RSS

RSS|

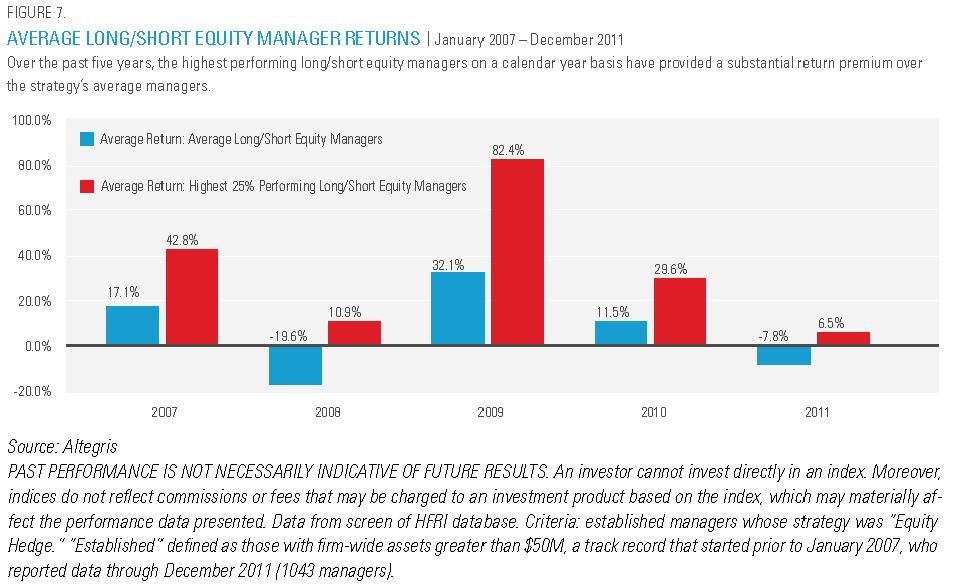

Part two of a two part report by Jon Sundt, President & CEO, Altegris Executive Summary The recent financial crisis spurred investors to focus on liquid, noncorrelated assets in their quest to better manage portfolio risk-while still seeking returns. It is no surprise, then, that increasing numbers of financial advisors and their clients have been considering liquid alternative investments to help meet this challenge. At Altegris, we define liquid alternative investments as mutual funds that may be suitable for a wide range of investors, and which provide access to best-of-breed alternative investment managers who can go long or short in various markets. While alternative investments have typically been geared toward institutional and high-net-worth investors, liquid alternatives enable a broader range of investors to take advantage of the historic strengths of hedge funds, while also benefiting from the attributes of mutual funds. Alternatives have been migrating to a broader investor base for some time, but that trend has gathered speed in the wake of the financial crisis. Investors are seeking out liquid alternatives that offer the potential for uncorrelated returns, lower volatility, and greater transparency and liquidity, while alternative investment managers are increasingly open to offering their strategies via more liquid vehicles, as they represent another potential avenue for asset growth and provide access to a new investor base. Some alternative investment strategies are better suited to a mutual fund structure than others. At Altegris, we believe that long/short equity, managed futures and global macro are particularly strong fits within a mutual fund framework. In Altegris' view, long/short equity, managed futures and global macro should be included in a core alternatives allocation within a portfolio, and together offer the potential for lowering volatility and generating strong, non-correlated returns- providing both downside protection and enhanced performance potential in rising markets. In contrast to this core, some strategies that are compelling in a hedge fund format do not necessarily translate as well to mutual funds-due to a lack of liquidity or because they require levels of gross long and/or short exposure* beyond what is allowable in a mutual fund structure in order to generate appropriate risk-adjusted returns. With the universe of alternative investment managers available via mutual funds expanding rapidly, it is becoming more of a challenge to identify premier investment talent. As such, we believe there are clear benefits from partnering with a firm such as Altegris that has built deep relationships with "the real deal"-- top-flight, experienced alternative investment managers with the ability on a historical basis to deliver alpha-and can package their strategies in a liquid format for a range of advisors and their clients. At Altegris, we believe that this elite level of talent is worth paying for-from a mutual fund investor's standpoint, potentially higher fees for select liquid alternatives are appropriate in exchange for access to some of the best investment managers in the world. Particularly in light of recent history, we believe that it is critical for investors to maintain investment flexibility and focus on strategies with the ability to perform in a variety of market conditions. Therefore, we suggest that investors build a diversified portfolio and position themselves to take advantage of a range of market opportunities, including allocating to a mix of "convergent" and "divergent" strategies available in liquid structures- with long/short equity, managed futures and global macro representing prominent examples of these two types of categories. By gaining exposure to premier alternative investment managers, in a liquid format, investors can potentially enjoy the best of both worlds-the flexibility and convenience of mutual funds and the portfolio effects of alternative investments-in the pursuit of their long-term investment goals. This is the second half of a two part article. To see the previous article, click here. "The Real Deal" With the universe of alternative investment managers available via mutual funds expanding rapidly-on top of the 5,000-plus hedge funds already in operation-it is becoming more of a challenge for investors to identify and access the most talented investment professionals. As such, we believe there are clear benefits from partnering with a firm such as Altegris that has built deep relationships with premier alternative investment managers around the world, and can secure opportunities to invest with these managers and package their strategies in a liquid format for a range of advisors and their clients. At Altegris, we believe that investors realize the full benefits of liquid alternatives only when they work with "the real deal": top-flight, experienced alternative investment managers with a robust infrastructure behind them, and the demonstrated ability to deliver alpha in a variety of market environments. Figure 7 illustrates the degree to which the best managers can outperform relative to average managers within a particular alternative investment strategy-in this case, long/short equity. In addition, this performance dispersion highlights the fact that, unlike traditional investments whose performance is typically measured relative to benchmarks, the absolute returns of alternative investments are driven by manager skill- and thus manager selection is particularly important.

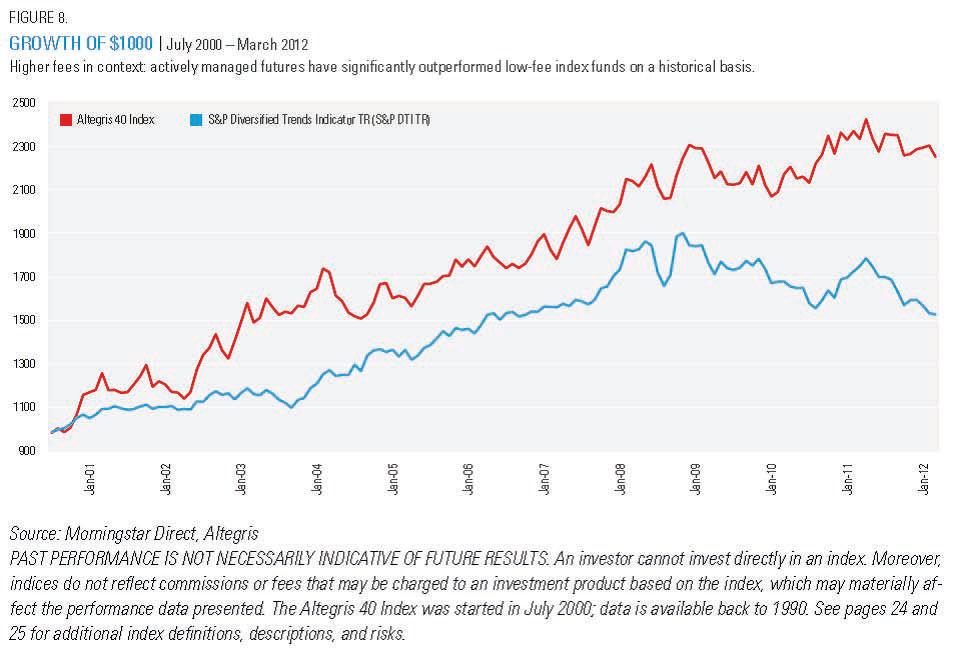

In order to facilitate these opportunities for investors, an advisor should possess the expertise in alternatives to blend top-down viewpoints with bottom-up analysis to identify the most compelling market opportunities for clients and the best-of-breed managers within each strategy. A detailed assessment and multilayered due diligence process for each manager is also essential before an investment is approved. An advisor must then be able to provide an entrée to managers who are often capacity constrained or have historically provided limited access to non-institutional investors. Once strategies are implemented within a multi-manager portfolio, the advisor should utilize advanced return analysis and risk profiles to actively manage and rebalance the portfolio. Finally, the advisor should have the resources to perform an ongoing evaluation of each manager in the portfolio-including constant investment review and risk monitoring. This blend of alternatives background, investment skills and analytical resources is rare among investment advisors, based on our experience, and is a key rationale for partnering with a firm such as Altegris. For mutual fund investors more accustomed to low-cost, index-based products, the higher fee levels often associated with exposure to liquid alternatives can be an issue. At Altegris, we believe that true talent is worth paying for-from a mutual fund investor's standpoint, potentially higher fees are appropriate in exchange for access to some of the best investment talent in the world: an elite group of managers within the alternative investment universe with a history of consistently generating strong risk-adjusted returns in both up and down markets, supported by institutional-quality infrastructure. Whether in private placement or mutual fund format, the best managers can be more expensive for investors to engage directly-if they are open to new investors at all. Regardless of the vehicle, the best managers are in a position to be able to command higher fees-if they can deliver consistently strong risk-adjusted returns, those fees represent a wise investment, in our view. Figure 8 shows the extent to which a higher-fee investment can compound assets relative to a low-fee vehicle. Within Morningstar's managed futures category, many passive strategies-which generally feature lower fees than their actively managed counterparts-track the Diversified Trends Indicator (DTI) Index, which can go both long and short depending on whether prices are above or below their seven-month moving average. In our example, we compare the compound growth of an initial $1,000 investment in the DTI with an identical allocation to the Altegris40, an asset-weighted index that comprises the 40 largest managers in the managed futures space. Managers report their returns net of both performance fees (typically around 20%) and management fees (around 2%) for inclusion in the Altegris 40 Index. As such, the substantial 73% difference in the compound of the allocation to that index vs. an investment in the DTI since July 2000 underscores the notion that higher fees can be worthwhile in the service of better returns. Certainly, passive exposures via indices, such as in exchange-traded funds (ETFs), represent a viable- and popular-option for investors seeking more liquid access to alternatives. However, Altegris believes that actively managed mutual funds have the ability to best capture the risk-return attributes of core alternative investment strategies such as long/short equity, managed futures and global macro due to their nimbleness and flexible investment opportunity sets.

Preparing for the Markets' Next Phase Particularly in light of recent history, we believe that it is critical for investors in formulating their long-term plans to maintain investment flexibility and focus on strategies with the ability to perform in a variety of market conditions. At the same time, we also believe that the ability to go long and short in various asset classes is a key driver for extended investment success. While it's difficult to draw up a macroeconomic forecast for the next few years, volatility in the markets is a factor that will always exist to some extent regardless. As a result, we believe it is important for portfolios to incorporate investments that are able to not only withstand times of increased market volatility, but potentially profit from them as well-and managed futures within our alternatives core may be one such investment (See Figure 9). Managed futures have historically performed well in a wide variety of market conditions, including when expected volatility is high or simply shifting. The ability of managed futures to perform despite market volatility may, therefore, be beneficial to those seeking to counter market uncertainty.

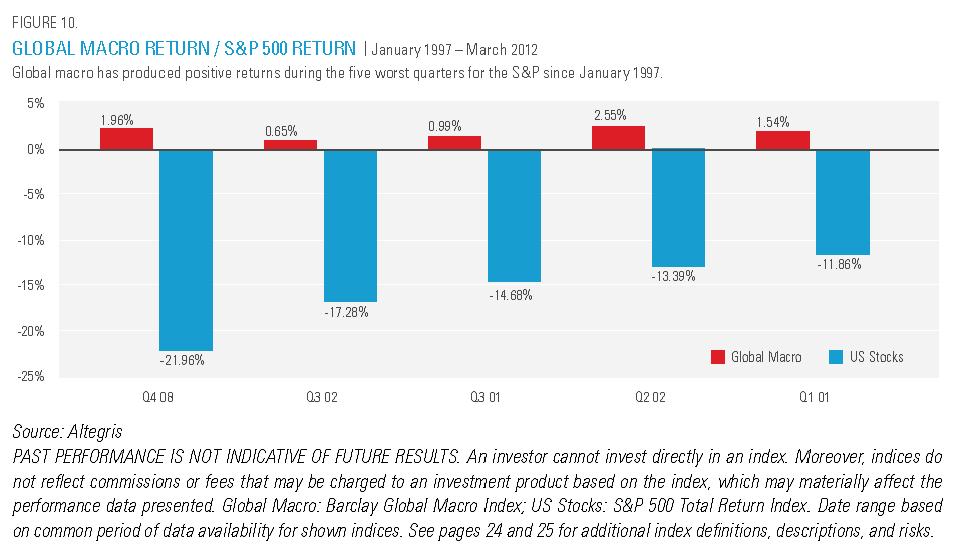

Beyond preparing for continued volatility, we believe that investors should endeavor to build a diversified portfolio and position themselves to take advantage of a range of market opportunities by allocating to a mix of so-called "convergent" and "divergent" strategies that are available in liquid structures-a topic that Altegris plans to examine in greater detail in an upcoming white paper. Convergent strategies are based on the idea that the intrinsic value of securities and asset classes can be measured using fundamental data. By analyzing this data, a convergent manager can express an opinion on whether a security is over-/undervalued, believing that the price will "converge" to its intrinsic value over time. Long/short equity is a prominent example of a convergent strategy. Divergent strategies, in contrast, aim to profit when fundamental valuations are ignored by the market. These strategies-of which managed futures is a prime example-seek to identify and exploit serial price movement (trends and momentum) that reflect changing market themes and investor sentiment. Global macro is a strategy that could fall under either category, depending on the market environment. Macro managers may anticipate market dislocations and position their portfolios for "divergence," or they may identify mispriced markets and position their portfolios for "convergence." In fact, global macro's flexibility is further underscored by the fact that the strategy has historically exhibited strong performance in bear markets- particularly relative to equities. In fact, global macro's flexibility is further underscored by the fact that the strategy has historically exhibited strong performance in bear markets- particularly relative to equities. Figure 10 illustrates how global macro managers as a group have demonstrated significant "crisis alpha"-the ability to make profits in periods when long-only strategies have experienced substantial losses.

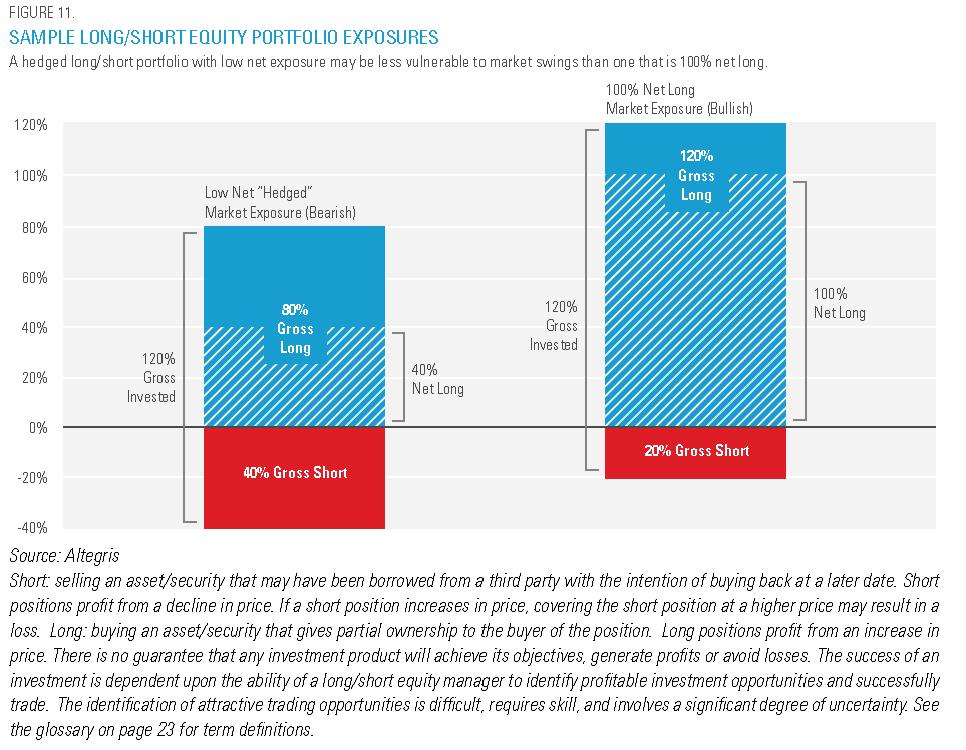

Amid changing economic conditions, we believe that the ability-and skill-to go both long and short is crucial for delivering strong risk-adjusted returns in up and down markets. Strategies that include long and short exposures can be highly flexible, and managers can adjust those exposures to a variety of market conditions. In long/short equity, for example, higher net long exposures (where long exposure is significantly greater than short exposure) will generally correspond with periods of increased bullishness in the strategy, while lower net exposures would typically indicate a more bearish outlook and/or cautious positioning. We believe that this ability to adapt exposures on both the long and the short sides of portfolios provides an edge over traditional long-only portfolios, where the manager might rely on stock-picking abilities and market beta. That is, a long/short portfolio can be adjusted to hedge against swings in the market, whereas a portfolio that is 100% net long (high beta) is vulnerable to such swings (See Figure 11).

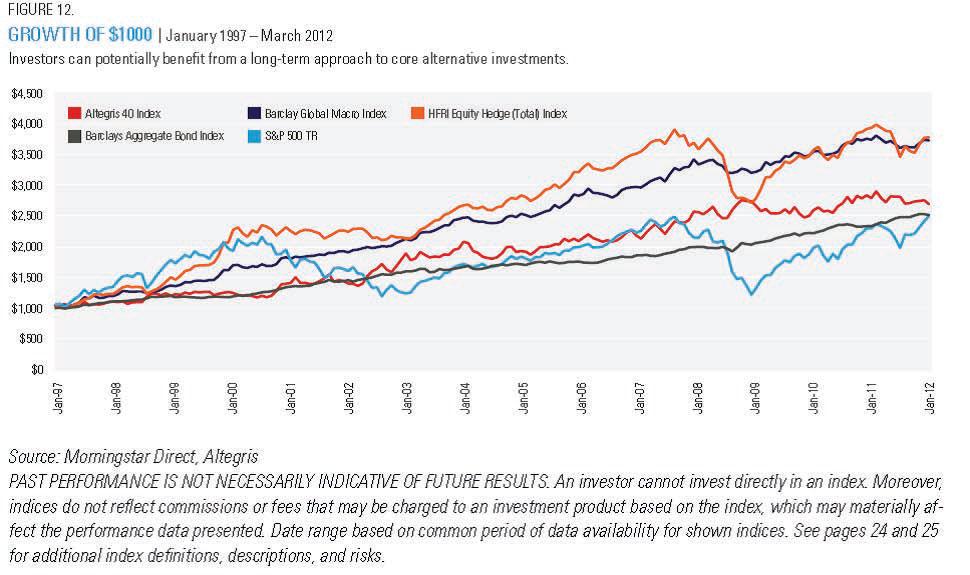

Additional alpha may be generated by a manager's ability to successfully pick securities on both the long and the short sides. As a result, the best managers not only use shorting as a hedging mechanism, but also as an opportunistic means of delivering alpha in a range of environments. This further underscores the appeal of experienced alternative managers who have a history of successfully identifying securities on both the long and short sides, and simultaneously managing the delicate balance between those two books-as opposed to managers transitioning from the long-only world who might be astute at identifying undervalued securities but have not yet proven that they possess the skills to efficiently oversee a short portfolio. In the context of a long-term investment strategy, long/short equity, managed futures and global macro are all designed to do well in a wide range of short-term market conditions. As liquid, opportunistic, non-correlated investments, these strategies can potentially allow an investor to weather an array of short-term conditions in order to achieve his or her longer-term risk-adjusted return objectives, as illustrated by the compound growth of a $1,000 investment in Figure 12.

Conclusion Alternative investments and mutual funds have historically existed in separate realms-where high-net-worth and institutional investors have been the beneficiaries of access to the former, and a broader range of investors have taken advantage of the strengths of the latter. However, recent years have seen a blurring of the lines between the two worlds-and that shift has gathered momentum in the wake of the financial crisis. By gaining exposure to premier alternative investment managers, in a liquid, mutual fund format, investors can infuse their portfolios with more flexibility, reduce correlations to stocks and bonds and improve their potential risk-return profiles. Altegris believes that, through the use of liquid alternatives, investors can potentially enjoy the best of both worlds-mutual funds and alternative investments-as they pursue their long-term investments goals. Risks and Important Considerations Altegris Advisors LLC is an SEC-registered investment adviser that advises alternative strategy mutual funds that may pursue investment returns through a combination of managed futures, macro, equity long short, fixed income and/or other investment strategies. MUTUAL FUNDS INVOLVE RISK INCLUDING POSSIBLE LOSS OF PRINCIPAL. As with all mutual funds, there is the risk that you could lose money through your investment in the Fund. No Fund is intended to be a complete investment program. Many factors affect a fund's net asset value and performance and there can be no assurance that any fund will achieve its investment objectives. Alternative investment mutual funds are subject to certain risks including, but not limited to, non-diversification risk, which means that a fund may invest in fewer securities at any one time than a diversified fund and the fund's performance may be more sensitive to any single economic, business, political or regulatory occurrence. Factors such as domestic and foreign economic growth and market conditions, interest rate levels and political events affect the securities and derivatives markets. When the value of the fund's investments goes down, your investment in a fund decreases in value and you could lose money. An investment in derivatives, such as futures and options contracts, involves additional risks that a fund would not be subject to if it invested directly in the securities and commodities underlying those derivatives. The fund may experience losses that exceed losses experienced by funds that do not use futures contracts and options. Long options positions may expire worthless. Although futures contracts are generally liquid instruments, under certain market conditions there may not always be a liquid secondary market. Trading restrictions or limitations may be imposed by an exchange, and government regulations may restrict trading in futures contracts and options. Over-the counter transactions are subject to little, if any, regulation and may be subject to the risk of counterparty default. When a fund invests in fixed income securities or derivatives, the value of your investment in the fund will fluctuate with changes in interest rates. In general, the market price of debt securities with longer maturities will increase or decrease more in response to changes in interest rates than shorter-term securities. Other risk factors include credit risk (the debtor may default) and prepayment risk (the debtor may pay its obligation early, reducing the amount of interest payments). "High yield" or "junk" bonds present greater credit risk than bonds of higher quality, as well as heightened liquidity risk and risk of default. Foreign investing involves risks not typically associated with US investments, including adverse fluctuations in foreign currency values, adverse political, social and economic developments, less liquidity, greater volatility, less developed or less efficient trading markets, political instability and differing auditing and legal standards. These risks are magnified in emerging markets. Alternative investment mutual funds may also engage in short selling and short position derivative activities, which involve significant financial risk. Positions in shorted securities and derivatives are speculative and more risky than "long" positions (purchases) because the cost of the replacement security or derivative is unknown. Therefore, the potential loss on an uncovered short is unlimited, whereas the potential loss on long positions is limited to the original purchase price. You should be aware that any strategy that includes sellingsecurities short could suffer significant losses. Shorting will also result in higher transaction costs (such as interest and dividends), which reduces a fund's return, and may result in higher taxes. The use of leverage by a fund, such as borrowing money to purchase securities or the use of options, will cause the Fund to incur additional expenses and magnify the fund's gains or loss. The investment expertise of the portfolio manager may prove to be inaccurate and may not produce the desired results. The manager's judgments about the attractiveness, value and potential appreciation or depreciation of a particular security in which the fund invests may prove to be inaccurate and may not produce the desired results. If used in connection with the sale or promotion of an investment company product, this material must be preceded or accompanied by a prospectus for the respective product. About Altegris Altegris searches the world to find what we believe are the best alternative investments. Our suite of private funds, actively managed mutual funds and managed accounts provides an efficient solution for financial professionals and individuals seeking to improve portfolio diversification. With one of the leading research and investment groups focused solely on alternatives, Altegris follows a disciplined process for identifying, evaluating, selecting and monitoring investment talent across a spectrum ofalternative strategies including managed futures, global macro, long/short equity, event driven and others. Veteran experts in the art and science of alternatives, Altegris guides investors through the complex and often opaque universe of alternative investing. Alternatives are in our DNA. Our very name, Altegris, highlights our singular focus on alternatives, the highest standards of integrity and a process that constantly seeks to minimize investor risk while maximizing potential returns. The Altegris Companies, wholly owned subsidiaries of Genworth Financial, Inc., include Altegris Investments, Altegris Advisors, Altegris Funds and Altegris Clearing Solutions. Altegris currently has approximately $3.36 billion in client assets, and provides clearing services to $774 million in institutional client assets.* * Altegris and its affiliates are subsidiaries of Genworth Financial, Inc. and are affiliated with Genworth Financial Wealth Management, Inc., and include: (1) Altegris Advisors, LLC, an SEC registered investment adviser; (2) Altegris Investments, Inc., an SEC-registered broker-dealer and FINRA member; (3) Altegris Portfolio Management, Inc. (dbaAltegris Funds), a CFTC-registered commodity pool operator, NFA member and SEC-registered investment adviser; and (4) Altegris Clearing Solutions, LLC, a CFTC-registered futures introducing broker and commodity trading advisor and NFA member. The Altegris Companies and their affiliates have a financial interest in the products they sponsor, advise and/or recommend, as applicable. Depending on the investment, the Altegris Companies and their affiliates and employees may receive sales commissions, a portion of management or incentive fees, investment advisory fees, 12b-1 fees or similar payment for distribution, a portion of commodity futures trading commissions, margin interest and other futures-related charges, fee revenue and/or advisory consulting fees. Genworth Financial, Inc. (NYSE: GNW) is a leading Fortune 500 insurance holding company dedicated to helping people secure their financial lives, families and futures. Genworth has leadership positions in offerings that assist consumers in protecting themselves, investing for the future and planning for retirement-including life insurance, long-term care insurance, financial protection coveragesand independent advisor-based wealth management-and mortgage insurance that helps consumers achieve home ownership while assisting lenders in managing their risk and capital. |

|

This article was published in Opalesque Futures Intelligence.

|

{kind=link}