RSS

RSS|

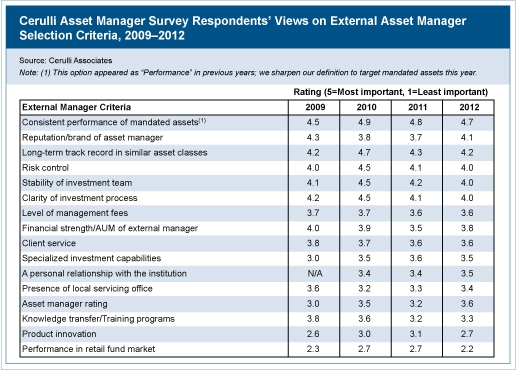

Opaleque Industry Update - Niche strategy managers will prosper while general strategy managers will mostly struggle in future. Cerulli Associates estimates that Asia ex-Japan institutional assets accessible to external asset managers (i.e., addressable assets) have expanded from US$462.2 billion in 2007 to US$998.3 billion at the end of 2011. Cerulli projects that this figure will continue to climb to more than US$1.7 trillion in 2016. At the same time, addressability will improve from 8.9% in 2007 to a projected 12.3% in 2016. However, the growing pool of addressable assets translates into neither easier access for all types of asset managers nor greater profitability. Cerulli's conversations with institutional asset owners show that, over the long term, the mandate universe is developing hourglass characteristics: either very specialized (such as absolute return Taiwanese equities) or very index-driven (such as minimum-volatility global equity index). Both examples are mandates from Taiwan's new Labor Pension Fund in 2012. Indeed, alternatives, single-country, and regional allocations are playing larger and larger roles in Asian institutions' portfolios. Cerulli's proprietary survey of asset managers in Asia ex-Japan also shows that specialization has gained significance as a criterion for being awarded a mandate: in 2009, it was rated 3 on a scale of 1 to 5 where 5 is most important. This rating has increased in consecutive years to 3.5 in 2012.

Mandates that call for specialized investment abilities, such as emerging market fixed income, Greater China, private equity, or hedge funds, still pay a premium over broad mandates. For instance, institutions award 40 to 80 basis points (bps) for emerging market equities versus 5 bps to 20 bps for local fixed income. As for hedge funds, few investors have been willing to pay the 200 bps management fee plus 2,000 bps performance levy (known as "2 and 20") since the Bernard Madoff scandal; but among private equity funds, the 2 and 20 fee structure meets with much less resistance. However, instances of fee wars-sometimes down to zero management fees-are appearing increasingly often as external asset managers in markets such as China, Korea, and Thailand attempt to win institutional assets, even if it is at a loss. Sometimes, the institutions themselves or their regulators are encouraging zero management fee structures. In China, for example, Cerulli is aware of the insurance regulator encouraging insurers to consider paying only performance fees to external managers. "The well-established global asset management firms don't usually participate in these kinds of competition, but there is no shortage of firms that will, especially recent entrants that need the prestige and perceived credibility of managing institutional assets," says Ken Yap, head of Asia-Pacific research at Cerulli Associates. In China, for example, numerous managers of enterprise annuity (corporate pension) assets have been accepting deals at a loss for years. On the other hand, the largest, most transparent Asian institutions, such as Korea Investment Corporation, the National Pension Service of Korea, and the Employees Provident Fund of Malaysia, are generally willing to pay fair rates for impeccable investment management and servicing, but the assets they outsource to external managers are increasingly niche. "But the move toward increasingly niche mandates will develop over some time. For now, there are still broad mandates available, and the profitability depends on volume," Yap says. Cerulli's survey of asset managers shows that managing assets from central banks, quasi-government organizations, and pension funds (both government and corporate) yields the greatest profits in institutional business. Family offices are the least profitable, although many asset managers in Asia are keen to work with family offices. Press release These findings and more are from Quantitative Update: Institutional Asset Management in Asia 2012. CLICK HERE to request a press copy of this research. Bg |

Industry Updates

Cerulli: Asian institutional assets face profitability squeeze

Thursday, November 29, 2012

|

|

{kind=link}