Designed as investable benchmarks that replicate the performance characteristics of sophisticated hedge fund strategies, the IQ Hedge benchmark indexes were originally introduced on March 30, 2007, and have been calculating live since that date. IQ Hedge is the first family of investable benchmark indexes covering hedge fund replication/alternative beta strategies.

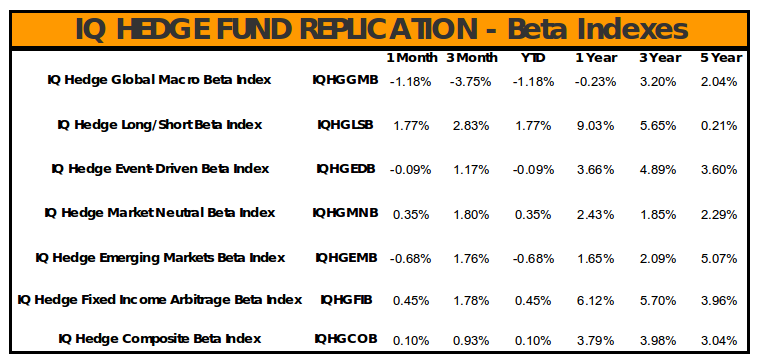

For the period ended January 31, 2013, the returns for the indexes were as follows:

Performance greater than one year is annualized. Past performance does not guarantee future results.

Performance greater than one year is annualized. Past performance does not guarantee future results.

Since its founding in 2006, IndexIQ has been a pioneer in the development and application of innovative index-based investment strategies. The IQ Hedge Indexes are increasingly being used as the basis of investment products worldwide, and as benchmarks for advisors to determine how well their actively managed hedge funds and alternative mutual funds are actually performing.

IndexIQ Indexes underlie a variety of investment products globally including ETFs, mutual funds, and institutional accounts. IndexIQ products are designed to be liquid, transparent, low cost,* and accessible to a broad range of investors, many of which are the first of their kind to be introduced to the market, including:

- IQ Alpha Hedge Strategy Fund (IQHIX Institutional Share Class; IQHOX Investor Share Class), the first open-end, no-load hedge fund replication mutual fund;

- IQ Hedge Multi-Strategy Tracker ETF (NYSE Arca: QAI), the first US-listed hedge fund replication Exchange-Traded Fund;

- IQ Hedge Market Neutral Tracker ETF (NYSE Arca: QMN) providing exposure to the market neutral hedge fund universe (launch 10/4/12);

- IQ Hedge Macro Tracker ETF (NYSE Arca: MCRO), the first Global Macro/Emerging Markets hedge fund replication ETF;

- IQ Merger Arbitrage ETF (NYSE Arca: MNA), the first merger arbitrage ETF;

- IQ Real Return ETF (NYSE Arca: CPI), the first US-listed real return ETF, which seeks to generate a real return above the rate of inflation as measured by changes in the Consumer Price Index;

- IQ US Real Estate Small Cap ETF (NYSE Arca: ROOF), the first US Real Estate Small Cap ETF;

- IQ Global Resources ETF (NYSE Arca: GRES), the first hedged global natural resources ETF;

- IQ Global Agribusiness Small Cap ETF (NYSE Arca: CROP), the first agribusiness small cap ETF;

- IQ Global Oil Small Cap ETF (NYSE Arca: IOIL), the first global oil small cap ETF;

- IQ Canada Small Cap ETF (NYSE Arca: CNDA), the first Canada small cap ETF;

- IQ Australia Small Cap ETF (NYSE Arca: KROO), the first Australia small cap ETF.

Press release

bc