RSS

RSS|

At the recent New York CTA Expo, author and trend following CTA Andrew Abraham delivered a presentation on managed futures portfolio development in light of difficult market environments By Andrew Abraham In every strategy you can have positive market environments as well as negative periods. There is no Holy Grail nor is investing ever really easy.

Trend following fund manager Andrew Abraham is author of two books.

There were both trends on the long side and the short side during this volatile period. Prices hit nose bleed highs on crude and then crashed back to earth. Crude hit highs in the $140 dollar range only to crash to the $30 dollar range. In both of these cases some trend following CTAs profited. Other markets such as wheat also had tremendous trends. Gold, silver and sugar also experienced moves. It does not matter if they are uptrends or downtrends commodity trading advisors have the potential to benefit via trends. However investors who chased returns were shortly disappointed in 2009 & thereafter. Too many investors seem to make the mistake of buying highs and selling lows of commodity trading advisors with managed futures. Continuing to 2013: It Has Been a Very Challenging Last 2 Years for Managed Futures. I have met with family offices who thought they made the correct decisions investing in large CTAs in 2009 only to be disappointed and actually lose money. Many investors lose money even with successful managers! It is very easy psychologically to invest when a manager is having a good run. Too many investors, however, "Buy the Highs and Sell the Lows."� Further, it is very easy to allocate to a large manager with billions under management (but they are not perfect and can lose money also). "Many investors lose money even with successful managers! It is very easy psychologically to invest when a manager is having a good run." The reality of managed futures over the last two years has been:

However as much as Past Performance is not necessarily indicative of future performance, I am encouraged. A tremendous amount of money has left the space. Some of the most well-known legends are hanging up their coats. It is not out of the norm to have periods in excess of two years with flat to negative returns. As much as this sub performance can easily continue, one can think on a contrarian basis potentially. Business Week ran an article in the late 1970s called "The Death of Equities". We all know that the greatest bull market of all time started shortly thereafter. One must truly believe that "Anything can happen." Look at the Nasdaq meltdown, Japan's stock market implosion in 1989 from 39,000 to today's numbers or even crude oil volatile run from the $140 dollar range to $30. When investing in managed futures possibly the goal is not just making money. On a personal level, even though I am a CTA myself I invest with other CTAs & managed futures in order to try to compound money over time & diversity, I am concerned about inflation. It is possible with all the money that has been printed throughout the world there is the threat of Inflation. Paul Singer, the principle of Elliott Associates L.P. $16 Billion Hedge fund has stated in one of his recent presentations that "The thing that scares me most is significant inflation, which could destroy our society." I have been trading managed futures and investing with CTAs since 1994. In order to be consistent I developed a set of rules in which I adhere to both in my trading as well as my allocation to other CTAs. As stated prior, my goal is to attempt to compound money over long periods of time. Rules for Investing in World Class Money Managers

Some unique CTAs have been around for decades and have achieved these high hurdles. Conversely countless CTAs have failed. In every field there are always a few unique people with extreme talent.

However there is NO HOLY GRAIL. It is never easy! There are always long periods of drawdowns & losing periods even with unique CTAs who have been around for decades.

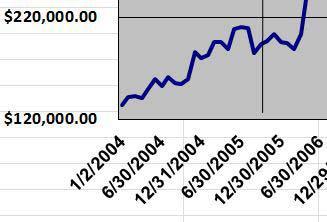

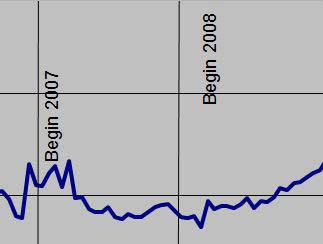

Drawdowns are inevitable. Even the successful unique CTAs that know how to deal with risk management, money management and proper trading psychology also went through some very ugly periods of trading. The irony is that probably the vast majority of investors who allocated to them did not achieve the success they did. As most traders and investors do they jump ship at the first draw down or period of illusive profits. An idea is to allocate during these inevitable drawdowns. In order to succeed when investing in managed futures, one needs the proper perspective. As in this example we will detail what can easily happen and has happened.(In the graphics below Mr. Abraham highlights periods of long, flat managed futures performance and steep drawdowns, painting a realistic picture of both negative and positive performance.)

� How Easy It Really wasn't - 1 year + of No profits. From December 2005 until December 2006

� Steep & Sharp Draw Downs

� Long Flat Period of Elusive Profits

Andrew Abraham, Principle of Abraham Investment Management has 19 years of futures trading experience investing in CTAs as well as developing and running mechanical systematic trading systems for his own trading & CTA. Andrew is the author of the books - The Bible of Compounding Money- How to Invest with World Class Money Managers as well as The Bible of Trend Following- How Professional traders compound money and manage the risks. www.AbrahamCta.com - Andrew@AbrahamCta.com |

|

This article was published in Opalesque Futures Intelligence.

|

{kind=link}