RSS

RSS|

Editor's Note: In our October issue of Opalesque Futures Intelligence we conducted an interview with Simon Lack, who authored the book Hedge Fund Mirage (Wiley, 2012). Mr. Lack made the assertion that hedge fund stated performance may not be all that it appears. In the December Opalesque Futures Intelligence we carried part one of an academic rebuttal by renowned academics Thomas Schneeweis and Hossein Kazemi. In this issue we present part two of the article.

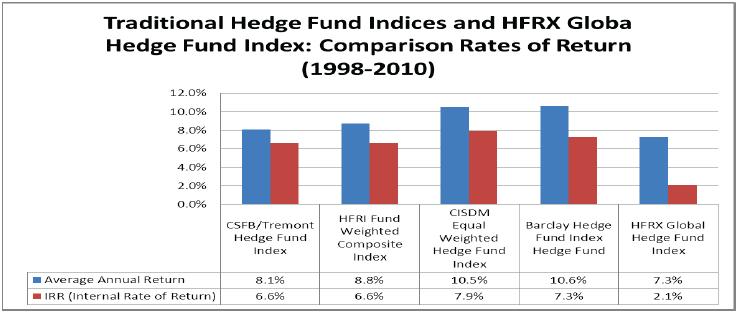

Hedge Funds as Absolute Return Generators Simon Lack emphasizes (correctly) that hedge funds are sometimes described as absolute return strategies which are not correlated with traditional stock and bond markets. In both the hedge fund and mutual fund industry some firms call their investment program 'absolute return' since they are not managed to reflect or track the performance of any stated benchmark. Investors should be careful to distinguish between a firm which calls itself 'absolute return' and which does not track a stated investment benchmark but has 'return volatility' and a firm which attempts to pass itself off as an absolute return program which makes money in every market environment with little or no volatility. For the past almost 15 years academic research (Fung and Hsieh, 2001, 2006, Schneeweis et. al, 1998, 2002, 2003, 2012) has demonstrated that hedge fund strategy returns are due not only to the unique trading skill of individual managers but also driven systematically by market factors such as changes in credit spreads, or market volatility which are directly related to the longer term fundamental security holdings of the hedge fund, rather than exclusively by an individual manager's alpha. Therefore, one can think of hedge fund returns as a combination of manager skill and an underlying return to the hedge fund strategy or investment style itself. In fact, similar to the equity and bond markets, passive security-based hedge fund indices have been created which are designed to capture the underlying return to the hedge fund strategy (Crowder, et. al, 2011).1The performance of an individual manager can be measured relative to that 'strategy' return. If a manager's performance is measured relative to the investible passive security-based hedge fund index/benchmark, then the differential return may be viewed as the manager's 'alpha' (return in excess of a similar non manager based investable replicate portfolio). If a manager's performance is measured relative to an index of other active managers, then the manager's relative performance simply measures the over or under performance to that index of manager returns. Today one does not or should not 1) refer to hedge fund returns as absolute return vehicles that have the potential for positive returns in any market environment or 2) suggest that hedge fund returns should be compared to a simple equity index, bond index or the risk free rate. We have moved on. Hedge Fund Return: Digging into the Numbers Lack criticizes the use of most hedge fund indices as creating a return which gives equal weight to all managers and therefore equates the performance of small managers with large managers. He also maintains that "you have to use an index that reflects the experience of the average investor...clearly the investors in aggregate are more heavily invested in the larger funds���‚��� if more money is invested, then that year's results affect more people and are more important. This is why hedge funds haven't been that good for the average investor, because the (average investor) only started investing in hedge funds in the last several years (pages 6-7)".As a result, Lack suggests that a better estimate of industry returns would be to "Asset Weight" all managers. This may be testable if one had a database which actually captured all hedge funds and for which reported AUM which reflects true "Industry" AUM. In fact the AUM estimated at the industry or strategy levels are just that, an estimate. Even the AUM reported in most data bases have a number of issues (an analysis of two of the largest data bases (CSFB/Tremont and CISDM/Morningstar) indicates that in any one month between 10% and 20% of firms report the same AUM in consecutive months).Thus, fund reported AUM most likely does not reflect true AUM (Schneeweis, 2012). Moreover, many large hedge fund managers fail to report to most hedge fund data sets. In short, current hedge fund AUM data is so flawed that it simply prevents any individual from using that data to estimate asset weighting within or across the industry. Despite concerns over the ability of asset weighted indices to reflect true fund weightings, Lack uses industry returns based on the HFR Global Hedge Fund index (not the original HFR Global Hedge Fund index but on a recently constructed index called the HFRX Global Hedge Fund Index). Note, Lack states that this index is a "broadly representative index that is asset weighted and is designed to reflect the industry as a whole" (p. 6). Unfortunately, "designed" does not mean "does". Anyone who takes the time to go to the HFR website will see the process by which HFR creates the index. The index itself is based on a series of algorithmic modeling, index assumptions and fund selection. It does not reflect all funds available to HFR in their data base and the process by which the strategies are weighted is unclear. Certainly one has the right to use any index one desires to represent an industry (S&P 500, Russell 1000, EAFE) but one should ensure that the index does not distort or is designed to promote one's story (or at least let the audience know). Note that the current HFRX Global Hedge Fund Index was created post 2000. As a result the constructed historical returns before its creation may be severely suspect. In Exhibit 1, we report on the relative performance of the HFRX Global Hedge Fund index returns with other hedge fund industry 'equal weighted' and'asset weighted'index based returns.2 The results remind us of the Indiana Jones movie in which Indiana Jones had to pick the right chalice or die - of course, he lives. Lack also chooses well, if the goal is to show the absence of benefits in allocating to hedge funds.For the period of his analysis (1998-2010) HFRX Global Hedge Fund index underperforms (See Exhibit 1 and Exhibit 2)other equal weighted (HFR, CISDM, and Barclay)and asset weighted hedge fund indices (CSFB)3 which are based on actual reported manager returns to the databases, and are not constructed solely "to reflect" hedge fund return through a complicated selection and algorithmic process (HFRX).4 Exhibit 1: Performance of Comparison Traditional Hedge Fund and HFRX Global Hedge Fund Index

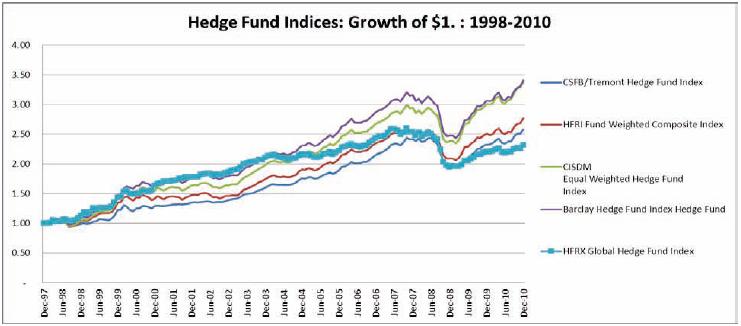

Exhibit 2: Growth of Alternative Equal Weighted and Asset Weighted Hedge Fund Indices

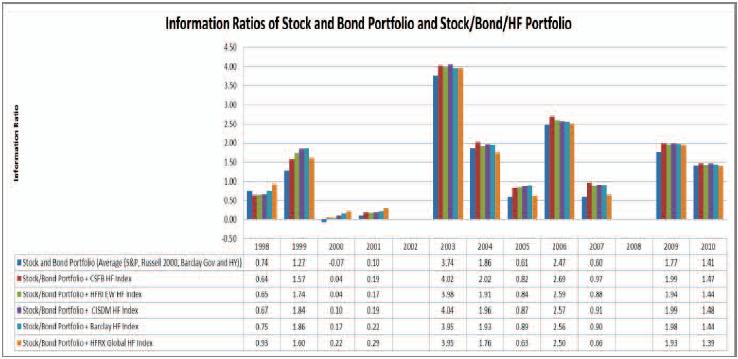

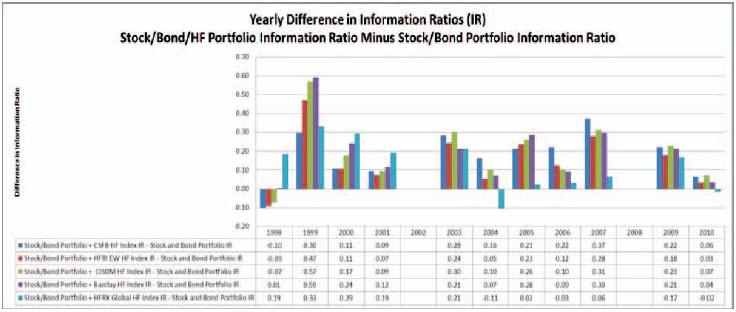

Note the Dow Jones Credit Suisse Hedge Fund IndexSM was the industry's first asset-weighted hedge fund index. In other words, Lack's results are based on a hedge fund index (HFRX Global Hedge Fund Index) which provide a low estimate of the actual hedge fund average returns relative to those reportedby most traditionally used hedge fund indices (Asset or Equal Weighted). 5Lack points out however, that if one wishes to provide an estimate of the industry return, which takes industry AUM into considerationone may wish to use a return measure discussed in (Dichev and Yu, 2010) (e.g., internal rate of return (IRR)). 6However, when one uses hedge fund index returns reported in more traditional asset or equal weighted indices, the IRR of the return over the period of analysis (using the Dichev/Yu method) increases dramatically relative to that reported for the HFRX Global hedge fund index. In short, as shown in Exhibit 1, over the time period of analysis if one uses any of themore commonly used hedge fund indices in contrast to the HFRX Global in each and every case the hedge fund index IRR (CSFB (6.6%), HFRI (6.6%), CISDM (7.9%), and Barclay (7.3%))would have been at leasttwice the approximately 3% risk free return benchmark (recommended for use by Lack) and more than three times greater than the IRR return of the HFRX Global Hedge Index (2.1%) reported by Lack. This is important, because using Lack's own methodology and using any other of the traditional hedge fund indices commonly used in academic research (asset weighted and equal weighted), the results show the benefit of hedge funds to the average investor.7 However, research has shown potential problems with the IRR approach used in the Lack analysis (Kazemi et. al., 2012). 8If one is concerned with the ability of hedge funds to provide benefits to the average investor and desires results which consider AUM differences which may have differed widely over the period of analysis, why not simply provide results on a year by year basis. The results in Exhibit 3 and 4show that for the past 13 years (1998-2010) the inclusion of any of the traditional hedge fund indices (HFR, CSFB CISDM, and Barclay) and/or the HFRX Global Hedge Fund index almost always provided return and risk benefits added to an equal weighted stock/bond portfolio9. (In years in which the portfolio return was negative, information ratio comparison is not relevant since an asset with a less negative return and lower standard deviation could report a lower (more negative information ratio). The results in Exhibit 3 and 4 contradict Lack's assertion that "virtually any combination of stocks and bonds would have turned out to be a better choice than hedge funds" (page 12).10 Exhibit 3: Yearly Information Ratios

Exhibit 4: Difference in Yearly Information Ratios

|

|

This article was published in Opalesque Futures Intelligence.

|

{kind=link}