RSS

RSS|

By Galen Burghardt and Brian Walls Pension funds are beginning to pay closer attention to managing their risks and on this front, they cannot help but notice that return volatilities in the managed futures realm are fairly stable while volatilities in equities are hugely variable. This is a lesson that we learned when we asked why drawdowns in equities would be deeper and longer than those we observe in managed futures even if the overall or average return volatilities in the two markets were set equal to one another. The answer lies in the behavior of return volatilities.

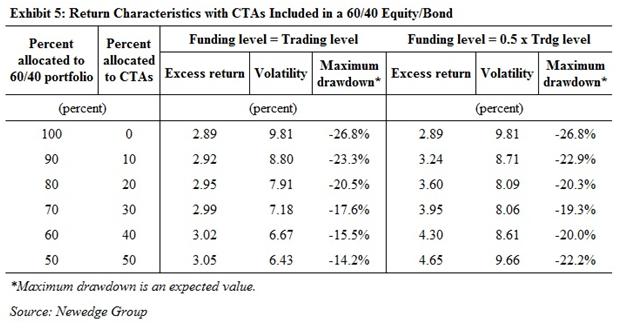

Exhibit 4: Annualized Volatilities and Net Asset Values S&P 500 Index In contrast, CTAs work hard to keep their return volatilities under control as part of their business model. As a result, when markets are highly volatile, CTAs scale back their positions to bring risk into line with their goals. These tight risk controls produced the following return volatilities:2007 8.19% 2008 7.50% From these, one would never know that 2008 and 2009 were crisis years. The Problems That CTAs Can Help Pension Funds Solve Because CTAs' returns are what they are and behave the way they do, they provide a way for pension funds to tackle three problems-smoothing return, increasing returns and reducing the depth and length of drawdowns. To illustrate these points, we set up the problem this way. First, we decided to "shrink" equity and bond Sharpe ratios back to values that would be plausible. For example, anyone who invests in equities cannot possibly believe that their true Sharpe ratio is only 0.07 and so we increased this to a value of 0.25. At the same time, we have just experienced roughly 30 years of falling interest rates and the Sharpe ratio of 1.02 for bonds seems high. So we decreased this to a value of 0.40. We left the Sharpe ratio for CTAs at 0.35 because we had no reason to suppose that this value was either too high or too low. We believe that the historical volatility values, however, are fairly realistic for an exercise like this. And so we used 16% for equity volatility, 3% for bond volatility and 9% for CTA volatility. Then we assumed that the base case would be a portfolio comprising 60% equities and 40% bonds. Anyone doing this kind of analysis must keep in mind that Sharpe ratios have wide distributions and not to demand more precision than randomness allows. At the same time, we think these are reasonably representative values for the problem at hand. As Mark Carhart and Kurt Winkelmann show in Modern Investment Management, one of the classic textbooks in this field, an equity risk premium of 4% for global equities is consistent with decades of return history and so would translate into a Sharpe ratio of 0.25 given the 16% volatility we have estimated here. Similarly, Antti Ilmanen shows in Expected Returns that a bond risk premium of 1% for a globally diversified portfolio of bonds would be in line with experience for periods that are not heavily influenced by excessive volatility. The 60/40 equity/debt mix we work with is wildly at odds with any kind of mean/variance optimum and with the global equity and bond portfolio, both of which are closer to 20/80 or 25/75, but is clearly a reflection of that fact that pension funds are leverage constrained and can achieve their expected return goals only by taking very large amounts of risk with equities. And so, using these values, here is what we found when we included CTAs in a conventional equity/debt portfolio.

If the primary objective of the pension fund is to smooth returns, then the results in Exhibit 5 show that return volatility could be reduced dramatically with no real change in expected excess returns. An allocation of 30% to CTAs, for example, would reduce the volatility of this portfolio's returns from 9.8% to 7.2%-a reduction that would have a highly tonic effect on the portfolio's Sharpe ratio. Moreover, because CTAs manage their risks the way they do, the portfolio's return volatility also would be more stable than what they now experience given the influence of equities on their portfolios. On the other hand, if the pension seeks to increase returns, they can take advantage of the fact that the CTA business model produces a portfolio of cash and futures that is very heavy on cash. The reason is simply this. Gains and losses on futures can be translated into returns only by choosing a dollar value that can serve as the denominator. The 9% return volatility that we show here is what one would calculate if you assume that an investor's funding level (i.e., the amount of cash given over the CTA) is the same as the CTA's trading level (i.e., the hypothetical amount of money used as the denominator when calculating returns). In practice, most of this cash is not needed for risk management purposes and it is possible to invest in CTAs using funding levels that are lower than the CTAs' trading levels. And, in the next set of columns in Exhibit 5, we show what would have happened to portfolio returns and volatilities if the funding level were set equal to half the trading level. The effects on returns are astonishing. A 30% allocation to CTAs would increase the overall portfolio's excess return by 1% and it would accomplish this with a reduction in overall return volatility as a bonus. Of course, almost anything that reduces the influence of equity returns on a portfolio stands to reduce the portfolio's drawdowns when times are tough. We find here that in the first case, where the funding level equals the trading level, increasing the allocation to CTAs steadily reduces the portfolio's expected maximum drawdown even up to an allocation of 50% to CTAs. What is more remarkable is that we find decreases in the portfolio's expected maximum drawdown up to a point (that is, an allocation of 30% in this example), even though we are introducing a return series whose volatility is 18% and is therefore higher than that of equity volatility. Part of the decrease is the natural effect of diversification. But at least part of the decrease is because the steady, well behaved volatility of CTA returns is better for a pension fund than is the highly variable volatility that one can expect from equity returns. How Much Should Pension Funds Invest in CTAs? This question has come up at our research forums and it is the question we addressed at the CERN asset management seminar in Geneva. The answer is surprisingly large, if you take as a starting point a portfolio that is too heavily weighted toward equities and if you grant the correlation and Sharpe ratio assumptions we used above.

We stopped at 50% for two reasons. First, an assumed allocation of 60% would require a Sharpe ratio for CTAs of 0.440, which was more than what they have delivered over the past two decades. The other was that it is almost inconceivable that a pension fund would actually commit more than 50% to something like CTAs. The important lesson to draw from this exercise, though, is that these Sharpe ratios are minimum performance standards for an alternative to stocks and bonds and CTAs have done better than these standards. Managed Futures as a Model of How Good Hedge Funds Can Be Transparency comes from the fact that everything is marked to market daily at real market prices. Investing in hedge funds-CTAs included-poses several problems for institutional investors, not the least of which is that returns are self-reported. On other fronts, however, managed futures set a standard that is rarely matched and almost impossible for other classes of hedge funds to exceed. In particular, managed futures afford high transparency and liquidity and can be used with very low foreign exchange risk. Transparency comes from the fact that everything is marked to market daily at real market prices. The liquidity stems from the fact that the CTA model combines positions in futures, which are extremely liquid, with large quantities of cash. One of the ironies of the financial crisis of 2008 was that many institutional investors turned to their CTA investments for cash because they could. As a further bonus, foreign exchange is extremely easy to manage in a CTA portfolio. The cash can be held in nearly any currency the investor chooses and the gains and losses on futures positions can be swept into the home currency with whatever frequency the investor wants. As a result, much of the foreign exchange risk that plagues a conventional globally diversified asset portfolio is minimal for investments in CTAs. Is there a capacity problem? We think that for all practical purposes the answer is no. This question was on everyone's lips when CTAs managed only $100 billion, and since then CTAs have found ways to grow well beyond what they thought were their capacity constraints. So what's not to like? Pension funds have serious problems that conventional assets may not be able to help them solve. Part of the explanation is that the bulk of what CTAs do is based on momentum trading in a highly diversified set of broad and liquid markets. Another part is that their chief trading tool is futures, where volume and open interest are defined largely by the market's demand for activity and open positions. And part of the explanation is that the largest and most successful CTAs diversify across momentum models. So there is not the same rush to get into a trade or out of a trade that brought down the quant equity strategy in August 2007. So what's not to like? Pension funds have serious problems that conventional assets may not be able to help them solve. Their returns have been too low, too volatile and their drawdowns have been too deep and too long. At the same time, the managed futures industry has matured to the point where it can offer a credible and hugely valuable investment tool that affords positive, uncorrelated and stable returns. These three things alone would make CTAs ideal for pension funds. And knowing that they work in a tightly regulated environment, that their valuations are accurate and transparent and that they afford such a high level of liquidity will assure chief investment officers that they are dealing with experienced professionals who know how to manage money. It seems to us that pension funds need what CTAs offer and they are now ready to take them seriously. Galen Burghardt and Brian Walls work in the prime brokerage unit of Newedge and co-wrote Managed Futures for Institutional Investors (Bloomberg, 2011). They thank Mark Carhart (Kepos Capital), Antti Ilmanen (AQR Capital Management) and Theodore Economou and Gregoire Haenni (CERN pension fund) for many lively conversations and for their guidance in this research. They also thank their colleagues in research at Newedge, Ryan Duncan and Lianyan Liu. Any questions about analysis or sources of data and information can be addressed directly to the authors at either galen.burghardt@newedge.com or brian.walls@newedge.com. For additional information visit www.NewEdge.com |

Managed Futures researchers Galen Burghardt and Brian Walls wrote the well received book, Managed Futures for Institutional Investors. This is the first part of a two part article penned by the two and it addresses hot topics, such as study bias in managed futures indices.

Managed Futures researchers Galen Burghardt and Brian Walls wrote the well received book, Managed Futures for Institutional Investors. This is the first part of a two part article penned by the two and it addresses hot topics, such as study bias in managed futures indices.

|

This article was published in Opalesque Futures Intelligence.

|

{kind=link}