RSS

RSS|

Top-Selling Industry Author Wisdom of Buy and Hold Questioned By Mike Dever and John Uebler In 1999, global stock markets were at the peak of an 18-year secular bull market. Buy-and-hold had become a mantra. That’s no big surprise. At that time, there was no doubt that a person who had bought and held U.S. stocks (NYSEArca: SPY) over a long period would have made more money than in almost any other investment. But that belief was neither rocket science nor sound investment advice. It was merely a simple observation. Yet books, articles, and investment seminars, by the truckload, were produced that expounded on the benefits of buy-and-hold.

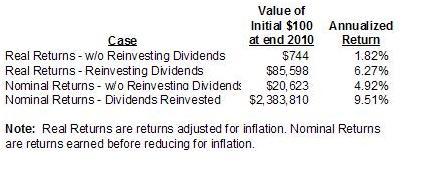

Since the start of 1900, U.S. equities produced a real average annualized return of 1.82% if dividends were spent, rather than reinvested, and a 6.27% real annualized return with dividends reinvested. The “real” return adjusts the performance for the negative effects of inflation, which reduced the returns by more than 3% per year on average. If we were to look at the “nominal” return, the amount stocks earned before adjusting for inflation, the returns jump to 4.92% if dividends were spent and 9.51% with dividends reinvested.

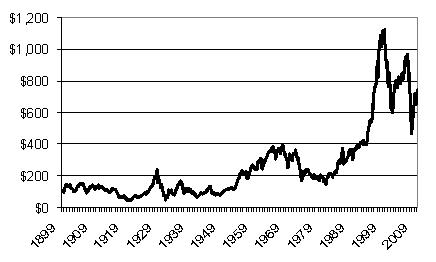

Growth of $100 Placed into U.S. Stocks in 1990 Real Returns – Without Dividends

This means that for more than 50 years any person who placed $100 into a broad basket of U.S. stocks (such as NYSEArca: IBM, NYSEArca: KO, NYSEArca: CAT, NYSEArca: JPM) and who did not reinvest his or her dividends, would have suffered a loss, allowing for inflation. This really does give new meaning to the term “long run.” However, perhaps even more is the fact that all of the real stock market returns earned over the past 111 years can be attributed to just an 18 year period – the great bull market that began in August 1982 and ended in August 2000. Without those 18 years the real, inflation-adjusted return of stocks, without reinvesting dividends, was negative! This highlights the greatest risk of the buy-and-hold strategy, which is that stock market returns are extremely “lumpy”. About the Authors: 1. Robert J. Shiller, Irrational Exuberance (Princeton: Princeton University Press, 2000, 2005, updated). Data used in Shiller book and for S&P 500 Total Return performance available at: http://www.econ.yale.edu/~shiller/data/ie_data.xls. Retrieved February 14, 2011. 2. Shiller, “Irrational Exuberance.” Regulator News News Item: On June 9, 2012 PFG founder and CEO Russ Wasendorf Sr. was found parked in his car outside the Cedar Falls, IA corporate headquarters in a suicide attempt. In the car was a note where the futures industry executive confessed he had committed fraud for 20 years. NFA takes emergency enforcement action against Chicago futures firms Peregrine Financial Group, Inc. and Peregrine Asset Management, Inc. NFA has taken the Member Responsibility Action (MRA) to protect customers because PFG has failed to demonstrate that it meets capital requirements and segregated funds requirements. NFA also has reason to believe that PFG does not have sufficient assets to meet its obligations to its customers. Effective immediately, PFG and PAM are prohibited from soliciting or accepting any additional customer accounts or customer funds, except as margin for existing positions. Additionally, PFG and PAM are prohibited from accepting or placing trades for any customer accounts except for the liquidation of existing customer positions and are prohibited from distributing, disbursing or transferring any funds, including to existing customers, without the prior approval of NFA. |

|

This article was published in Opalesque Futures Intelligence.

|

{kind=link}