RSS

RSS|

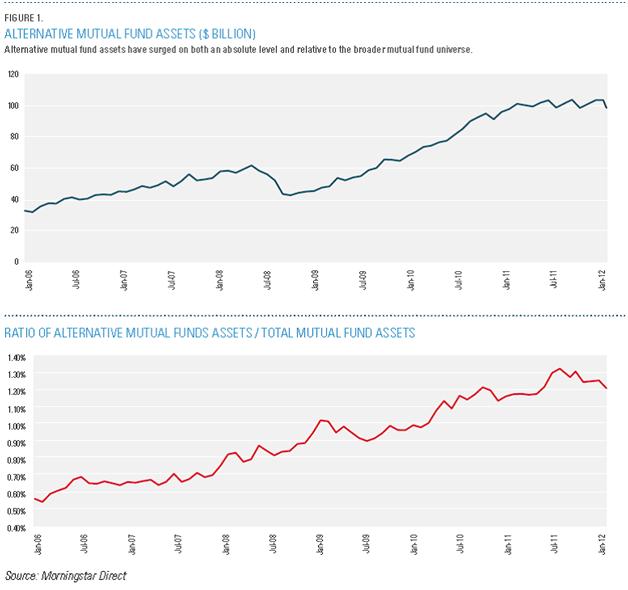

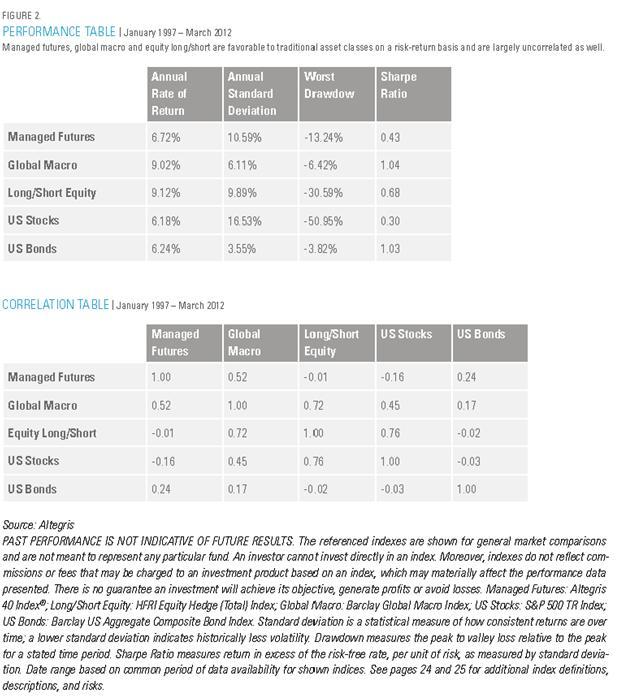

Part one of a two part report by Jon Sundt, President & CEO, Altegris Executive Summary The recent financial crisis spurred investors to focus on liquid, noncorrelated assets in their quest to better manage portfolio risk-while still seeking returns. It is no surprise, then, that increasing numbers of financial advisors and their clients have been considering liquid alternative investments to help meet this challenge. At Altegris, we define liquid alternative investments as mutual funds that may be suitable for a wide range of investors, and which provide access to best-of-breed alternative investment managers who can go long or short in various markets. While alternative investments have typically been geared toward institutional and high-net-worth investors, liquid alternatives enable a broader range of investors to take advantage of the historic strengths of hedge funds, while also benefiting from the attributes of mutual funds. Alternatives have been migrating to a broader investor base for some time, but that trend has gathered speed in the wake of the financial crisis. Investors are seeking out liquid alternatives that offer the potential for uncorrelated returns, lower volatility, and greater transparency and liquidity, while alternative investment managers are increasingly open to offering their strategies via more liquid vehicles, as they represent another potential avenue for asset growth and provide access to a new investor base. Some alternative investment strategies are better suited to a mutual fund structure than others. At Altegris, we believe that long/short equity, managed futures and global macro are particularly strong fits within a mutual fund framework. In Altegris' view, long/short equity, managed futures and global macro should be included in a core alternatives allocation within a portfolio, and together offer the potential for lowering volatility and generating strong, non-correlated returns- providing both downside protection and enhanced performance potential in rising markets. In contrast to this core, some strategies that are compelling in a hedge fund format do not necessarily translate as well to mutual funds-due to a lack of liquidity or because they require levels of gross long and/or short exposure* beyond what is allowable in a mutual fund structure in order to generate appropriate risk-adjusted returns. With the universe of alternative investment managers available via mutual funds expanding rapidly, it is becoming more of a challenge to identify premier investment talent. As such, we believe there are clear benefits from partnering with a firm such as Altegris that has built deep relationships with "the real deal"-- top-flight, experienced alternative investment managers with the ability on a historical basis to deliver alpha-and can package their strategies in a liquid format for a range of advisors and their clients. At Altegris, we believe that this elite level of talent is worth paying for-from a mutual fund investor's standpoint, potentially higher fees for select liquid alternatives are appropriate in exchange for access to some of the best investment managers in the world. Particularly in light of recent history, we believe that it is critical for investors to maintain investment flexibility and focus on strategies with the ability to perform in a variety of market conditions. Therefore, we suggest that investors build a diversified portfolio and position themselves to take advantage of a range of market opportunities, including allocating to a mix of "convergent" and "divergent" strategies available in liquid structures- with long/short equity, managed futures and global macro representing prominent examples of these two types of categories. By gaining exposure to premier alternative investment managers, in a liquid format, investors can potentially enjoy the best of both worlds-the flexibility and convenience of mutual funds and the portfolio effects of alternative investments-in the pursuit of their long-term investment goals. The Emergence of Liquid Alternative Investments One of the principal legacies of the financial crisis that began in 2008 has been an increased focus on liquid, non-correlated assets, as investors seek to better manage risk in their portfolios-without giving up on performance. It is no surprise, then, that increasing numbers of financial advisors and their clients are turning to liquid alternative investments to help meet this challenge. At Altegris, we define liquid alternative investments as mutual funds that may be suitable for a wide range of investors, and which provide access to best-of- breed alternative investment managers who can go long or short in various markets. While alternative investments have historically been the exclusive At the same time, these investors benefit from the hallmarks of mutual funds, including a daily liquidity, low investment minimums, more flexible investor pre-qualifications and efficient 1099 tax reporting. Alternatives have been migrating to a broader investor base for some time, but this trend has gathered speed in the wake of the financial crisis. As illustrated in Figure 1, assets in alternative mutual funds have increased 128% since October 2008, to $99B as of March 2012, while the ratio of alternative mutual fund assets to total mutual fund assets has risen 35.7% during that same timeframe, according to Morningstar Direct. In the wake of the crisis, investors are seeking out liquid alternatives that offer the potential for uncorrelated returns, lower volatility, and increased transparency and liquidity. For example, more than 71% of financial planners ranked correlation among their top five considerations in evaluating alternative investments, followed by risk and liquidity, according to the Financial Planning Association's 2011 Alternative Investments Survey, conducted in May 2011. Investors in UCITS (a European investment product similar to US mutual funds) said in a survey published in November 2010 by Strategic Insight and Global Custodian magazine, Alternative and Hedge Fund UCITS in the Next Decade, that liquidity is the most important factor supporting the growth of alternative UCITS. In addition, institutional investors polled in a 2010 KPMG survey, Transformation: The Future of Alternative Investments, cited transparency as the primary challenge facing the alternative investment industry. At a time of rising investor demand, alternative investment managers are also becoming increasingly open to offering their strategies via more liquid vehicles as they seek to expand their businesses. Liquid alternatives offer managers another avenue for asset growth at a point when competition has never been fiercer-estimates peg the number of alternative investment managers operating globally at more than 5,000. In addition, mutual fund investors represent a relatively untapped-and relatively "sticky"-client base for alternative investment managers, as assets comprising a number of smaller allocations from advisors and individual high-net worth investors can be more stable than a large block from a single institutional investor. The Best Strategies for Liquid Alts Some alternative investment strategies are better suited to a mutual fund structure than others. At Altegris, we believe that long/short equity, managed futures and global macro are particularly strong fits within a mutual fund framework, and that these strategies should comprise a core allocation for any investor seeking a diversified exposure to alternative investments. Long/short equity typically entails a manager going long equities he or she expects to increase in value, while selling short equities he or she expects to decrease in value. Managed futures, in contrast, comprise a highly technical strategy in which managers generally utilize proprietary, model-based trading systems to identify market trends and react to corresponding price movements in securities. Global macro is a fundamental strategy in which managers use macroeconomic data to predict price movements. As a result, investors allocating to these strategies via liquid alternatives can enjoy some of the primary potential advantages of mutual funds-a high degree of transparency, the ability to quickly invest and redeem (thus aiding in actively rebalancing portfolios), and regulatory and board oversight-while also reaping the possible rewards of alternative investment exposure, including strong potential risk-adjusted returns and reduced volatility (See Figure 2).

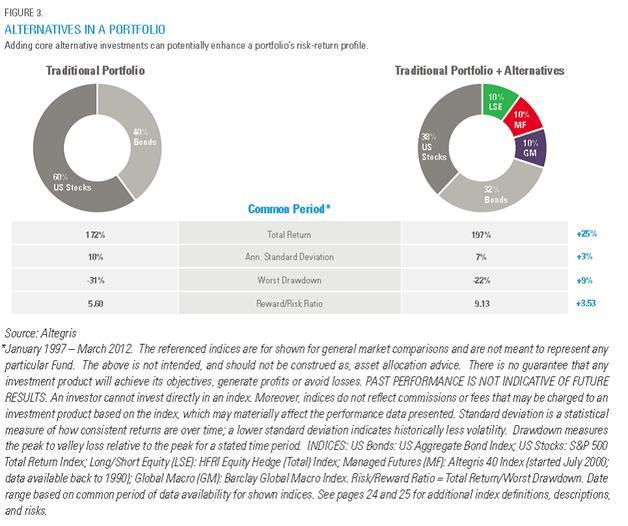

Long/Short Equity, Managed Futures and Global Macro: The Core of Alternative Investments In Altegris' view, long/short equity, managed futures and global macro should be included in a core alternatives allocation within a portfolio, and together offer the potential for lowering volatility and generating strong, non-correlated returns (See Figure 3)-providing both downside protection and enhanced performance potential in rising markets. Thus, the three strategies can combine to provide investors with one of the primary benefits of alternative investments: enhancing a portfolio's ability to perform in a wide range of market conditions.

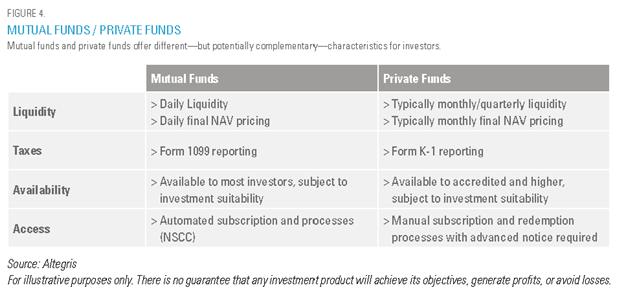

While liquid alternative investments can deliver more transparency and liquidity than typically offered by hedge funds accessible via private placement (SeeFigure 4), the two types of vehicles are not mutually exclusive within a well-diversified portfolio. For investors with the appropriate levels of investable capital for whom alternative investments are suitable, allocating sufficiently to liquid alternatives can free them up to simultaneously pursue less-liquid strategies offering higher risk-and potentially higher returns-by virtue of their longer investment horizons. As a result, liquid alternatives and private placement alternative investments can work in tandem to position a portfolio to generate potentially strong risk-adjusted returns in both up and down markets.

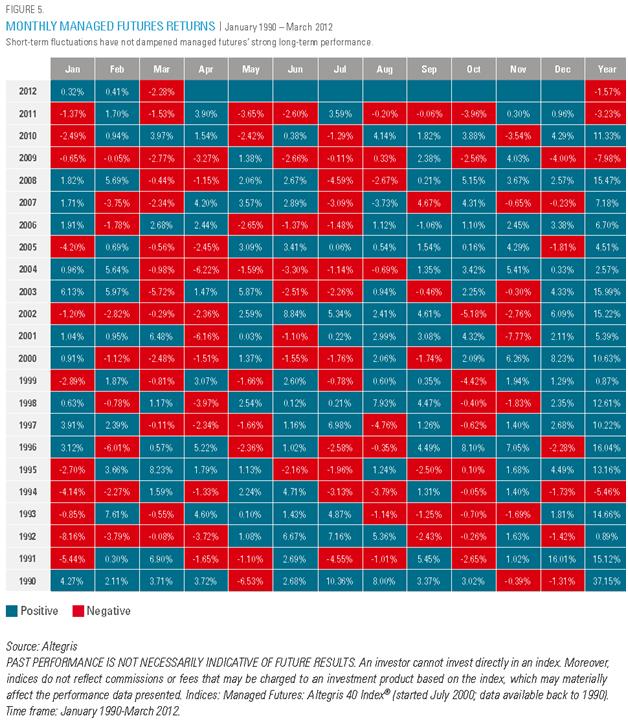

Even in the context of liquid alternative investments, it is important to keep in mind that the potential benefits of these strategies are typically realized over a long-term time horizon. For example, a quick glance at a chart of monthly managed futures performance shows a significant amount of "red," representing negative monthly returns. Yet, out of the last 22 full years for which data is available, managed futures had just three down calendar years, with average annual returns of 8.5% over that time period (See Figure 5). Investors should therefore expect managed futures-as well as other strategies, such as long/short equity or global macro-to have periods of underperformance relative to other asset classes. However, knowing that past performance is not necessarily indicative of future results, we believe that, historically, these strategies have proven their worth over the long term, and that patient investors will be best positioned to maximize the attributes of these approaches. In contrast to core strategies such as long/short equity, managed futures and global macro, some strategies that are compelling in a hedge fund format do not necessarily translate as well to mutual funds. For example, some are not sufficiently liquid. Indeed, the lack of liquidity is a fundamental driver of investment returns for these strategies. This group includes virtually all forms of distressed securities investing, certain structured credit approaches and activist/special-situation strategies. However, while these strategies can provide challenges within a liquid mutual fund structure, they remain more nimble than investments such as physical private real estate, private equity, venture capital, timber and other hard assets, and infrastructure when considering them within a portfolio context (See Figure 6). Leverage is another key factor in evaluating whether an alternative investment strategy fits within a mutual fund format. Strategies such as relative value and statistical arbitrage, for example, can produce attractive risk-adjusted returns, yet they require leverage levels beyond what is allowable in a mutual fund structure in order to be effectively implemented.

Part two of this article will be published in the next Opalesque Futures Intelligence About the Author: Jon Sundt, President & CEO, Altegris Jon Sundt President & CEO Jon Sundt has more than 25 years of experience in the alternative investment industry. He founded Altegris in 2002 and is President and CEO of the Altegris Companies and is a member of the Altegris Investment Committee. Altegris is one of the leading providers of best-of-breed alternative investments including hedge funds and mutual funds. Jon began his career as an options trader in 1986. Prior to founding Altegris, he served six years as Director of Managed Accounts and Senior Vice President of the Managed Investments Division of Man Financial, a subsidiary of the Man Group. An expert in managed futures and alternative investment strategies, Jon is the 2011 recipient of Institutional Investor's Rising Stars in the Mutual Fund Industry award. |

|

This article was published in Opalesque Futures Intelligence.

|

{kind=link}