading strategies, touched on a hot button issue recently when it released its white paper "Prospects for CTAs in a Rising Rate Environment." Among institutional investors one of the managed futures investing concerns has been the relative impact of interest rates on CTA performance. Although never widely discussed, the owner of the managed futures segregated account can benefit from interest income derived off the margin deposit. Due to this funding structure, CTAs have multiple returns streams. The primary performance driver is their trading strategy, but under certain circumstances CTAs also generated returns from the collateralized margin deposit that could be invested in interest bearing products such as short term US Treasuries. This additional returns driver, available only on investments that utilize a margin deposit, was always whispered to be part of the "secret sauce" of why managed futures performance has been traditionally strong. Thus, a managed futures investment was always viewed in part as a play on interest rates. In regards to returns from investments in Treasury Products, when rates were high and moving lower, the CTA might have benefited from two returns sources: the interest income from the treasury products and the price appreciation from the bonds. Problem is CTAs who benefited from interest income and bond prices might encounter difficulty in a rising rate environment, is thinking among some. However, this myth might not be entirely accurate. What is not being considered is the CTA can actually benefit from rising rates in the form higher interest income. While the value of a short term bond may declinein price as interest rates rise, these bonds are typically held to maturity by a cash management firm, thus negative price swings in performance bonds are negligible on the CTA's performance. Enter the study by Campbell & Company, which takes a statistical look at CTA performance during periods of rising interest rates. With interest rates at all time lows and much analysis focusing on the potential for a rising rate environment when the Fed finally stops manipulating the yield curve, the question becomes salient to investors. Statistical Study of Managed Futures during Rising Rate Environments The study considered the Barclay CTA index, where performance data of the diversified index back to 1980 and study bias issues with the index are reasonably close to issues with equity indexes. The Campbell study showed that in fact performed well during periods of rising rates, outperforming equity investments. Trends come and go, and on a statistical basis the trendless market environment has been rather long in the tooth.

Is All Interest Income Calculated in Reported Returns? What the study did not address is that depending on the account type and investor sophistication, the investor might not be credited with interest earned off collateralized margin deposits. For instance, much of the general Barclay CTA index is comprised of CTAs who might have operated in a distribution channel where the brokerage firm, not the CTA, accrued the interest income from the margin deposit. This thus such interest earned ("float") may not be included in the CTA's performance calculation. In a direct segregated account opened in the name of the investor, and not the CTA, the institution might typically accrue 60% or 80% of the interest income, depending on the negotiation and services being provided by the brokerage firm. In a retail account such interest is typically accrued to the brokerage firm. The point is, under many circumstances, the CTA might not even be capturing interest income. The Barclay CTA index is generally considered to include a significant number of CTAs using in retail distribution channels through FCMs, and thus the CTA likely did not accrue interest income and could not report this as a component of their performance capsule. Performance reported by a CTA to major CTA databases is typically reviewed by the National Futures Association (NFA) during their audit of the CTA. In a direct segregated account the goal to ensure that reported performance is an accurate reflection of the actual investor experience, inclusive of all fees, expenses.� Further, performance reporting between databases is typically monitored by the brokerage industry and reviewed by investors. To download the CTA report in detail, click on this link to visit www.uncorrelatedinvestments.com (requires free registration). � Prospects for CTAs in a Rising Interest Rate EnvironmentThe following is an excerpt of the Campbell & Company Study EXECUTIVE SUMMARY

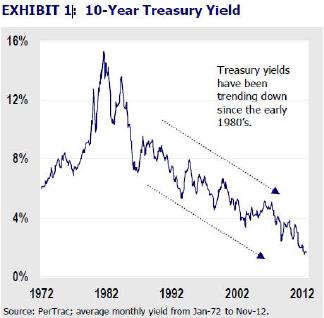

INTRODUCTION The last sustained rise in interest rates, as defined by the direction of the Fed Funds rate, ended in 1982. Since then, with the exception of just a few years in each of the last three decades, the US Federal Reserve has proffered an easy money policy, gradually guiding interest rates down from the Volker-era stratosphere.

During this period, the alternative investment industry evolved dramatically from its nascent stages in the 1970s, when it consisted of a handful of funds managing a relatively small pool of assets. Consequently, the majority of active hedge funds and CTAs have spent their entire existence operating in a bull market for fixed income, and have yet to experience a secular uptrend in rates. This lack of experience and corresponding lack of performance data can make it somewhat challenging for investors to set appropriate expectations for such an environment. Many pundits began predicting an imminent turning point in interest rates several years ago, as the Fed Funds target rate sat dormant at 0%-0.25% and yields on long-dated government securities seemingly bottomed out. Since then, however, deterioration in the Eurozone, an uncertain climate in the Middle East, and fiscal concerns in the US have caused rates to decline even further; as we now know, one of the best trades in 2011 was simply to be long Treasuries. As of this writing (December 2012), Treasury yields remain near their historical lows. The purpose of this paper is not to predict when interest rates will begin to trend upwards, how high they will go, or what the catalyst will be for such a change. This paper will instead evaluate the possible implications to the CTA industry of a shift to a rising interest rate environment in the US. To download the CTA report in detail, click on this link to visit www.uncorrelatedinvestments.com (requires free registration). |

|

This article was published in Opalesque Futures Intelligence.

|

{kind=link}